Weather Forecasting Services Market Size, Share, Trends and Forecast by Forecasting Type, Purpose, Organization Size, End User, and Region, 2026-2034

Weather Forecasting Services Market Size, Share, Trends & Forecast (2026-2034)

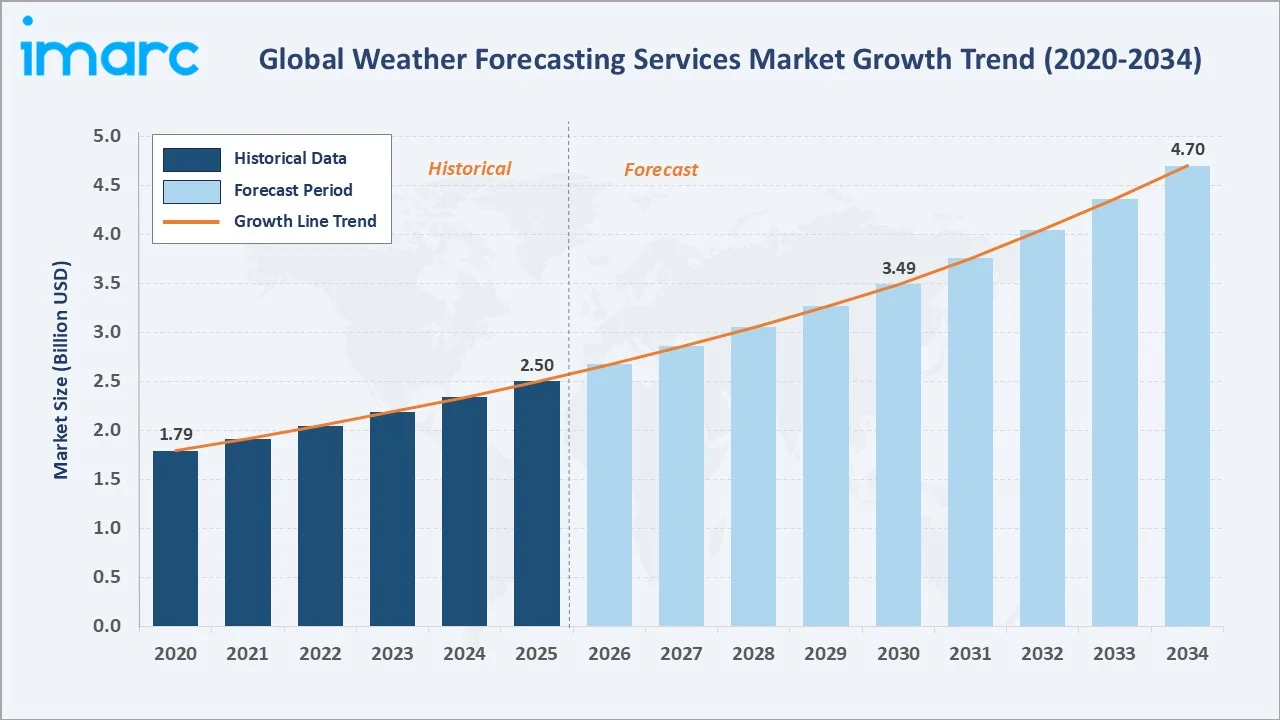

The global weather forecasting services market reached USD 2.50 Billion in 2025 and is projected to reach USD 4.70 Billion by 2034, growing at a CAGR of 6.90% during 2026-2034. The market is driven by the escalating frequency of extreme weather events resulting from climate change, rapid integration of artificial intelligence and machine learning into numerical weather prediction models, and surging demand for precision weather intelligence across agriculture, aviation, energy, logistics, and disaster management sectors.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.50 Billion |

|

Forecast Market Size (2034) |

USD 4.70 Billion |

|

CAGR (2026-2034) |

6.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (28.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

