United States Electric Vehicle Charging Station Market Size, Share, Trends and Forecast by Charging Station Type, Vehicle Type, Installation Type, Charging Level, Connector Type, Application, and Region, 2026-2034

United States Electric Vehicle Charging Station Market Size, Share, Trends & Forecast (2026-2034)

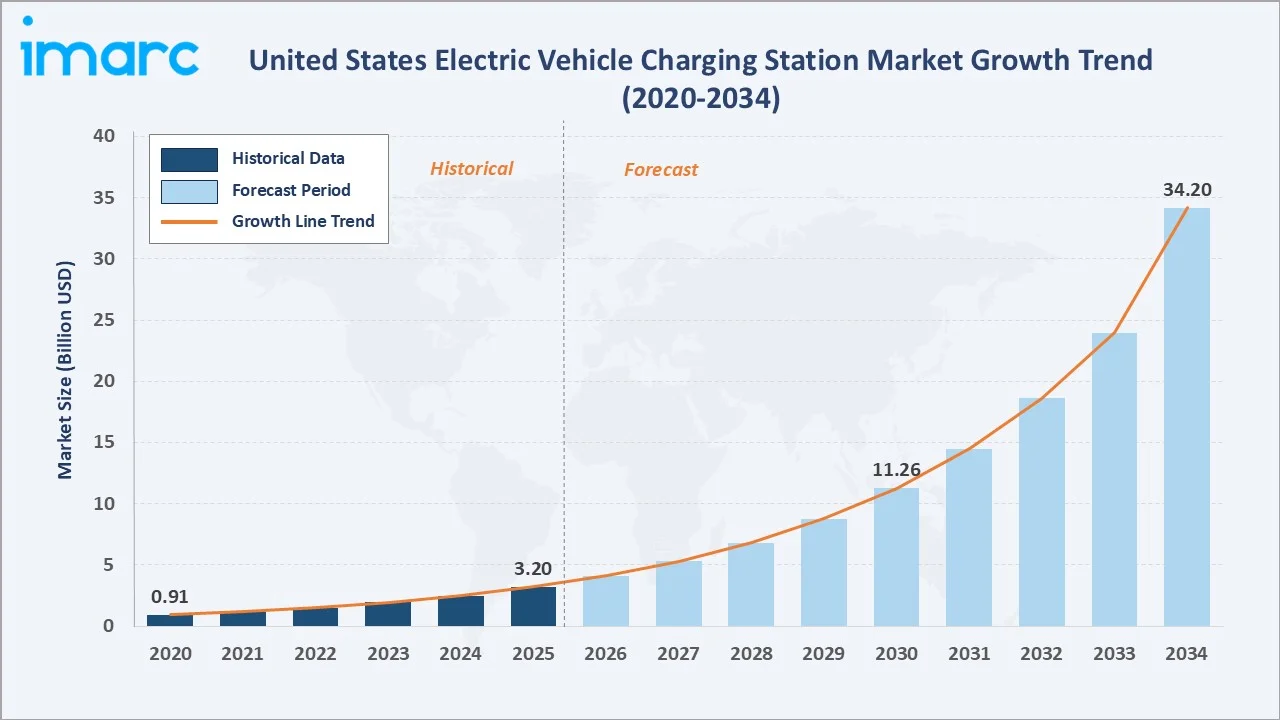

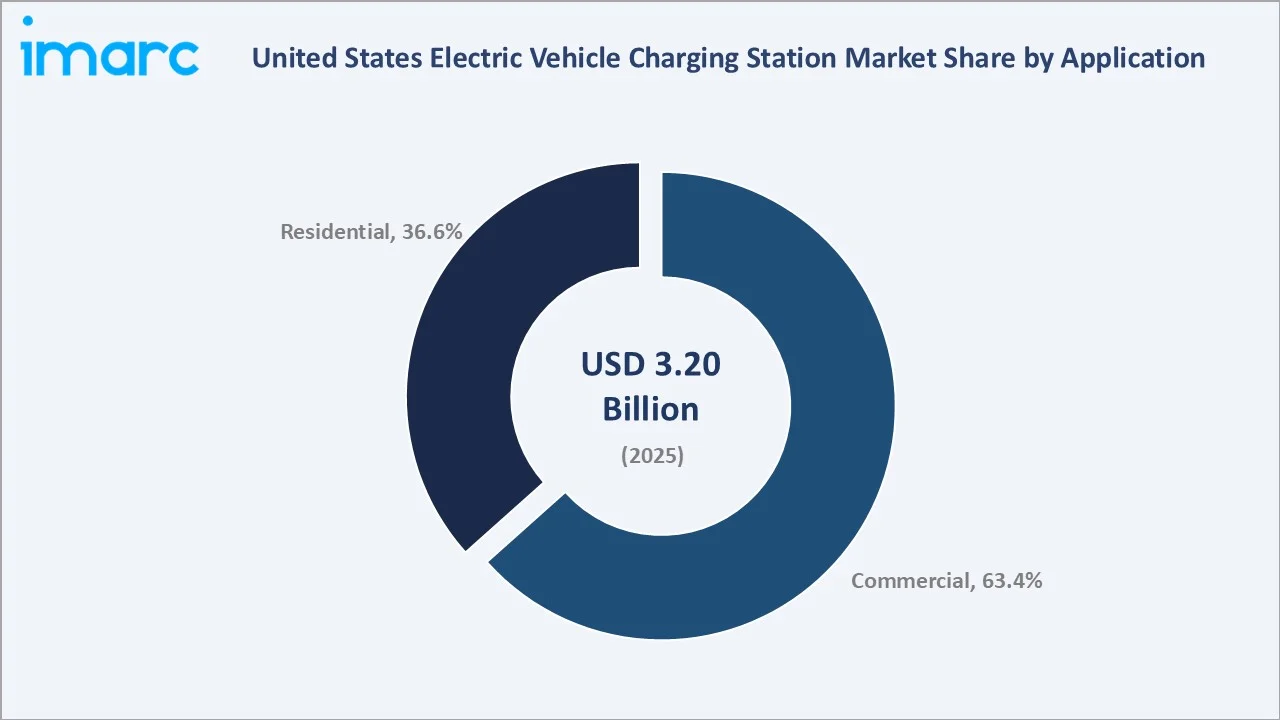

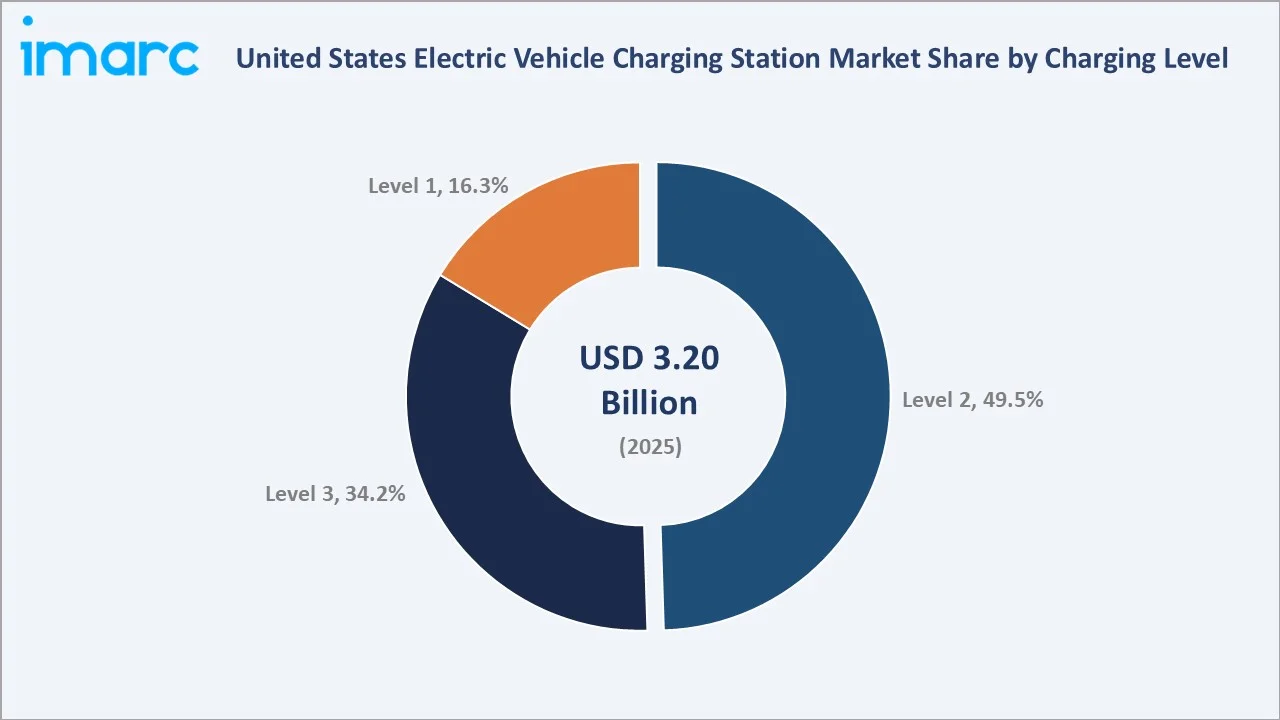

The United States electric vehicle charging station market reached USD 3.20 Billion in 2025 and is projected to reach USD 34.20 Billion by 2034, growing at a CAGR of 28.60% during 2026-2034. The growth trajectory of the market reflects the convergence of landmark federal legislation surging EV adoption across all vehicle segments, and the accelerating corporate