Weather App Market Size, Share, Trends and Forecast by Marketplace and Region, 2026-2034

Weather App Market Size, Share, Trends & Forecast (2026-2034)

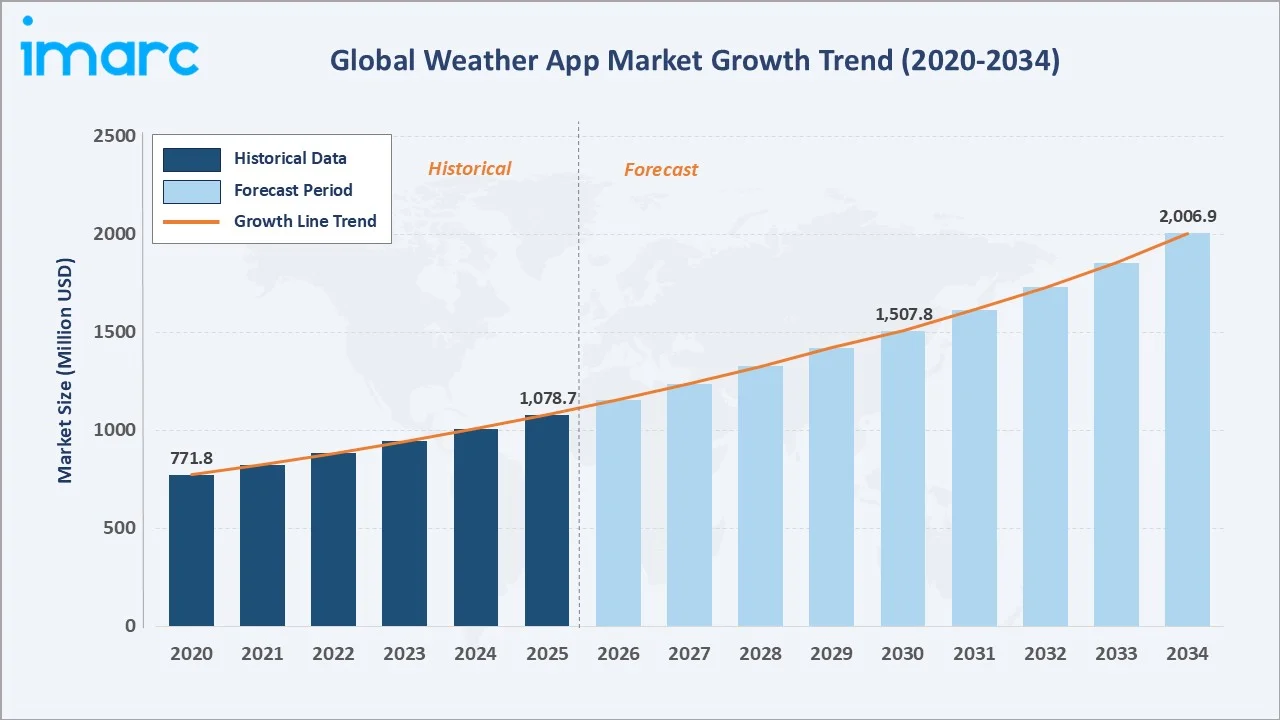

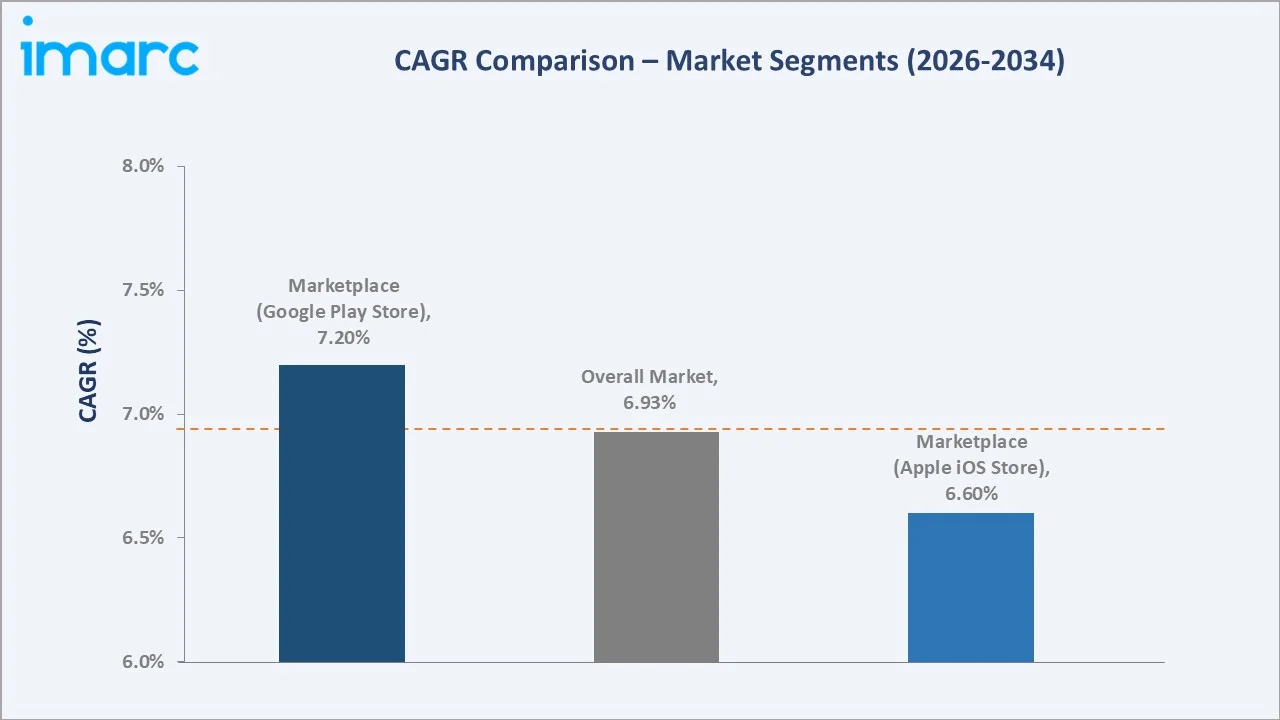

The global weather app market reached USD 1,078.7 Million in 2025 and is projected to reach USD 2,006.9 Million by 2034, growing at a CAGR of 6.93% during 2026-2034. The market is driven by the rapid proliferation of smartphones globally, rising demand for accurate real-time weather intelligence, and the growing integration of artificial intelligence and machine learning into weather forecasting platforms.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,078.7 Million |

|

Forecast Market Size (2034) |

USD 2,006.9 Million |

|

CAGR (2026-2034) |

6.93% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

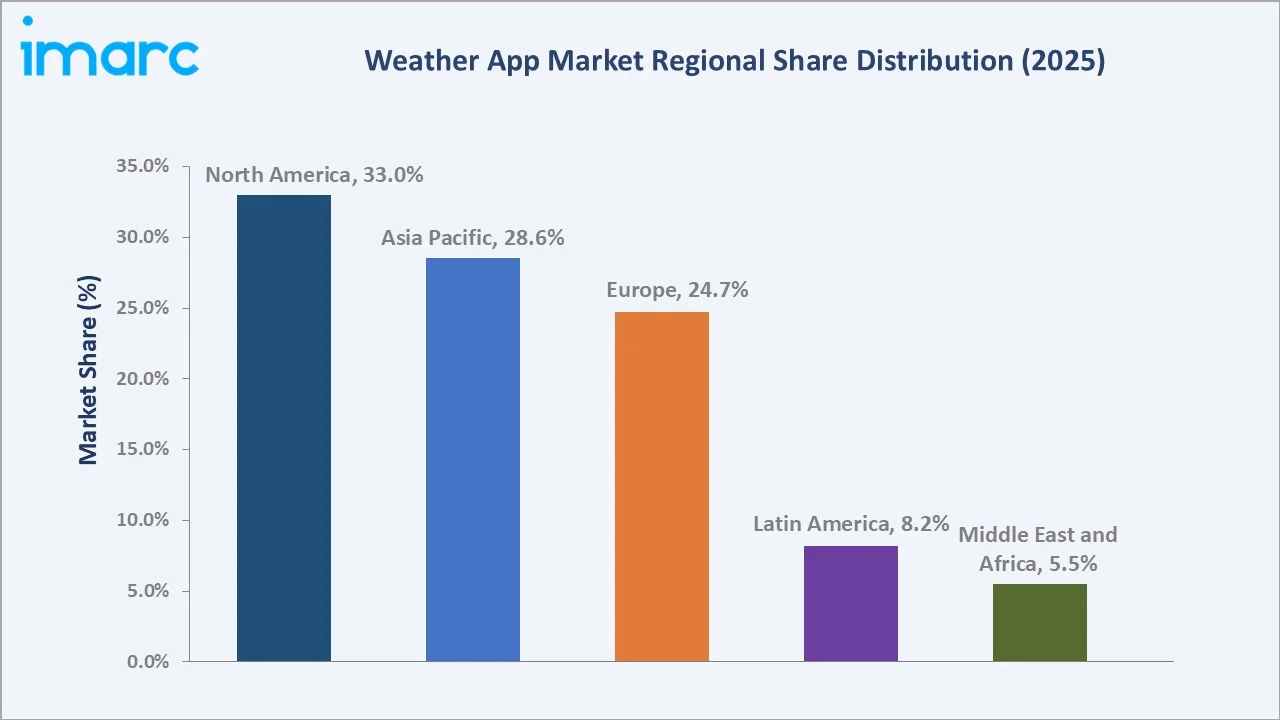

North America (33.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

North America leads all regions with a 33.0% share in 2025, while Google Play Store commands the largest marketplace position at 58.9% due to the dominant global penetration of Android devices. The weather app market growth is further accelerated by increasing climate change awareness, growing reliance on weather data across agriculture, aviation, logistics, and outdoor event sectors, and monetization innovations through freemium and subscription revenue models.

To get more information on this market, Request Sample

North America dominates the global weather app market, holding a 33.0% share in 2025, supported by widespread smartphone penetration, advanced mobile infrastructure, and a strong culture of app usage for daily planning. Google Play Store commands the largest marketplace share at 58.9% in 2025, reflecting the massive global Android user base.

The weather app market forecast through 2034 is shaped by continuous advancements in AI-powered hyper-local forecasting, increasing wearable device integration, and the proliferation of sector-specific weather intelligence APIs targeting agriculture, logistics, and insurance industries.