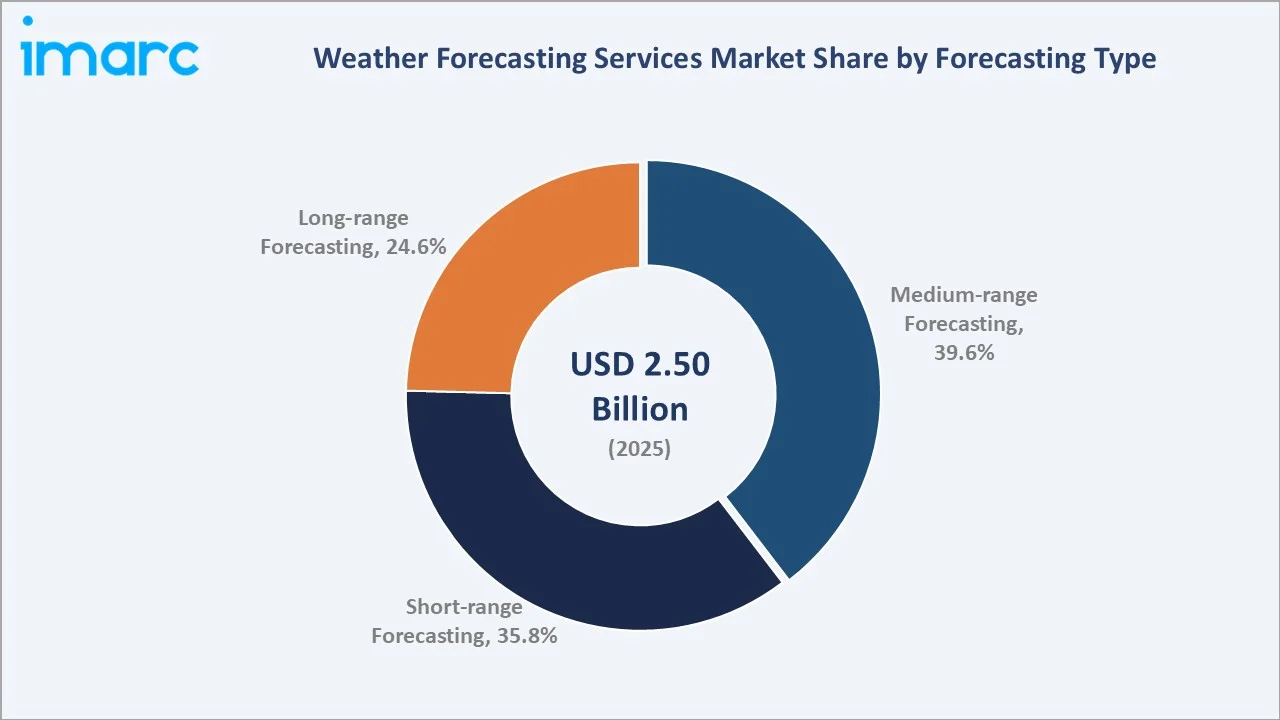

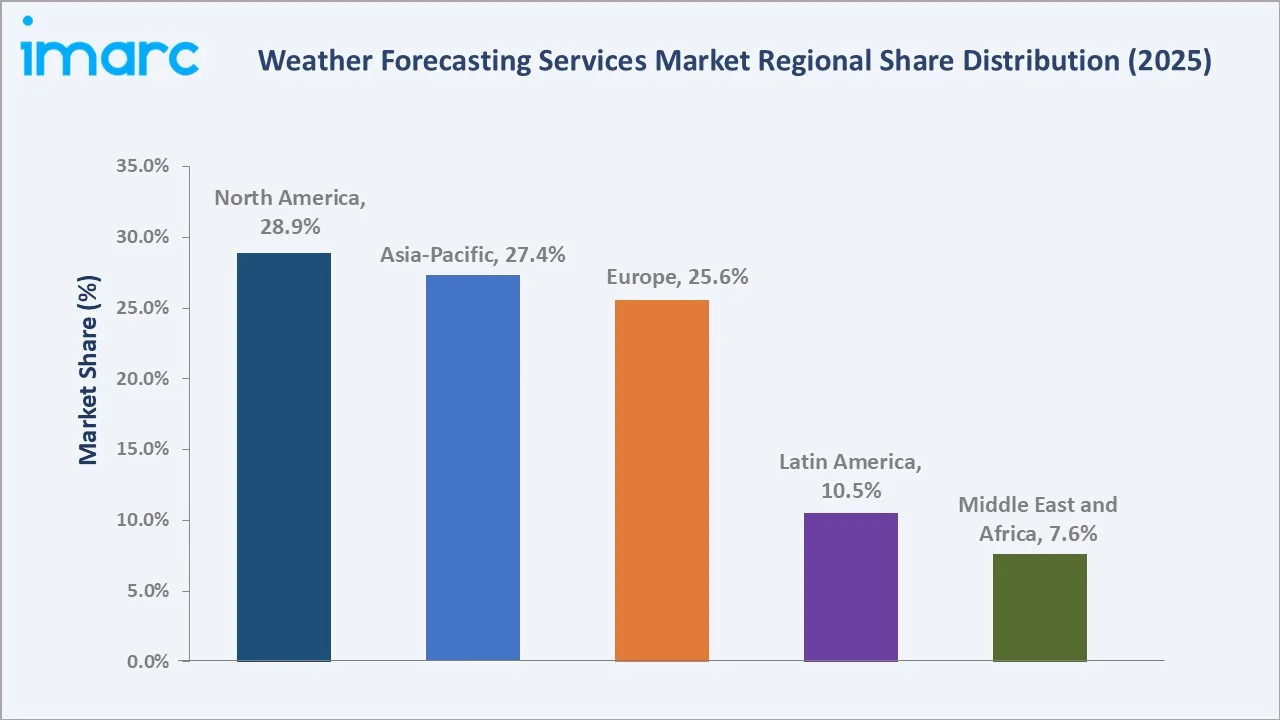

North America leads all regions with a 28.9% share in 2025, while medium-range forecasting commands the largest segment position at 39.6% due to its optimal balance between accuracy and operational planning horizons.