sustainability commitments of US fleet operators, retailers, and commercial real estate developers investing in charging infrastructure to attract and retain EV-driving customers and employees.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.20 Billion |

|

Forecast Market Size (2034) |

USD 34.20 Billion |

|

CAGR (2026-2034) |

28.60% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

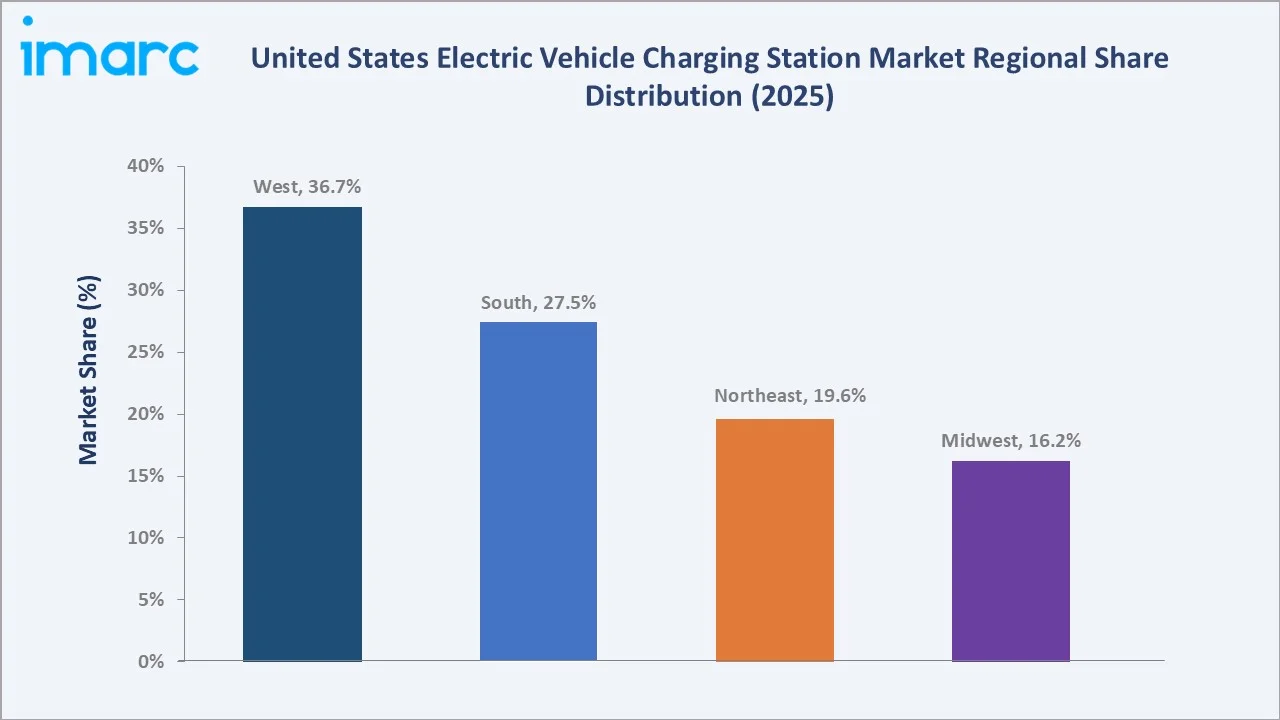

The West region leads with a 36.7% market share in 2025, driven by California's ZEV mandate, the highest US EV penetration rate, and state-level charging infrastructure incentives layered on top of federal NEVI funding. Commercial applications dominate the segment breakdown at 63.4%, while Level 2 charging retains the largest share at 49.5% across charging levels.