Executive Summary

The global weather app market is experiencing sustained expansion, underpinned by accelerating smartphone adoption, rising consumer reliance on real-time weather data, and the growing application of AI-driven forecasting across consumer and enterprise segments. The market reached USD 1,078.7 Million in 2025 and is forecast to reach USD 2,006.9 Million by 2034, reflecting a robust CAGR of 6.93% over the forecast period.

North America leads globally with a 33.0% share in 2025, driven by high smartphone penetration, advanced mobile infrastructure, and enterprise adoption of weather data APIs. Asia Pacific follows with 28.6%, fueled by the massive Android user base in China, India, and Southeast Asia, and rapid digital adoption.

Europe contributes 24.7%, with a focus on premium weather services and climate monitoring applications. Google Play Store dominates the marketplace segment at 58.9% in 2025, while Apple iOS Store holds 32.4%. Key players, including AccuWeather, Inc., DTN, OpenWeather, Windyty SE, and ACME AtronOmatic, continue to invest in AI features, hyper-local forecasting, and cross-platform distribution strategies.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Marketplace) |

Google Play Store – 58.9% share (2025) |

|

Second Segment (Marketplace) |

Apple iOS Store – 32.4% (2025) |

|

Leading Region |

North America – 33.0% share (2025) |

|

Fastest Growing Region |

Asia Pacific (Android penetration + digital adoption) |

|

Top Companies |

AccuWeather, Inc., DTN, OpenWeather, Windyty SE, and ACME AtronOmatic |

Key Analytical Observations:

- Google Play Store accounts for 58.9% of the weather app market in 2025, driven by the global Android user base exceeding 3.9 billion active devices, with weather apps ranking consistently among the top-10 most downloaded utility application categories.

- North America leads the weather app market with a 33.0% share in 2025, supported by In 2024, the global number of smartphone users reached 4.88 billion, representing approximately 60.42% of the world’s population, according to BankMyCell.

- The weather app market trends reflect accelerating AI adoption, with leading platforms deploying machine learning models that deliver street-level, minute-by-minute forecasts significantly improving accuracy compared to traditional numerical weather prediction methods.

- Asia Pacific is the fastest-growing region, with mobile penetration in the Asia Pacific region expected to reach 70% by 2030, slightly below the global average of 73% for the same year, directly expanding the addressable market for weather app downloads and in-app subscription revenues.

- The weather app market growth is supported by enterprise demand for weather intelligence APIs in agriculture, logistics, aviation, and insurance sectors, with B2B data licensing emerging as the highest-margin revenue stream for leading operators.

Global Weather App Market Overview

Weather applications are mobile software platforms that aggregate, process, and present meteorological data to consumers and enterprises in real time. Originally limited to basic temperature and precipitation forecasts, modern weather apps have evolved into sophisticated AI-powered intelligence platforms delivering hyper-local forecasts, severe weather alerts, air quality indices, pollen counts, UV radiation readings, and sector-specific climate analytics.

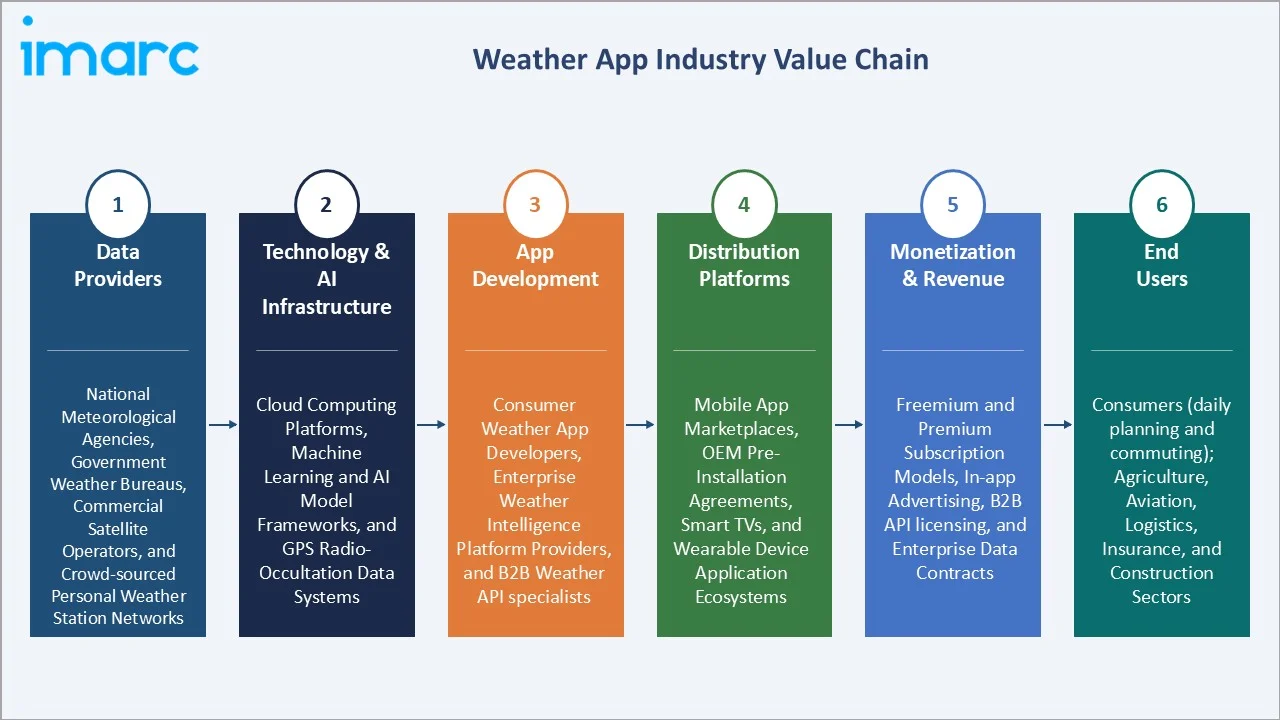

The market ecosystem spans raw data providers (national meteorological agencies, commercial satellites, IoT sensor networks), AI model developers, app publishers, distribution platforms, and end users spanning consumers, enterprises, and government agencies.