To get more information on this market, Request Sample

North America’s market leadership (28.9%, 2025) is underpinned by advanced national meteorological infrastructure, NOAA’s open data policy enabling commercial innovation, and strong enterprise adoption of weather intelligence APIs across agriculture, insurance, and logistics. Medium-range forecasting holds the largest share at 39.6%, driven by its practical utility for industries requiring 3–10 day operational planning.

Executive Summary

The global weather forecasting services market is experiencing sustained growth, driven by the intersection of climate change acceleration, AI-powered forecast innovation, and expanding enterprise demand for precision weather intelligence. The market reached USD 2.50 Billion in 2025 and is forecast to reach USD 4.70 Billion by 2034, reflecting a robust CAGR of 6.90% over the forecast period.

North America leads globally with a 28.9% share in 2025, driven by advanced meteorological infrastructure and strong commercial weather data adoption. Asia-Pacific follows with 27.4%, propelled by rapid digitalization, expanding agriculture and aviation sectors, and government investments in weather monitoring networks.

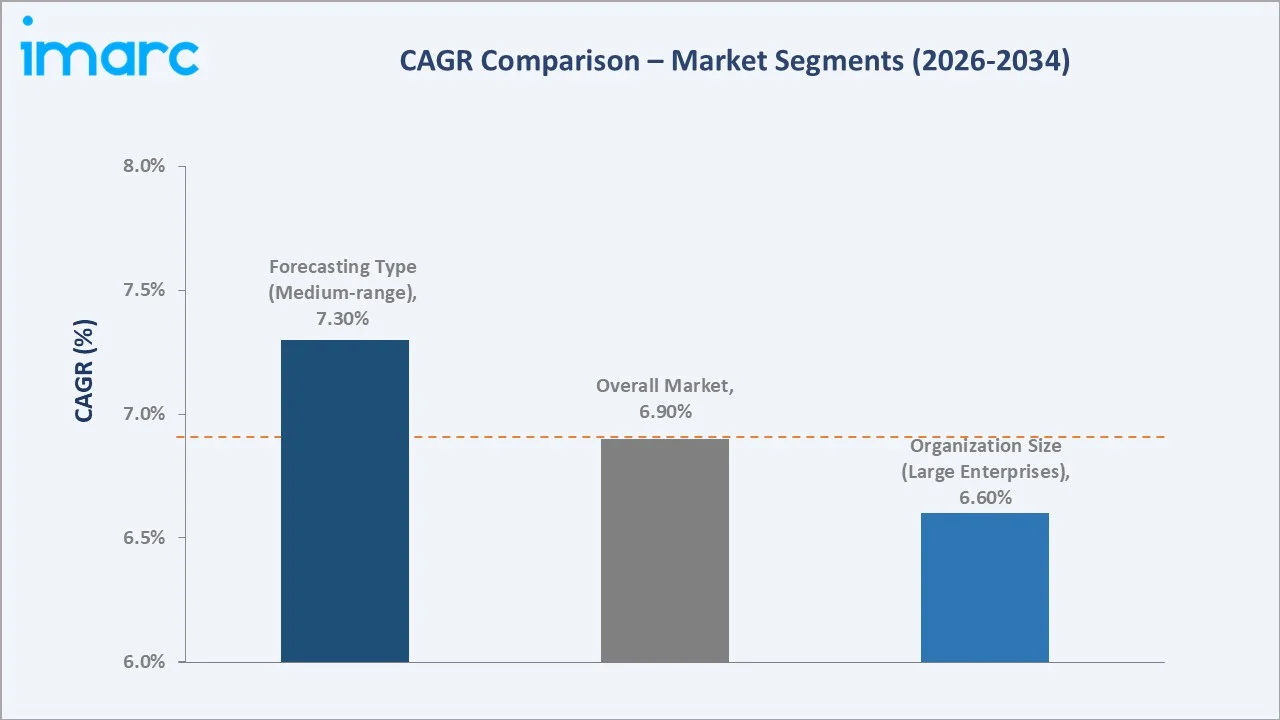

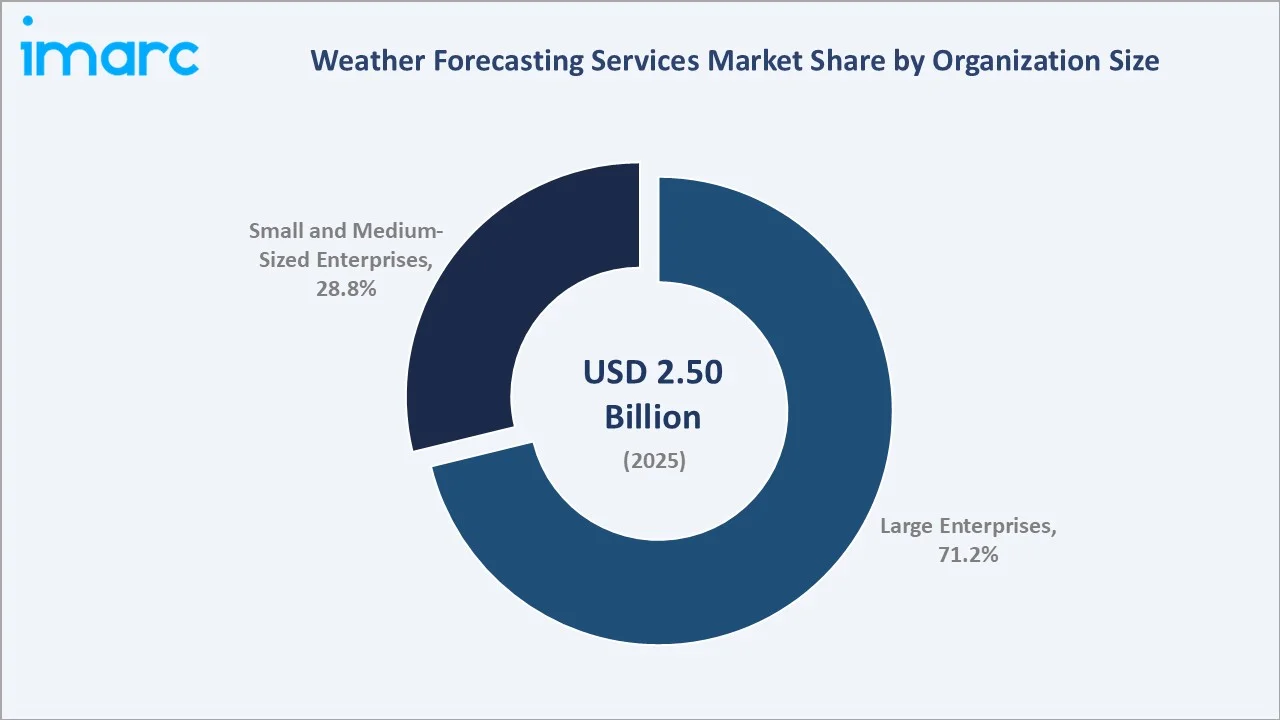

Medium-range forecasting dominates the forecasting type segment at 39.6%, while large enterprises account for 71.2% of the organization size segment due to their extensive operational need for climate intelligence. Key players including AccuWeather, Inc., The Weather Company LLC, Vaisala, DTN, and Spire Global are investing in AI model development, satellite data integration, and B2B API platform expansion.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Forecasting Type) |