To get more information on this market, Request Sample

The US EV charging station market is underpinned by structural forces: the federal NEVI program's USD 5 billion highway corridor funding mandate requiring charging stations every 50 miles on designated alternative fuel corridors, the IRA's Section 30C tax credit providing 30% credit on purchase and installation of qualified alternative fuel vehicle refueling property, including electric vehicle charging equipment, and the NACS (North American Charging Standard) standardization adopted by all major US automakers.

Executive Summary

The United States electric vehicle charging station market is experiencing exceptional expansion, driven by the largest government infrastructure investment in US energy history, accelerating EV adoption across passenger and commercial vehicle segments, and corporate sustainability mandates compelling nationwide charging deployment. The market reached USD 3.20 Billion in 2025 and is forecast to reach USD 34.20 Billion by 2034, growing at a CAGR of 28.60%.

Commercial applications dominate with a 63.4% share in 2025, encompassing workplace charging, retail and hospitality destination charging, public parking facilities, highway corridor fast charging hubs, and fleet depot charging installations. Level 2 AC charging retains 49.5% of the charging level segment, valued for its cost-effective installation, broad vehicle compatibility, and suitability for dwell-time charging scenarios where vehicles park for 2–8 hours.

The West region at 36.7% leads regionally, anchored by California's 1.5 million+ ZEV fleet, and the highest concentration of EV charging network operators. Leading vendors are competing across hardware manufacturing, network operations, and managed charging service delivery.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Commercial – 63.4% share (2025) |

|

Fastest Growing Application |

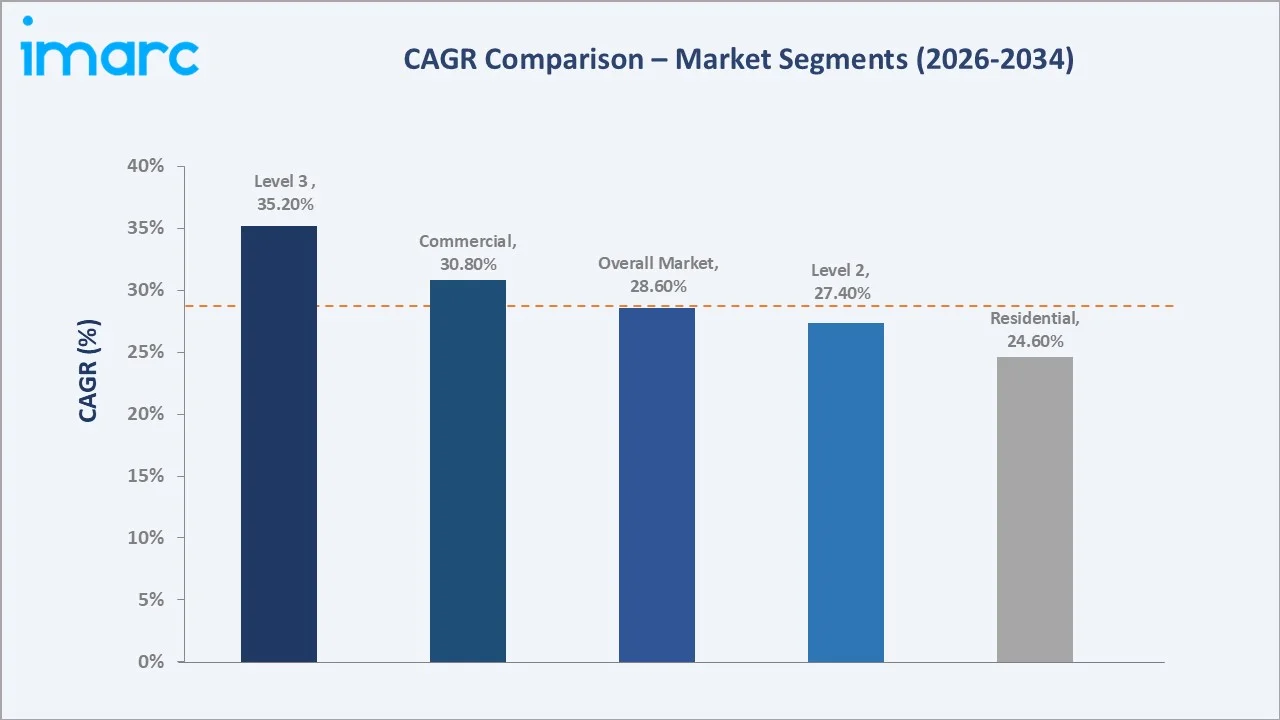

Commercial – ~30.8% CAGR (2026-2034) |

|

Largest Charging Level |

Level 2 – 49.5% share (2025) |

|

Fastest Growing Charging Level |

Level 3 (DC Fast) – ~35.2% CAGR (2026-2034) |

|

Leading Region |

West – 36.7% share (2025) |

|

Top Companies |

ChargePoint, Inc., Tesla, EVgo Services LLC, Blink Charging Co. |

Key Analytical Observations Supporting the Above Data:

- Commercial applications at 63.4% (2025) dominate owing to the economic returns on commercial EVSE investment, creating multi-stakeholder investment drivers that residential charging cannot match.

- Level 2 at 49.5% (2025) remains dominant because its cost profile enables mass deployment across the commercial destination and workplace charging segments that represent the largest share of charging sessions by volume.

- Level 3 DC fast charging with 34.2% (2025) share is growing fastest as the NEVI program mandates 150+ kW charging capability at federally funded highway corridor stations and commercial charging operators deploy ultra-fast 350 kW stations at truck stops and urban charging hubs to capture the premium revenue opportunity of 15–30 minute fast charge sessions.

- The West region's 36.7% share (2025) reflects strong EV adoption across the region, supported by California reaching a major milestone in Q4 2025 by surpassing 2.5 million cumulative new EV sales since 2011.