The proliferation of smartphones and ubiquitous mobile internet access has transformed weather apps into essential daily utilities. The ITU estimates that by 2025, around 6 billion people, or 74% of the global population, will be using the internet, with weather information ranking among the top three daily digital search activities globally.

The weather app market forecast is further shaped by the integration of IoT weather sensors, connected vehicle data streams, and commercial satellite constellations that are enabling unprecedented spatial and temporal resolution in consumer and enterprise weather forecasting products.

Market Dynamics

To evaluate market opportunities, Request Sample

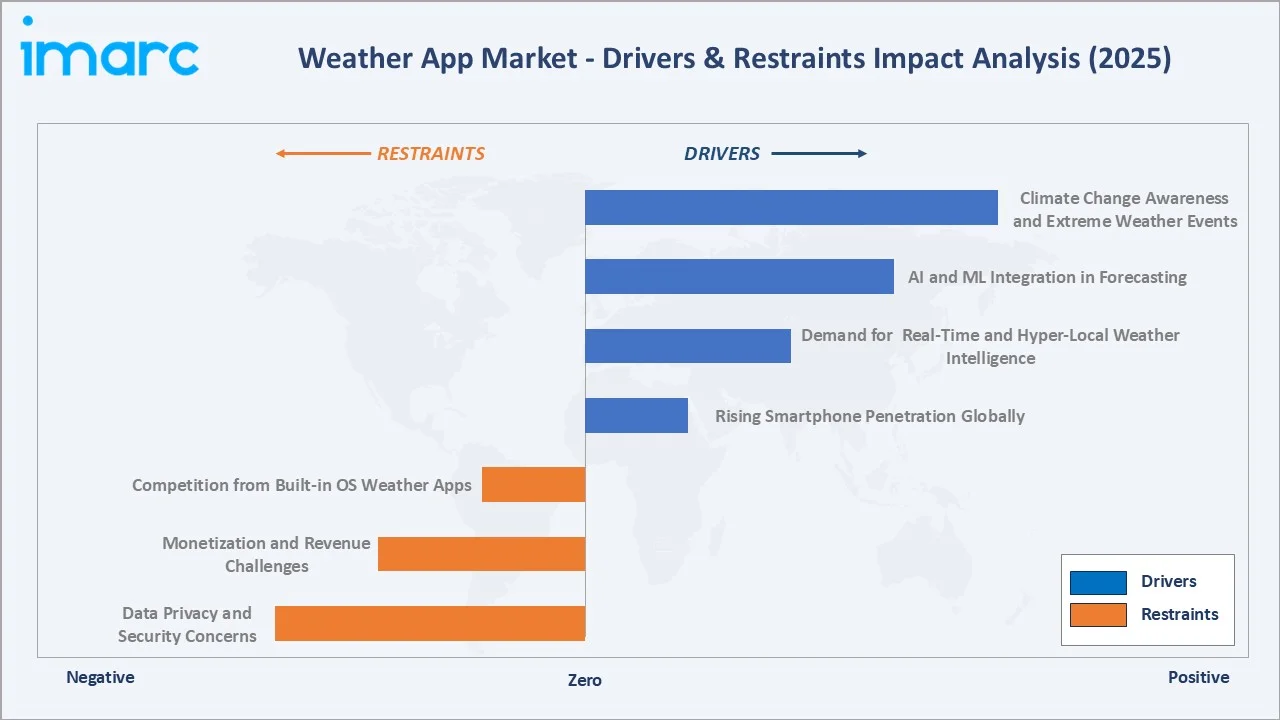

Market Drivers

- Rising Smartphone Penetration Globally: The number of smartphones surpassed 7.21 billion in 2024 and is projected to exceed 8.06 billion by 2029, directly expanding the addressable download market for weather applications. In emerging economies across South Asia, Southeast Asia, and Sub-Saharan Africa.

- Demand for Real-Time and Hyper-Local Weather Intelligence: According to IATA, weather-related disruptions cost global aviation a large sum annually, driving airline operators to adopt real-time weather intelligence platforms. Agriculture, logistics, and outdoor event management sectors are similarly increasing investment in precision weather data services.

- AI and ML Integration in Forecasting: Machine learning models trained on satellite imagery, radar data, and IoT sensor feeds are dramatically improving forecast accuracy at hyperlocal resolution. Leading operators have demonstrated 30-40% improvements in short-range forecast accuracy compared to traditional numerical weather prediction models, increasing user engagement and driving premium subscription conversion rates across consumer and enterprise weather app platforms.