Medium-range Forecasting – 39.6% (2025) |

|

Largest Segment (Organization Size) |

Large Enterprises – 71.2% (2025) |

|

Leading Region |

North America – 28.9% share (2025) |

|

Fastest Growing Region |

Asia-Pacific (digitalization + energy sector growth) |

|

Top Companies |

AccuWeather, Inc., The Weather Company LLC, Vaisala, DTN, and Spire Global |

Key Analytical Observations:

- Medium-range forecasting accounts for 39.6% of the market in 2025, favored for its 3–10 day forecast horizon that enables critical operational decisions across agriculture, aviation, logistics, and energy sectors requiring advance planning without sacrificing accuracy.

- Large enterprises hold 71.2% of the market in 2025, reflecting their substantial operational exposure to weather risk and capacity to invest in enterprise-grade weather intelligence platforms, custom API integrations, and dedicated meteorological support services.

- Mission-specific tools, such as ensemble forecasting, Impact-Based Forecasting (IBF), and AI/ML models like 'Mithuna-FS,' have enhanced the accuracy of severe weather predictions by 30-40% over the past decade, according to India Meteorological Department.

- The global renewable energy sector’s rapid expansion is creating a structural new demand driver, as solar and wind farm operators require minute-scale irradiance and wind speed forecasts to optimize grid balancing and maximize energy output.

- The weather forecasting services market growth is reinforced by increasing government contracts for national early warning systems, particularly across South and Southeast Asia, Sub-Saharan Africa, and Latin America where climate vulnerability is highest.