United States Electric Vehicle Charging Station Market Overview

Electric vehicle charging stations (EVCS) encompass the complete infrastructure ecosystem for delivering electrical energy to EV batteries, spanning Level 1 (120V AC household outlet), Level 2 (240V AC dedicated EVSE), and Level 3 (DC fast charging at 50–350+ kW). Applications span residential home charging, commercial workplace and retail charging, public fast charging, and fleet depot charging across passenger vehicles, commercial vans, and Class 8 trucks.

The market's structural growth engine is the policy-investment nexus: the IIJA allocation of USD 7.5 billion for U.S. EV charging infrastructure, including USD 5 billion under NEVI and USD 2.5 billion in competitive grants to expand a reliable national charging network. Along with that, IRA's Section 30C Alternative Fuel Vehicle Refueling Property Tax Credit represents the largest public-sector EV charging investment in US history.

Market Dynamics

To evaluate market opportunities, Request Sample

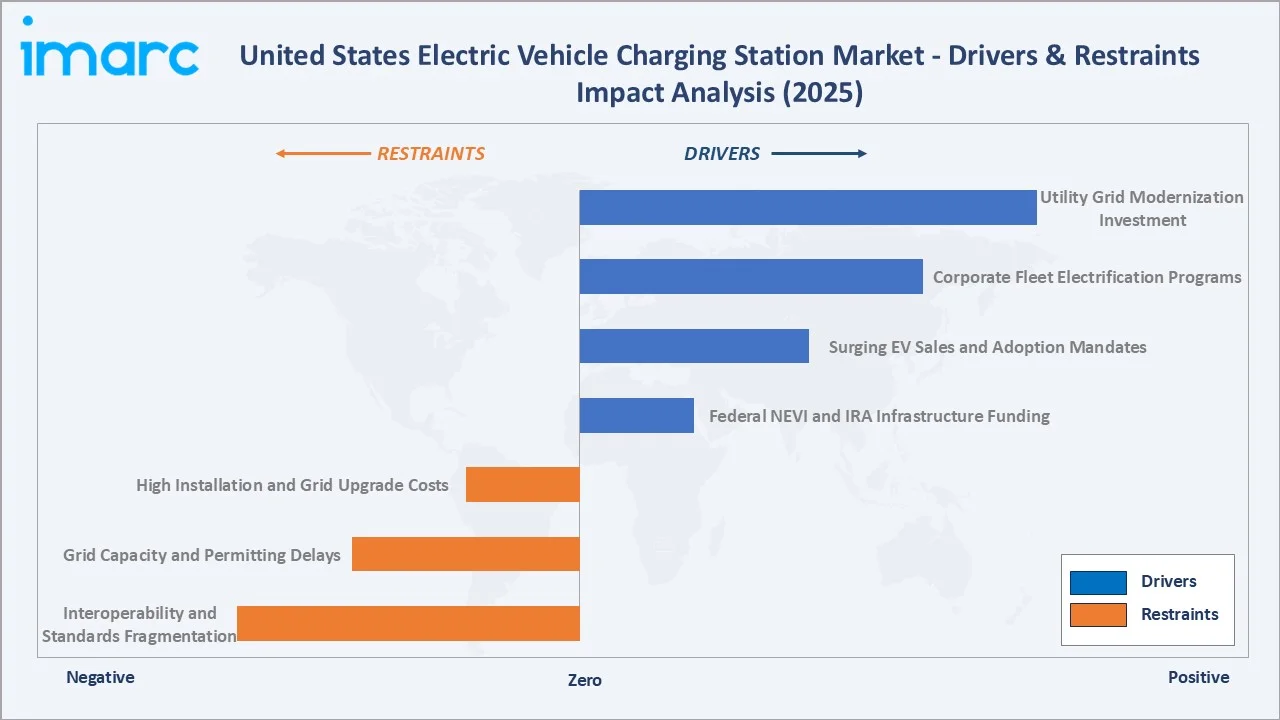

Market Drivers

- Federal NEVI and IRA Infrastructure Funding: The Infrastructure Investment and Jobs Act's USD 7.5 billion EV charging allocation, combined with the IRA's commercial charging tax credits and alternative fuel vehicle incentives, represents the largest federal EV infrastructure program in US history.

- Surging EV Sales and Adoption Mandates: US EV sales accounted for 234,000 in Q4 2025, representing 7.8% of new vehicle sales, with California, New York, and 16 additional states adopting Advanced Clean Cars II regulations mandating 100% zero-emission light-duty vehicle sales by 2035.

- Corporate Fleet Electrification Programs: Amazon's commitment to 100,000 electric delivery vans by 2030, FedEx's all-electric fleet transition plan, and Walmart's fleet electrification program collectively create USD 8–15 billion in fleet depot charging infrastructure investment demand through 2030.

- Utility Grid Modernization Investment: Electric utilities are investing USD 5+ billion in EV-specific grid upgrades that directly enable higher-power commercial and fleet charging installations previously constrained by grid capacity limitations. Utility-funded make-ready programs, which prepare electrical infrastructure to charger-ready condition at no cost to site hosts, are directly reducing the effective cost of commercial EVSE deployment by 20–40%.

Market Restraints

- High Installation and Grid Upgrade Costs: The cost of a single-port EVSE unit typically ranges from USD 300–1,500 for Level 1 chargers, USD 400–6,500 for Level 2 chargers, and USD 10,000–40,000 for DC fast chargers. Installation costs can vary significantly by site, with estimated ranges of USD 0–3,000 for Level 1, USD 600–12,700 for Level 2, and USD 4,000–51,000 for DC fast charging.

- Grid Capacity and Permitting Delays: Grid interconnection queues for high-power DCFC installations at utility service territory boundaries have extended to 18–36 months in constrained areas of California, New York, and Texas, creating significant project development risk for charging station operators.

- Interoperability and Standards Fragmentation: Despite NACS standardization adoption by major OEMs, the US market continues to operate a fragmented charging protocol ecosystem requiring multi-standard stations that increase hardware costs by 15–25% per charging port.

Market Opportunities

- Retail and Hospitality Destination Charging Expansion: In April 2026, Walmart and ABB E-mobility launched ABB’s A400 All-in-One fast chargers at seven Walmart locations in the Phoenix metropolitan area as part of a planned nationwide U.S. rollout. The chargers deliver up to 400 kW, support both CCS and NACS connectors, and aim to make EV charging more convenient by integrating it with Walmart’s retail locations.