- Climate Change Awareness and Extreme Weather Events: The increasing frequency and severity of extreme weather events are driving consumers and enterprises to adopt weather apps as critical safety and operational planning tools. According to research by Climate Central, in 2025, there were 23 weather and climate disasters, each causing at least USD 1 billion in damages, reinforcing consumer reliance on real-time weather alerts and emergency notification systems delivered through mobile weather applications.

Market Restraints

- Data Privacy and Security Concerns: Weather apps typically require persistent access to user location data to deliver personalized forecasts. Tightening data privacy regulations, including GDPR in Europe and CCPA in California, impose compliance costs on app developers and restrict location data monetization strategies, particularly for advertising-driven freemium revenue models.

- Monetization and Revenue Challenges: Despite high download volumes, converting free users to paid subscriptions remains challenging. Industry conversion rates for weather app premium subscriptions average below 5%, constraining revenue growth for operators that rely primarily on consumer subscription revenues rather than B2B data licensing.

- Competition from Built-in OS Weather Apps: Apple Weather and Google Weather, pre-installed on iOS and Android devices, respectively, provide competitive baseline functionality that reduces the urgency for consumers to download third-party weather apps.

Market Opportunities

- B2B Weather Data API Licensing: Enterprises across agriculture, insurance, logistics, construction, and energy are increasingly embedding weather intelligence APIs into operational software platforms. The B2B weather data market represents the highest-margin growth opportunity, with average contract values 10-50 times higher than individual consumer subscriptions.

- Wearable Device and Smart Home Integration: Smartwatch weather apps, connected vehicle displays, and smart home voice assistant integrations represent a rapidly expanding distribution channel. Apple Watch weather apps and Amazon Echo weather skills are driving new engagement touchpoints that extend weather app utility beyond smartphone screens.

Market Challenges

- Forecast Accuracy and User Trust: Inaccurate forecasts damage user trust and drive app uninstalls. Maintaining forecast accuracy across diverse geographies and weather scenarios requires continuous investment in data infrastructure, model training, and quality assurance, representing a significant operational cost burden for mid-tier weather app operators.

- Regulatory Fragmentation Across Markets: Diverging data localization laws, app store policies, and advertising regulations across key markets, including China, India, and the EU, create compliance complexity for global weather app operators, increasing the cost of international market expansion.

Emerging Market Trends

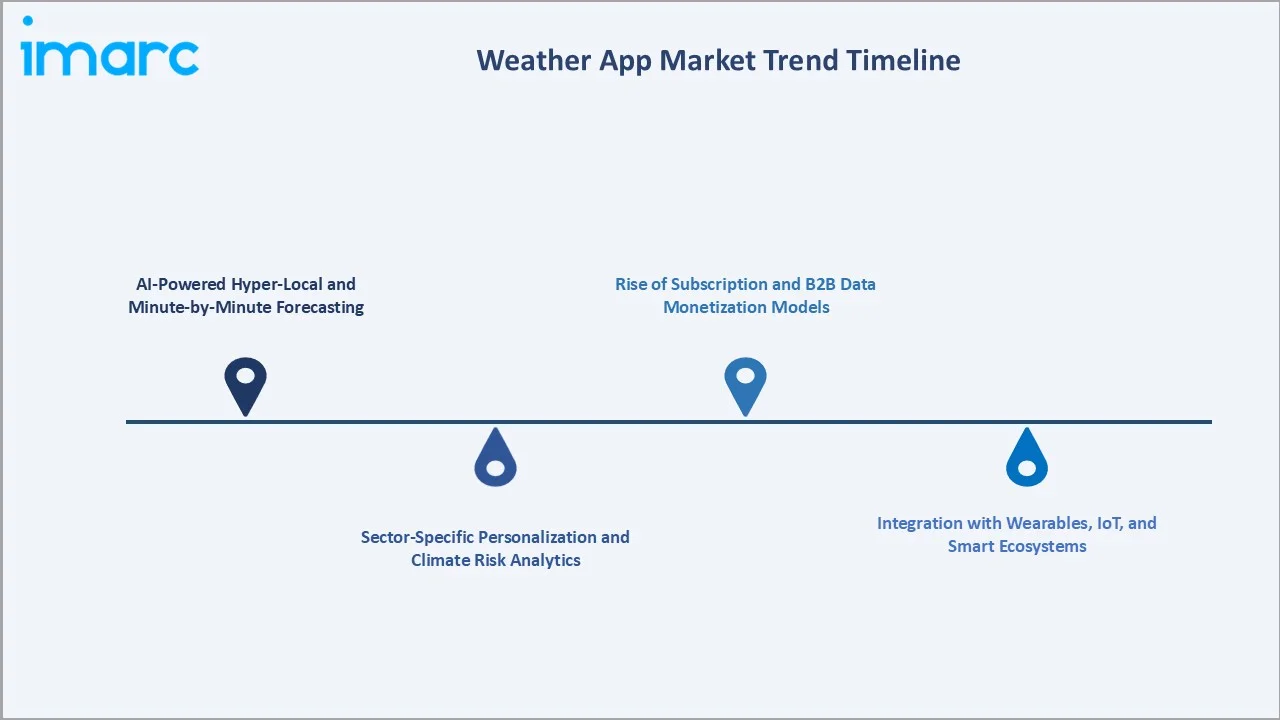

1. AI-Powered Hyper-Local and Minute-by-Minute Forecasting

In September 2024, IBM and NASA released an open‑source AI foundation model on Hugging Face designed for weather and climate applications, enabling higher‑resolution localized forecasts, improved climate projections, and better analysis of severe weather patterns. The model can be fine‑tuned for various scientific and operational uses, supporting researchers and developers to better analyze and predict severe weather events.