Global Weather Forecasting Services Market Overview

Weather forecasting services encompass the collection, processing, analysis, and dissemination of atmospheric data to generate actionable meteorological predictions for consumer, enterprise, and government end-users. Spanning short-range nowcasts to seasonal and long-range climate outlooks, the sector has evolved from government meteorological agency monopolies into a diversified commercial market served by AI-native startups, satellite operators, and established data companies.

The escalating economic cost of weather-related disruptions is the most powerful structural driver of market expansion. In 2024, the United States experienced 27 confirmed weather and climate disaster events, each causing losses exceeding USD 1 billion, according to NOAA. Globally, the economic toll of weather events exceeded USD 300 billion in 2024, underscoring the urgent need for precision forecast intelligence that enables enterprises, governments, and communities to implement proactive risk mitigation rather than reactive crisis response.

Market Dynamics

To evaluate market opportunities, Request Sample

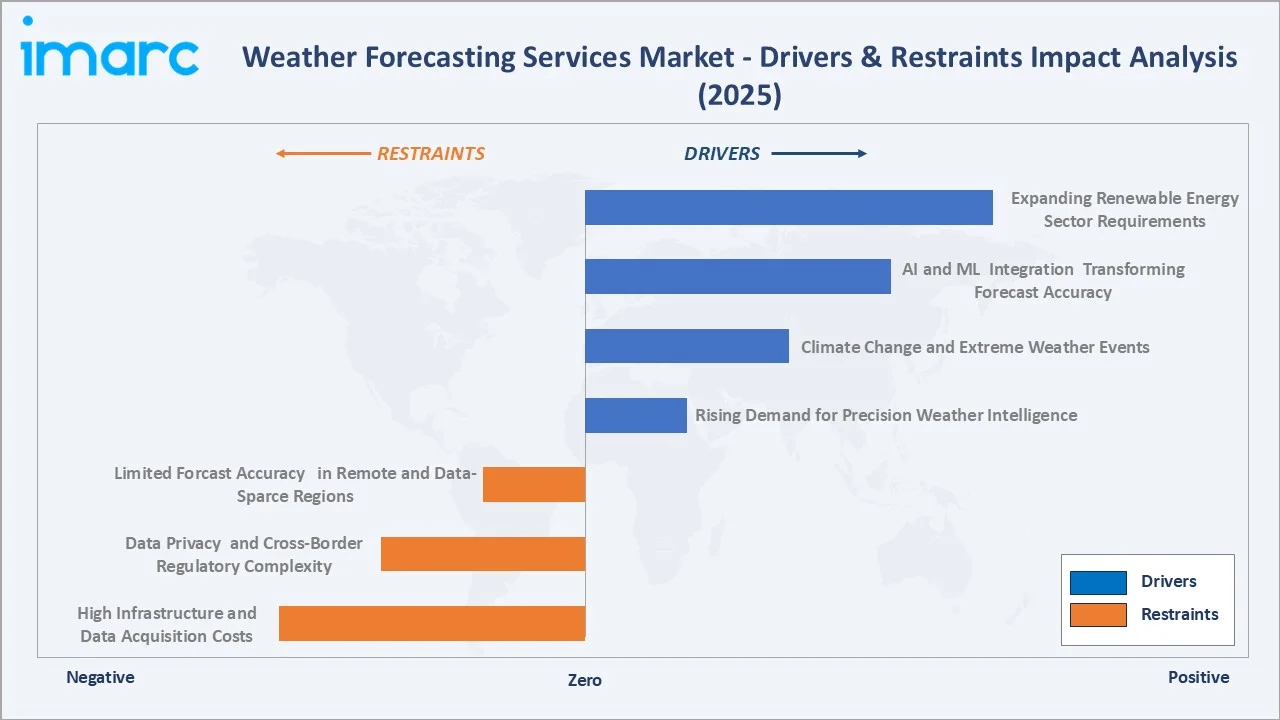

Market Drivers

- Rising Demand for Precision Weather Intelligence: According to a new report by the Food and Agriculture Organization of the United Nations (FAO), disasters have caused an average of USD 99 billion annually. This drives sustained enterprise investment in weather intelligence APIs, dedicated meteorological services, and real-time alert platforms.

- Climate Change and Extreme Weather Events: The intensifying frequency and severity of extreme weather events, hurricanes, heatwaves, wildfires, and severe flooding, is driving unprecedented demand for advanced warning systems across governments, insurers, and businesses.

- AI and ML Integration Transforming Forecast Accuracy: The integration of deep learning architectures and physics-informed neural networks into weather prediction has produced transformative accuracy improvements. DeepMind unveiled GraphCast, an AI model trained on decades of historical weather data that can generate highly accurate global 10‑day forecasts in under a minute.

- Expanding Renewable Energy Sector Requirements: The global solar and wind power capacity is expected to triple by 2030 under net-zero pathways, creating massive new demand for hyper-local, minute-scale weather forecasts that optimize energy dispatch, grid balancing, and preventive turbine maintenance decisions.