- Medium and Heavy-Duty Vehicle Charging Infrastructure: The Commercial Clean Vehicle Credit, providing up to USD 40,000 per commercial vehicle, and the NEVI Heavy Duty program, providing USD 2.5 billion for truck stop charging, are creating investment momentum in the highest-power charging tier.

Market Challenges

- Charging Reliability and Uptime Performance: By the end of 2023, some major EV charging networks reported outage rates of up to 70% across their DC fast-charging ports, driven by software failures, payment system outages, and vandalism. Poor charging reliability erodes EV driver confidence and suppresses public charging utilization rates.

- Workforce Development for Electrician Shortage: The EV charging installation pipeline requires licensed electricians for all electrical work, creating a workforce bottleneck. The International Brotherhood of Electrical Workers and the National Joint Apprenticeship and Training Committee have launched EV charging-specific training programs, but the apprenticeship-to-journeyman timeline of 5 years means the skilled workforce constraint will moderate EVSE deployment speed through at least 2027.

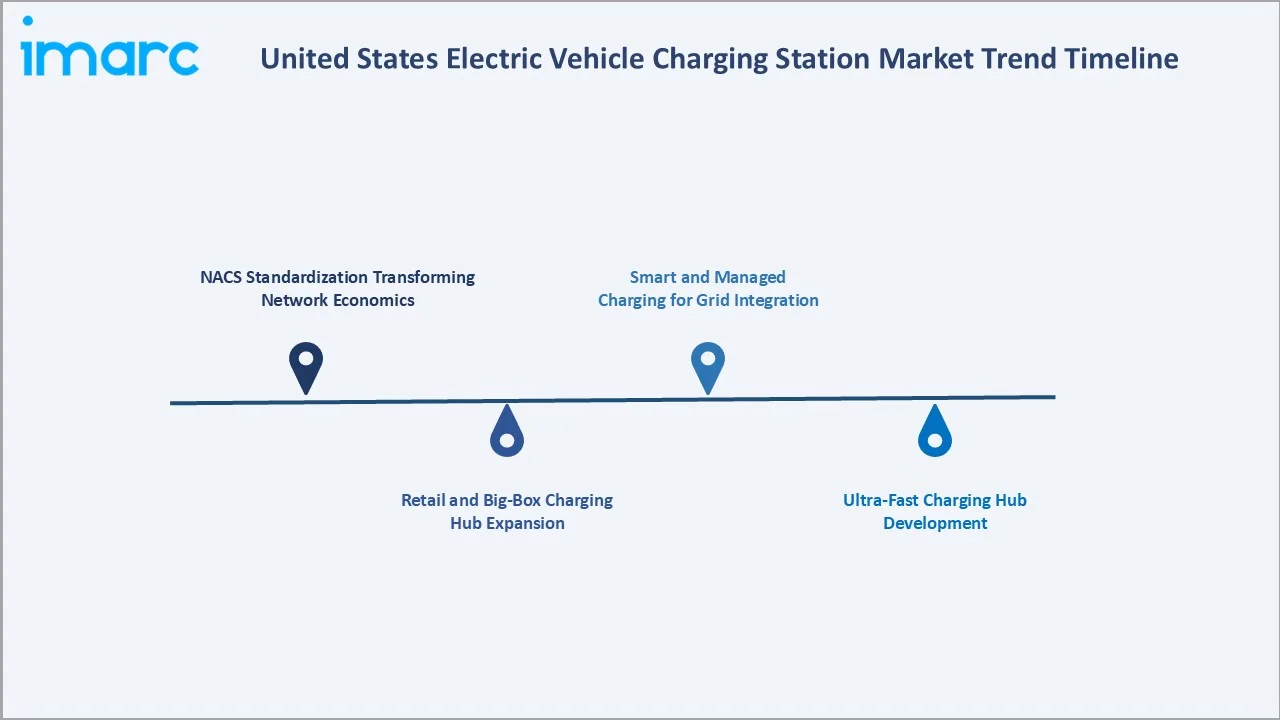

Emerging Market Trends

1. NACS Standardization Transforming Network Economics

The adoption of NACS by Ford, GM, Honda, Nissan, Mercedes-Benz, and essentially all major automakers since 2023 is eliminating the connector fragmentation that previously required multi-standard charging stations. In December 2024, ChargePoint, Inc. and General Motors announced plans to install many hundreds of ultra-fast public charging ports across the U.S. by the end of 2025, using Omni Port and up to 500 kW Express Plus charging technology.

2. Retail and Big-Box Charging Hub Expansion

Target, Kroger, and major shopping mall REITs are deploying destination charging as a customer dwell-time monetization strategy, recognizing that EV drivers at Level 2 charging stations spend 15–45 additional minutes in-store per session. This creates a new revenue stream for site hosts while delivering the customer proximity density that maximizes charging session frequency and network utilization.

3. Ultra-Fast Charging Hub Development

The charging industry is transitioning from distributed individual-station deployment toward high-power charging hub architecture with facilities including 8–50+ DCFC ports at 150–350 kW per port, designed for 15–30 minute turnaround charging at highway rest areas, urban parking structures, and logistics corridors.

4. Smart and Managed Charging for Grid Integration

Utility partnerships with charging network operators are advancing smart charging programs that dynamically schedule EV charging sessions to align with off-peak electricity pricing and renewable energy availability, reducing both charging costs for EV owners and peak demand charges for site hosts.