2. Rise of Subscription and B2B Data Monetization Models

Weather app monetization is undergoing a fundamental structural shift from advertising-dependent freemium models toward premium subscription tiers and B2B data licensing partnerships. The weather app market trends in B2B monetization are expected to accelerate as enterprises across climate-sensitive industries recognize weather intelligence as a critical operational input, positioning API licensing as a USD 800 million+ sub-market within the broader weather app ecosystem by 2030.

3. Integration with Wearables, IoT, and Smart Ecosystems

According to the latest data from IDC's Worldwide Wearable Device Tracker, global wearable device shipments increased by 9.1% year-on-year in 2025, reaching a total of 611.5 million units.

With weather functionality consistently ranking among the three most-used built-in features, representing a significant new distribution surface for weather app publishers to embed their forecasting capabilities.

4. Sector-Specific Personalization and Climate Risk Analytics

Leading weather app operators are moving beyond generic consumer forecasting toward deeply personalized, sector-specific weather intelligence platforms that deliver decision-relevant insights tailored to individual professional and lifestyle contexts. Precision agriculture weather apps now integrate soil moisture sensors, evapotranspiration models, and crop-specific growth stage forecasts to guide irrigation, planting, and harvest timing decisions.

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Data Providers |

National meteorological agencies, government weather bureaus, commercial satellite operators, and crowd-sourced personal weather station networks. |

|

Technology & AI Infrastructure |

Cloud computing platforms, machine learning and AI model frameworks, and GPS radio-occultation data systems. |

|

App Development |

Consumer weather app developers, enterprise weather intelligence platform providers, and B2B weather API specialists. |

|

Distribution Platforms |

Mobile app marketplaces, OEM pre-installation agreements, smart TVs, and wearable device application ecosystems. |

|

Monetization & Revenue |

Freemium and premium subscription models, in-app advertising, B2B API licensing, and enterprise data contracts. |

|

End Users |

Consumers (daily planning and commuting); agriculture, aviation, logistics, insurance, and construction sectors. |

Technology Landscape in the Weather App Industry

AI and Deep Learning Forecast Models

Next-generation weather apps are powered by convolutional neural networks and transformer-based deep learning architectures trained on decades of historical radar, satellite, and surface observation data. GraphCast forecasts weather conditions up to 10 days in advance with greater accuracy and speed compared to the industry-standard High Resolution Forecast (HRES) system, which is produced by the European Centre for Medium-Range Weather Forecasts (ECMWF).

Commercial Satellite and Radar Networks

The expansion of commercial low-earth-orbit satellite constellations, including Spire Global’s 120+ satellite radio-occultation network is dramatically increasing the volume and spatial coverage of raw weather observation data available to commercial app developers, enabling unprecedented forecast precision in data-sparse regions.

Crowd-Sourced and Personal Weather Station Networks

Weather Underground’s network of over 250,000 personal weather stations globally provides hyperlocal ground-truth data that enhances forecast accuracy at the neighborhood level. App developers increasingly integrate crowd-sourced observation networks alongside official meteorological data to reduce forecast error in dense urban environments where local heat island effects and building-induced wind patterns cannot be captured by regional weather station networks.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Marketplace |

Google Play Store |

58.9% |

2025 |

|

Region |

North America |

33.0% |

2025 |

By Marketplace

Google Play Store dominates the weather app marketplace with a 58.9% share in 2025. Its leadership reflects the overwhelming dominance of Android in global smartphone markets, where Android holds approximately 68.24% of the global mobile operating system market share as of February 2026. The rising number of Android smartphone activations in high-growth markets, including India, Brazil, Indonesia, and Nigeria, is directly expanding the Google Play Store’s addressable base for weather app distribution.

To access detailed market analysis, Request Sample

Apple iOS Store holds a 32.4% share (2025). Despite the smaller absolute user base compared to Android, iOS users demonstrate significantly higher average revenue per user (ARPU) for premium weather app subscriptions, driven by iPhone users’ above-average disposable income levels and higher propensity to pay for app-store purchases.

Regional Market Insights

North America’s market leadership (33.0%, 2025) reflects both high consumer engagement with weather apps and a mature enterprise weather intelligence market. The United States accounts for approximately 53% of North American revenue, supported by the fact that 53% of Americans use weather apps daily, according to recent consumer surveys.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

33.0% |

High smartphone penetration, enterprise API demand, and severe weather alerting |

|

Asia Pacific |

28.6% |

Android growth in India/SEA, agriculture demand, and rapid digitalization |

|

Europe |

24.7% |

Climate change awareness, premium subscription culture, and smart city apps |

|

Latin America |

8.2% |

Rising smartphone adoption, the demand in the agriculture sector, and tourism |

|

Middle East & Africa |

5.5% |

Oil & gas sector demand, infrastructure expansion, and event planning |

Asia-Pacific represents the second-largest regional market for weather apps, accounting for a 28.6% share in 2025, and is positioned as the fastest-growing region through 2034. The region's growth is primarily driven by the massive and expanding Android user base across China, India, Indonesia, Vietnam, and the Philippines, where smartphone adoption continues to accelerate among first-time internet users who rely heavily on weather apps for agricultural planning, daily commuting, and outdoor livelihood decisions.