Market Restraints

- High Infrastructure and Data Acquisition Costs: Building and maintaining proprietary weather observation networks, including ground stations, Doppler radar systems, weather balloons, and satellite data subscriptions, represents substantial capital investment.

- Data Privacy and Cross-Border Regulatory Complexity: Weather data collected via IoT sensor networks and mobile devices may capture location-sensitive information subject to GDPR, India’s PDPB, and China’s PIPL data regulations.

- Limited Forecast Accuracy in Remote and Data-Sparse Regions: Forecast accuracy degrades significantly in regions with sparse surface observation networks, including the open ocean, polar regions, and large parts of Africa and South Asia.

Market Opportunities

- Parametric Insurance and Climate Risk Analytics: The growing use of parametric weather insurance products, which pay out automatically based on measured weather thresholds rather than assessed losses, is driving demand for accurate, verifiable weather data from certified commercial providers.

- Government Early Warning System Modernization: The UN’s Early Warnings for All initiative aims to provide universal access to multi-hazard early warning systems by 2027, creating a substantial addressable market for commercial weather forecasting operators to supply technology, data, and managed services to national meteorological agencies.

Market Challenges

- Model Skill Verification and Accountability Standards: The proliferation of AI-based weather forecasting models has outpaced the development of standardized skill verification frameworks and liability frameworks. Enterprises relying on commercial weather forecasts for operational decisions require transparent accuracy benchmarks, audit trails, and contractual accountability for forecast failures.

- Talent Shortage in Meteorological Data Science: The intersection of atmospheric science, deep learning, and high-performance computing represents a rare skillset. Competition for qualified meteorological data scientists is intensifying, with technology companies offering compensation packages that traditional meteorological agencies and smaller forecasting firms cannot match, creating workforce bottlenecks for the industry.

Emerging Market Trends

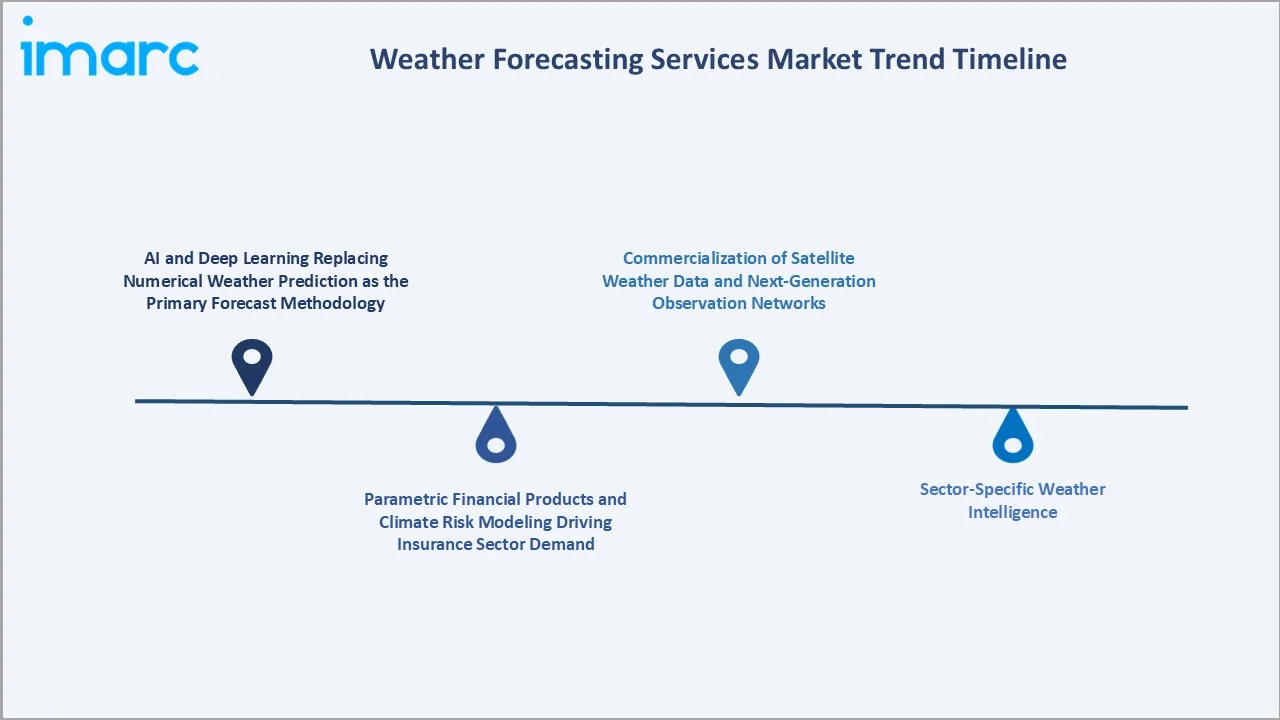

1. AI and Deep Learning Replacing Numerical Weather Prediction as the Primary Forecast Methodology

DeepMind introduced GraphCast, an AI‑based weather model trained on decades of historical data that can produce highly accurate global 10‑day forecasts in under a minute. It marked a decisive inflection point for AI forecast credibility. In February 2025, the European Centre for Medium‑Range Weather Forecasts (ECMWF) made its Artificial Intelligence Forecasting System (AIFS) operational, running AI‑based weather predictions with up to 20% better tracking of tropical cyclones.