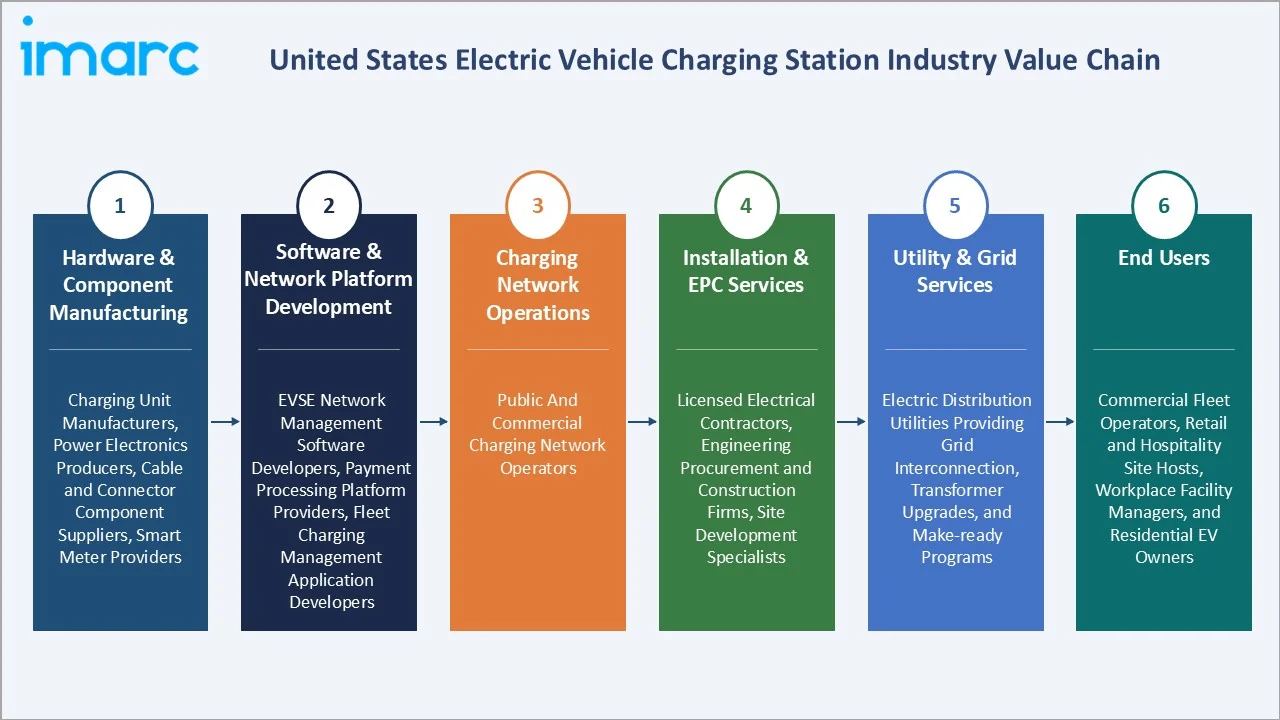

Industry Value Chain Analysis

The US EV charging station value chain spans hardware manufacturing through end-user charging service delivery, with each stage occupied by specialized manufacturers, software developers, network operators, installation contractors, and utility partners whose performance directly influences charging availability, reliability, and total cost of ownership.

|

Stage |

Key Players / Examples |

|

Hardware & Component Manufacturing |

Charging unit manufacturers, power electronics producers, cable and connector component suppliers, smart meter providers |

|

Software & Network Platform Development |

EVSE network management software developers, payment processing platform providers, fleet charging management application developers |

|

Charging Network Operations |

Public and commercial charging network operators |

|

Installation & EPC Services |

Licensed electrical contractors, engineering procurement and construction firms, site development specialists |

|

Utility & Grid Services |

Electric distribution utilities providing grid interconnection, transformer upgrades, and make-ready programs |

|

End Users |

Commercial fleet operators, retail and hospitality site hosts, workplace facility managers, and residential EV owners |

Technology Landscape in the United States EV Charging Station Industry

Level 2 AC Charging Infrastructure

Level 2 EVSE constitutes the backbone of US commercial and residential charging infrastructure, accounting for 49.5% of market share in 2025. ChargePoint's CP6000 series and Blink's IQ 200 series represent the commercial-grade Level 2 hardware serving workplace, retail, and hospitality charging applications.

Level 3 DC Fast Charging Infrastructure

DC fast charging is experiencing the most rapid technological evolution in the market, with 350 kW high-power charging (HPC) stations becoming the new deployment standard for highway corridor applications. ABB's Terra HP 350 kW chargers and Tesla's V4 Supercharger represent the current commercial standard, while 1+ MW megawatt charging systems for commercial trucks are advancing through pilot deployments at Pilot Flying J and TA/Petro truck stop networks.

Smart Charging and Energy Management Platforms

In November 2025, ChargePoint released its next-generation ChargePoint Platform to manage EV charging operations across fleets, commercial sites, CPOs, OEMs, and energy providers. The platform supports charging infrastructure from single sites to global networks, with enhanced software integration, energy-system compatibility, and operational optimization features.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Commercial |

63.4% |

2025 |

|

Charging Level |

Level 2 |

49.5% |

2025 |

|

Charging Station Type |

🔒 |

🔒 |

2025 |

|

Vehicle Type |

🔒 |

🔒 |

2025 |

|

Connector Type |

🔒 |

🔒 |

2025 |

|

Installation Type |

🔒 |

🔒 |

2025 |

|

Region |

West |

36.7% |

2025 |

By Application

The commercial segment dominates with a 63.4% share in 2025, reflecting the multiple compounding investment drivers, including IRA tax credits, customer attraction ROI, fleet decarbonization mandates, and NEVI program access, that simultaneously make commercial EVSE investment financially compelling across a broad range of business contexts.

To access detailed market analysis, Request Sample

Residential charging represents 36.6% of the market, encompassing Level 1 convenience charging using standard household outlets and Level 2 home charging via dedicated 240V EVSE units installed in garages and driveways. Home charging represents 80%+ of total EV charging sessions by volume, making residential EVSE the highest-frequency use case even while commercial infrastructure captures the majority of revenue.

By Charging Level

Level 2 commands a 49.5% share in 2025. Level 2's market leadership reflects its optimal balance of charging speed, installation cost, and grid impact for the dominant commercial destination and workplace charging use cases.

Level 3 DC fast charging represents 34.2% and is growing fastest (~35.2% CAGR) as the NEVI program mandates 150+ kW DCFC deployment at highway corridors, Tesla opens its Supercharger network to all NACS-compatible vehicles, and commercial operators deploy ultra-fast charging hubs to compete in the premium highway and urban fast-charge segment.

Regional Market Insights

The West region's leadership (36.7%, 2025) is structurally anchored by California's combination of the highest US EV penetration rate, the California ZEV mandate driving 100% zero-emission vehicle sales by 2035, and the Fast Charge California Project offering statewide incentives of up to USD 100,000 per DC fast-charging port.