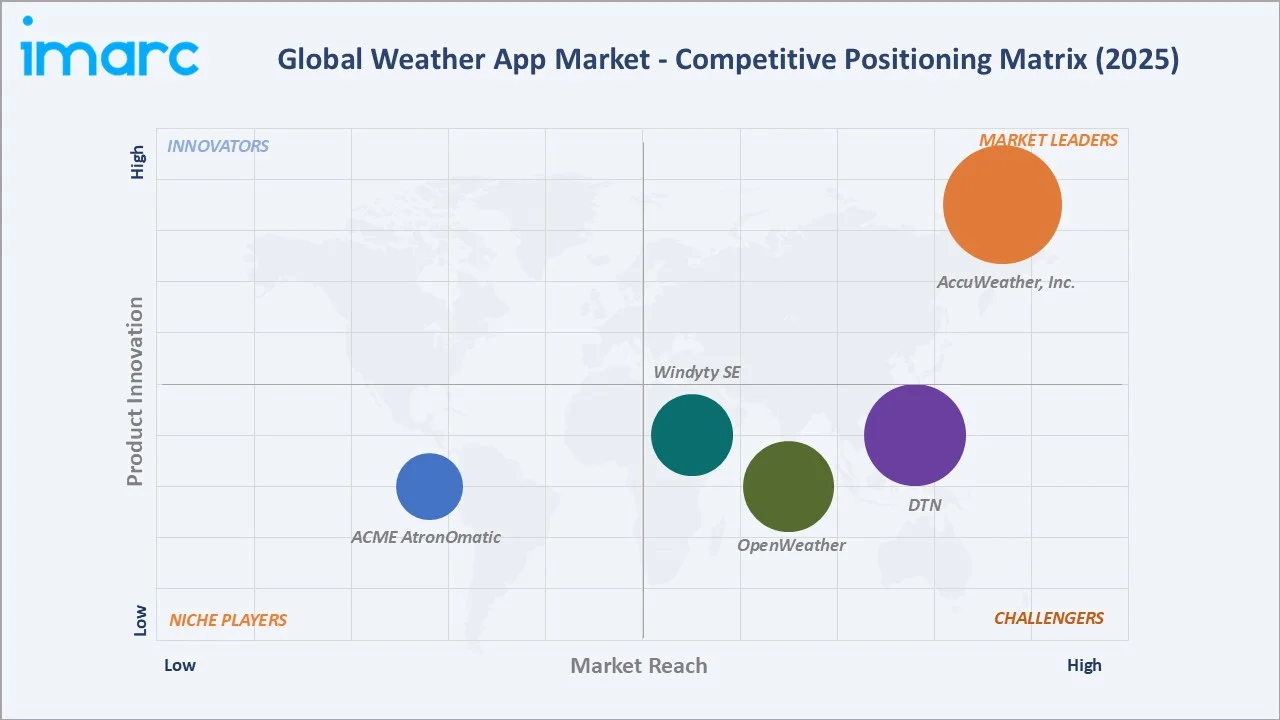

Competitive Landscape

The global weather app market exhibits a moderately fragmented structure. The leading operators, AccuWeather, Inc., OpenWeather, and DTN collectively hold approximately 40–48% of global market revenue in 2025.

|

Company |

Brand/ Platform/ Programs |

Market Position |

Core Strength |

|

AccuWeather, Inc. |

AccuWeather |

Market Leader |

World's largest commercial weather media company; 1.5 billion users; patented MinuteCast minute-by-minute precision |

|

DTN |

DTN Weather Hub |

Strong Challenger |

B2B enterprise specialist; agriculture, energy, and logistics weather API leader |

|

OpenWeather |

OpenWeather |

Challenger |

Developer-first, self-service global weather API platform serving 6+ million customers |

|

Windyty SE |

Windy.com |

Challenger |

Visual meteorological platform; 50M+ users; popular with aviation, marine, and outdoor professional audiences |

|

ACME AtronOmatic |

MyRadar |

Niche Player |

Radar-focused consumer app; iOS and Android; 50M+ downloads |

A diverse ecosystem of specialized operators, including Windyty SE and ACME AtronOmatic, serves niche segments across premium consumer, aviation, sailing, and outdoor sports use cases.

Key Company Profiles

AccuWeather, Inc.

AccuWeather, headquartered in Pennsylvania, is the world’s largest commercial weather media company, serving 1.5 billion users worldwide through consumer apps, enterprise APIs, and media broadcast services. Its MinuteCast technology delivers minute-by-minute precipitation forecasts at individual address resolution.

- Product Portfolio: AccuWeather consumer app (iOS and Android).

- Recent Developments: In August 2025, AccuWeather, Inc. launched an improved version of its mobile app with over 50 new and enhanced features, including upgraded radar maps and exclusive lightning alerts to keep users safer and better informed.

- Strategic Focus: Enterprise API expansion; AI accuracy leadership; global emerging market user acquisition through localized app experiences.

DTN

DTN, headquartered in Bloomington, Minnesota, is a leading provider of high-precision weather intelligence solutions for agriculture, energy, transportation, and aviation enterprises. DTN operates a proprietary weather observation network comprising over 70,000 ground stations across North America.