2. Commercialization of Satellite Weather Data and Next-Generation Observation Networks

Spire Global’s Radio occultation is a satellite remote sensing technique that measures changes in GPS signal paths through Earth’s atmosphere. These high‑precision observations, used in over 200 million daily global measurements, are critical for improving both weather forecasts and climate models by enhancing atmospheric data in numerical prediction systems.

3. Sector-Specific Weather Intelligence

Precision agriculture weather platforms now integrate soil moisture sensors, evapotranspiration models, crop growth stage databases, and disease pressure forecasts to guide irrigation, pesticide application, and harvest timing decisions at field level. The global precision agriculture market is projected to reach USD 22.5 billion by 2034, with weather intelligence APIs representing a core enabling technology layer for every major precision farming platform.

4. Parametric Financial Products and Climate Risk Modeling Driving Insurance Sector Demand

Parametric weather insurance products, which use measured meteorological thresholds (e.g., rainfall below 50mm during a critical crop growth period) to trigger automatic payouts, require certified, high-accuracy weather data from approved commercial providers at specific geographic coordinates. DTN’s ClimateEdge platform provides long-range climate risk scenario modeling for real estate developers, infrastructure investors, and insurance underwriters seeking 30-year asset-level climate exposure assessments.

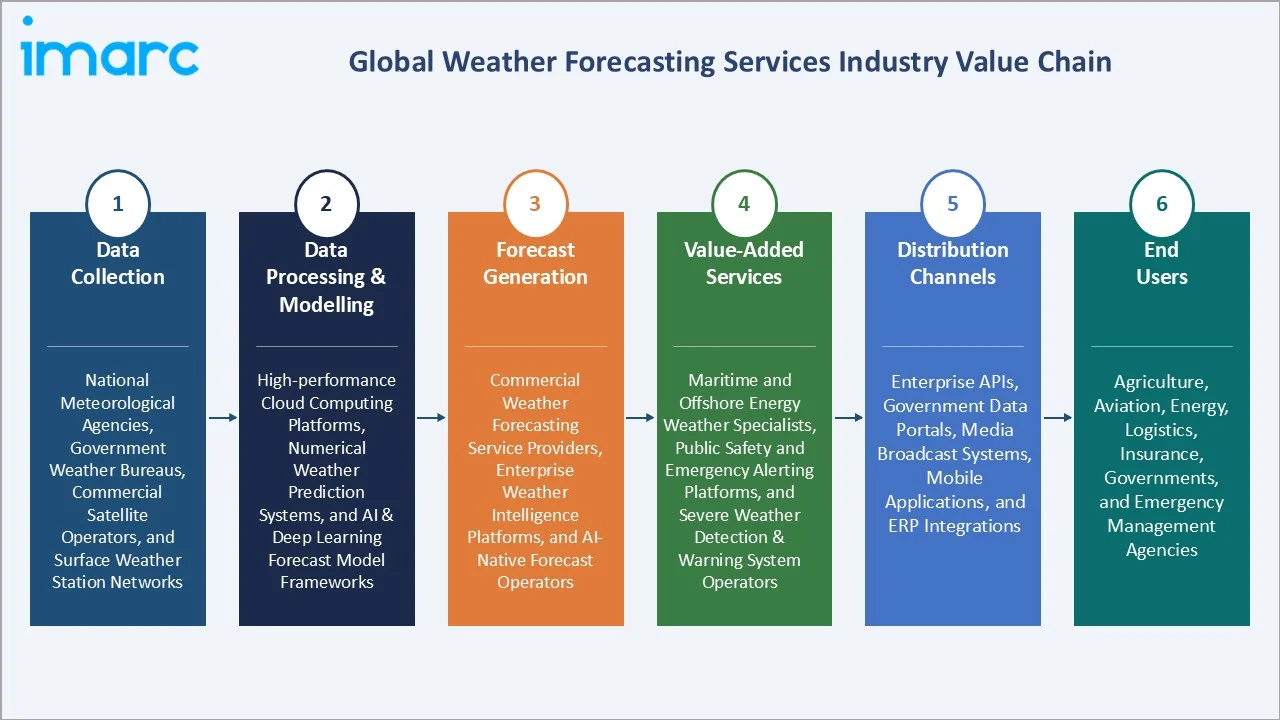

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Data Collection |

National meteorological agencies, government weather bureaus, commercial satellite operators, and surface weather station networks |