The South at 27.5% is the fastest-growing region in percentage terms, with Texas, Florida, and Georgia collectively representing the three largest state EV markets after California. Texas's deregulated energy market is enabling innovative demand response and V2G business models for commercial charging operators, while Florida's tourism-driven economy creates high charging demand at hotels, theme parks, and highway corridors.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West |

36.7% |

Leading state-level ZEV mandates and EV adoption rates; comprehensive utility make-ready programs reducing installation costs; favorable LCFS and state incentive structures |

|

South |

27.5% |

Rapidly growing EV adoption across major metropolitan areas; significant corporate fleet electrification activity from logistics and distribution operators; expanding state-level EV incentive programs in Texas, Florida, and Georgia |

|

Northeast |

19.6% |

Dense urban population centers driving high public charging utilization rates; significant DCFC deployment; strong commercial and workplace charging investment |

|

Midwest |

16.2% |

Significant fleet depot charging investment from manufacturing and logistics operators; NEVI funding activating highway corridor deployments; growing utility support programs in Illinois, Michigan, and Minnesota. |

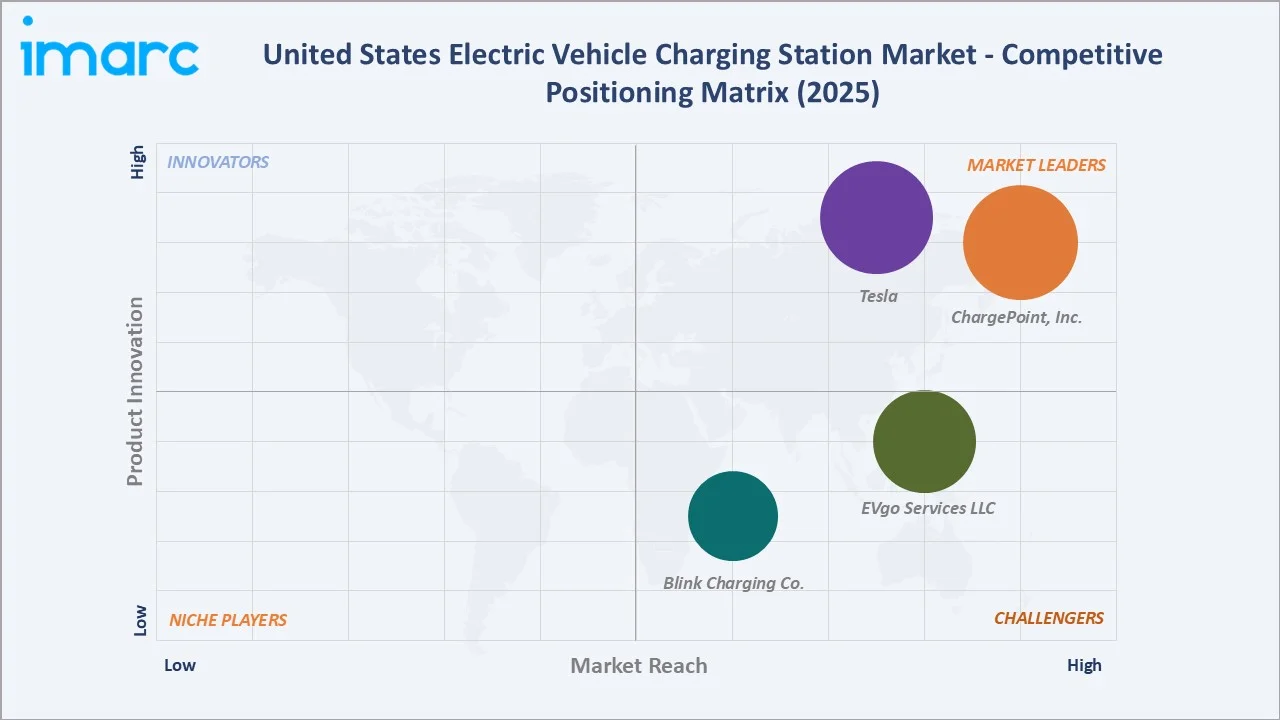

Competitive Landscape

The United States EV charging station market exhibits moderate fragmentation, with the top four operators collectively operating approximately 65–70% of public Level 2 and DCFC ports by station count in 2025.

|

Company Name |

Solutions/Brands |

Market Position |

Core Strength |

|

ChargePoint, Inc. |

Next-gen Express, Express Plus, ChargePoint Home Flex, Express 280, CP6000, Express Solo |

Market Leader |

Largest US charging network by station count; enterprise fleet and workplace charging platform; broad OEM and utility partnerships |

|

Tesla |

Charging, Home Charging, Supercharging, Wall Connector for Business, Supercharger for Business, Semi Charging for Business |

Market Leader |

Highest-rated charging reliability and user experience among major public networks, NACS open-network expansion to all compatible vehicles; integrated vehicle-to-charger ecosystem |

|

EVgo Services LLC |

EVgo Autocharge+, EVgo eXtend |

Strong Challenger |

Urban fast charging network; major retailer co-location partnerships; consistent 24/7 reliability |

|

Blink Charging Co. |

Charge on the Go, Charge at Home, Blink Charging for Businesses, Blink Care Program |

Challenger |

Fleet and workplace solutions; broad property owner partnerships |

Competition is intensifying as companies differentiate through charger reliability, DC fast-charging capacity, interoperability, subscription-based services, and access to federal and state infrastructure funding.

Key Company Profiles

ChargePoint, Inc.

ChargePoint, Inc. is one of the US’s largest EV charging networks by station count. The company’s software-centric business model differentiates it from pure-play network operators and enables faster scaling without the capital requirements of a fully owned-and-operated model.

- Product Portfolio: CP6000 Level 2 commercial chargers, Express Plus modular DCFC system, Home Flex Level 2 residential charger, ChargePoint Cloud network management platform, Next-gen Express, Express 280, and Express Solo.

- Recent Developments: In April 2026, ChargePoint, Inc. launched Express Solo, a standalone DC fast charger capable of delivering up to 600 kW to one EV or sharing power across up to four EVs. The charger features a compact footprint, around 40% higher power density, NACS/CCS support, and integration with solar, battery storage, and Eaton power systems.

- Strategic Focus: Fleet and workplace charging platform growth; ultra-fast DCFC hub expansion; NACS hardware transition; commercial truck charging infrastructure development.

EVgo Services LLC

EVgo Services LLC is one of the US’s leading pure-play public DCFC network operators. The company’s strategic focus on urban fast charging co-located with major retailers creates a high-utilization charging portfolio.

- Product Portfolio: DC fast charging stations, high-power charging hubs, in-depot fleet fast charging, EVgo eXtend white-label DCFC network solutions, and EVgo Autocharge+.

- Recent Developments: In March 2025, EVgo Services LLC and Toyota opened the first DC fast-charging stations under Toyota’s “Empact” vision, located in Baldwin Park and Sacramento, California. Each EVgo-owned station can serve up to eight vehicles simultaneously and features 350 kW fast chargers, improving public charging access in underserved communities.