- Product Portfolio: DTN Weather Hub

- Recent Developments: In January 2026, DTN launched its Weather Hub for outdoor safety to help outdoor safety leaders and event organizers turn real‑time weather intelligence into actionable safety decisions. It delivers centralized, hyper‑local forecasts and alerts to support rapid responses for live events, public safety operations, and emergency planning.

- Strategic Focus: B2B enterprise expansion; climate risk analytics product development; precision agriculture weather intelligence leadership.

Market Concentration Analysis

The weather app market exhibits moderate fragmentation, with the top four global operators controlling approximately 40–48% of total revenue in 2025. A long tail of 200+ specialized weather app developers serves niche verticals and geographic markets, maintaining a highly competitive landscape below the tier-one operators. App store distribution democratizes market access, enabling well-funded startups and specialized operators to compete effectively against established players in specific feature categories or user segments.

Consolidation activity is increasing, driven by the high cost of proprietary weather data infrastructure, AI model development investment requirements, and enterprise sales capabilities needed to compete in the B2B API market. Between 2020 and 2024, three significant acquisitions reshaped the competitive landscape, as established technology platforms sought to acquire specialized weather intelligence capabilities.

Investment & Growth Opportunities

Fastest Growing Segments

B2B enterprise weather API licensing (estimated CAGR 9.5%), AI-powered hyper-local consumer premium subscriptions (CAGR 8.2%), and wearable/IoT weather integrations (CAGR 11.0%) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable sub-market of approximately USD 800 million by 2030.

Emerging Market Expansion

India, Indonesia, Nigeria, and Brazil collectively represent an incremental USD 320 million weather app revenue opportunity by 2034, driven by rapid smartphone adoption and growing agricultural and logistics sector demand for weather intelligence. Entry via Android-first app development, regional language localization, and low-data-usage app architectures are the preferred investment strategies for capturing this emerging market growth.

Venture and Institutional Investment Trends

- Key investment themes include AI-powered climate risk analytics, commercial weather satellite data networks, precision agriculture weather APIs, and parametric insurance weather triggers.

- Strategic investors from agriculture technology, insurance, logistics, and smart city sectors are acquiring weather intelligence capabilities, viewing accurate weather data as critical operational infrastructure rather than a standalone product category.

Future Market Outlook (2026-2034)

The global weather app market is positioned for sustained, broad-based growth through 2034. From a base of USD 1,078.7 Million in 2025, the market is projected to reach USD 2,006.9 Million by 2034, representing total incremental value creation of approximately USD 928.2 Million over the forecast decade, at a CAGR of 6.93%.

Three structural macro-themes underpin this trajectory: the continued global proliferation of internet-connected mobile devices; the escalating economic cost of weather-related disruptions across climate-sensitive industries, driving enterprise demand for precision weather intelligence; and the rapid maturation of AI and satellite-based forecasting technologies that are fundamentally improving the accuracy and granularity of weather predictions available to app developers. The weather app market outlook through 2034 strongly favors operators that achieve differentiated AI forecasting capabilities, diversified B2B revenue streams, and global distribution reach across both Android and iOS ecosystems.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 100 industry participants in 2024–2025, including weather app product managers, enterprise weather data buyers, mobile platform developers, meteorological technology specialists, and end users across North America, Europe, and the Asia Pacific.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, app store analytics platforms (App Annie, Sensor Tower), meteorological agency publications (NOAA, ECMWF, WMO), industry publications (Weather Business, Weatherwise), regulatory filings, and publicly available financial data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating global smartphone penetration rates, app download volume trends, average revenue per user benchmarks by market segment, and historical market evolution data from 2020 to 2025.

Weather App Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Marketplaces Covered | Google Play Store, Apple iOS Store, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AccuWeather, Inc., DTN, OpenWeather, Windyty SE, ACME AtronOmatic, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the weather app market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global weather app market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the weather app industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Weather App Market Report

The global weather app market reached USD 1,078.7 Million in 2025. It is projected to reach USD 2,006.9 Million by 2034.

The weather app market is expected to grow at a CAGR of 6.93% during the forecast period from 2026-2034, driven by rising smartphone penetration and growing demand for AI-powered weather intelligence.

North America leads the market with a 33.0% share in 2025, supported by high smartphone penetration, advanced digital infrastructure, and strong enterprise weather data adoption.

Google Play Store dominates the marketplace segment with a 58.9% share in 2025 (approx. USD 635.3 Million), reflecting the global dominance of Android devices.

Key drivers include rising global smartphone penetration, growing demand for real-time and hyper-local weather intelligence, AI and ML integration in forecasting, increasing climate change awareness, and expanding B2B enterprise adoption of weather data APIs.

Key players include AccuWeather, Inc., DTN, OpenWeather, Windyty SE, and ACME AtronOmatic.

Key challenges include data privacy and location data regulatory compliance, forecast accuracy maintenance, monetization conversion barriers for free users, and competition from pre-installed OS weather applications on iOS and Android devices.

High-value opportunities include B2B enterprise weather API licensing, AI-powered precision agriculture and logistics weather platforms, commercial satellite weather data networks, and parametric insurance weather trigger systems, particularly in high-growth markets across Asia Pacific and Latin America.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)