- Strategic Focus: Urban DCFC hub density expansion; NACS transition completion; fleet fast charging solutions; profitability improvement through utilization optimization and operating leverage.

Market Concentration Analysis

The US EV charging station market exhibits asymmetric concentration: the DCFC segment is highly concentrated, with Tesla operating 54% of public fast charging ports, while the Level 2 segment is more fragmented, with ChargePoint, Inc., Blink Charging Co., and hundreds of smaller network operators collectively serving commercial and workplace charging demand.

Market consolidation is proceeding through strategic acquisitions, Blink Charging Co.’s acquisition of SemaConnect (June 2022), ChargePoint, Inc. and General Motors deployment collaboration, as well as the competitive displacement of smaller operators unable to maintain the software, reliability, and brand investment required to sustain commercial network contracts.

Investment & Growth Opportunities

Fastest Growing Segments

Level 3 DC fast charging (~35.2% CAGR), commercial fleet depot charging (~32% CAGR), retail and hospitality destination charging (~30% CAGR), and bidirectional V2G-enabled charging hardware (~45%+ CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address a combined USD 25+ billion addressable market opportunity within the US EV charging ecosystem by 2030.

Emerging Market Expansion

The Midwest's below-average 16.2% market share relative to its EV adoption trajectory creates a catch-up investment opportunity as major OEM EV launches drive EV adoption among Midwest automotive workers receiving employee pricing incentives. Wisconsin opened a new NEVI funding round on May 27, 2026, with around USD 40 million available to expand EV fast-charging beyond its completed Alternative Fuel Corridor network.

Venture and Institutional Investment Trends

- The 30C Refueling Infrastructure Tax Credit provides up to 30% credit for qualified EV charging and alternative fuel refueling property installed in eligible low-income or non-urban census tracts. Eligible property includes EV charging ports, fuel dispensers, energy storage, and essential installation components.

- Private equity and infrastructure fund interest in US EV charging assets has increased dramatically in 2024–2025. Infrastructure fund interest is driven by the NEVI program's revenue floor guarantee, Buy America hardware requirements that favor US-domiciled operators, and the long-duration asset profile of utility-grade charging infrastructure that aligns with infrastructure fund return requirements.

Future Market Outlook (2026-2034)

The United States EV charging station market is positioned for extraordinary expansion through 2034. From a base of USD 3.20 Billion in 2025, the market is projected to reach USD 34.20 Billion by 2034, representing total incremental value creation of USD 31.0 billion at a CAGR of 28.60%.

This growth is underpinned by the federal NEVI deployment mandate, the IRA's decade-long tax credit commitment, the non-discretionary fleet electrification programs of major US employers, and the compounding EV fleet expansion that creates self-reinforcing charging infrastructure investment demand as each new EV adds to the national charging demand baseline.

By 2034, Level 3 DCFC will grow from 34.2% to approximately 45% of market share as highway corridor deployment completes and urban fast charging hub density reaches commercial-scale utilization. Commercial applications will retain 65%+ market share as fleet depot and retail charging drive the majority of deployment activity, while residential charging infrastructure density grows with the EV-owning homeowner population.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 100 industry participants in 2024–2025, including EV charging network operators, EVSE hardware manufacturers, utility EV program managers, federal and state transportation officials, commercial real estate charging operators, and institutional investors across California, Texas, New York, and Florida.

Secondary Research

Secondary research encompassed AFDC Alternative Fuels Data Center public charging port data, DOE Joint Office of Energy and Transportation NEVI program reports, NHTSA CAFE and ZEV mandate filings, Edison Electric Institute EV outlook, company SEC filings and investor presentations, IRA and IIJA legislative text and Treasury guidance, and industry publications.

Forecasting Models

Market size estimations incorporated US EV fleet growth projections, per-EV charging infrastructure demand ratios, EVSE average selling price trajectories by charging level, utilization-based network revenue modeling, and vendor revenue disclosures. A base-case CAGR of 28.60% reflects consensus estimates validated against NEVI deployment schedules, IRA tax credit utilization rates, and announced commercial charging investment programs from FY2020 to FY2025.

United States Electric Vehicle Charging Station Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Charging Station Types Covered | AC Charging, DC Charging, Inductive Charging |

| Vehicle Types Covered | Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV) |

| Installation Types Covered | Portable Charger, Fixed Charger |

| Charging Levels Covered | Level 1, Level 2, Level 3 |

| Connector Types Covered | Combines Charging Station (CCS), CHAdeMO, Normal Charging, Tesla Supercharger, Type-2 (IEC 621196), Others |

| Applications Covered | Residential, Commercial |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | ChargePoint, Inc., Tesla, EVgo Services LLC, Blink Charging Co., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States electric vehicle charging station market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States electric vehicle charging station market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States electric vehicle charging station industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Electric Vehicle Charging Station Market Report

The United States electric vehicle charging station market reached USD 3.20 Billion in 2025 and is projected to reach USD 34.20 Billion by 2034.

The market is expected to grow at a CAGR of 28.60% during 2026-2034, driven by federal NEVI and IRA infrastructure investment, surging EV adoption, and corporate fleet electrification programs.

The West region leads with a 36.7% share in 2025, anchored by California's ZEV mandate, the highest US EV penetration rate, and comprehensive state-level EVCS incentive programs.

Commercial applications dominate with a 63.4% share in 2025, encompassing workplace, retail, highway, hospitality, and fleet depot charging driven by IRA tax credits and corporate sustainability mandates.

Level 2 holds the largest share at 49.5%, valued for its cost-effective installation and suitability for commercial destinations and workplace charging where vehicles park for extended dwell times.

Some of the key players include ChargePoint, Inc., Tesla, EVgo Services LLC, and Blink Charging Co.

Level 3 is growing at ~35.2% CAGR due to the NEVI program's 150+ kW highway corridor mandate, Tesla Supercharger open-network expansion to all NACS-compatible EVs, and commercial operators deploying ultra-fast charging hubs to capture premium highway charging revenue.

Key challenges include high grid upgrade costs for DCFC installations, interconnection queue delays of 18–36 months in constrained markets, and electrician workforce shortages constraining deployment velocity.

Charging-as-a-Service models, retail and big-box destination charging hubs, and medium and heavy-duty truck charging infrastructure represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)