|

Data Processing & Modelling |

High-performance cloud computing platforms, numerical weather prediction systems, and AI & deep learning forecast model frameworks |

|

Forecast Generation |

Commercial weather forecasting service providers, enterprise weather intelligence platforms, and AI-native forecast operators |

|

Value-Added Services |

Maritime and offshore energy weather specialists, public safety and emergency alerting platforms, and severe weather detection & warning system operators |

|

Distribution Channels |

Enterprise APIs, government data portals, media broadcast systems, mobile applications, and ERP integrations |

|

End Users |

Agriculture, aviation, energy, logistics, insurance, governments, and emergency management agencies |

Technology Landscape in the Weather Forecasting Services Industry

AI-Powered Global Forecast Models

Transformer-based neural network architectures trained on multi-decade atmospheric reanalysis datasets are enabling commercial operators to generate global 10-day forecasts in seconds on GPU hardware, dramatically reducing compute costs compared to NWP. Google DeepMind’s GraphCast and Huawei’s Pangu-Weather model both demonstrated landmark accuracy improvements in 2024 peer-reviewed evaluations, accelerating the transition to AI-first operational meteorology across commercial and government forecasting platforms.

Commercial Satellite Radio-Occultation Networks

GPS radio-occultation technology aboard small commercial satellites measures atmospheric temperature and humidity profiles by analyzing the bending of GPS signals as they pass through the atmosphere. With over 100,000 daily profiles now available from commercial operators, this data stream is filling critical observational gaps in the Southern Ocean, Arctic, and data-sparse continental regions that historically constrained medium-range forecast accuracy in those areas.

Edge Computing and Real-Time Nowcasting

The everWeather 2.0 AIoT-based weather forecasting station integrates renewable energy for power autonomy, adaptive statistical models for forecasting, and a display for user engagement. In real-world tests, it achieved high short-term forecasting accuracy, with model errors ranging from 2% for 30-minute forecasts to 4% for 120-minute forecasts, proving its effectiveness in continuous weather monitoring.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Forecasting Type |

Medium-range Forecasting |

39.6% |

2025 |

|

Purpose |

🔒 |

🔒 |

2025 |

|

Organization SIze |

Large Enterprises |

71.2% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

North America |

28.9% |

2025 |

By Forecasting Type

Medium-range forecasting leads the weather forecasting services market with a 39.6% share in 2025. Its dominance reflects the practical utility of 3–10 day forecast horizons that enable critical advance operational decisions across multiple high-value industries. Medium-range forecast accuracy has improved dramatically with AI model adoption, with leading commercial platforms now achieving skill scores previously attainable only by ECMWF’s operational NWP system.

To access detailed market analysis, Request Sample

Short-range forecasting holds 35.8% of the market (2025), serving nowcasting and 0–48 hour prediction needs for aviation, road transport safety, and emergency management applications. Long-range forecasting represents 24.6%, used primarily by agricultural commodity traders, infrastructure planners, and insurance underwriters requiring seasonal and annual climate outlooks for strategic financial and operational risk management.

By Organization Size

Large enterprises dominate the organization size segment with a 71.2% share in 2025. Their leadership reflects both the scale of weather-related operational risk they face and their capacity to invest in enterprise-grade weather intelligence platforms. Major airlines, energy utilities, global logistics companies, commodity trading houses, and insurance conglomerates are the primary large enterprise buyers of weather forecasting services.

Small and medium-sized enterprises hold a 28.8% share in 2025. The SME segment is growing faster than the large enterprise segment, driven by the democratization of weather intelligence through affordable API subscription models, self-service forecast platforms, and the proliferation of weather-integrated SaaS products targeting SME agriculture, construction, and outdoor recreation operators.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

28.9% |

NOAA open data policy, renewable energy growth, enterprise API demand |

|

Asia-Pacific |

27.4% |

Agriculture sector expansion, aviation growth, government infrastructure investment |

|

Europe |

25.6% |

Renewable energy sector, climate adaptation policy |

|

Latin America |

10.5% |

Agriculture (soy, coffee), infrastructure projects, disaster preparedness |

|

Middle East & Africa |

7.6% |

Oil & gas operations, desalination, aviation hub expansion |

North America’s market leadership (28.9%, 2025) is a function of both supply and demand advantages. NOAA’s open data policy makes high-resolution radar, satellite, and surface observation data freely available to commercial developers, enabling a vibrant ecosystem of commercially differentiated forecast products built on government observation infrastructure.

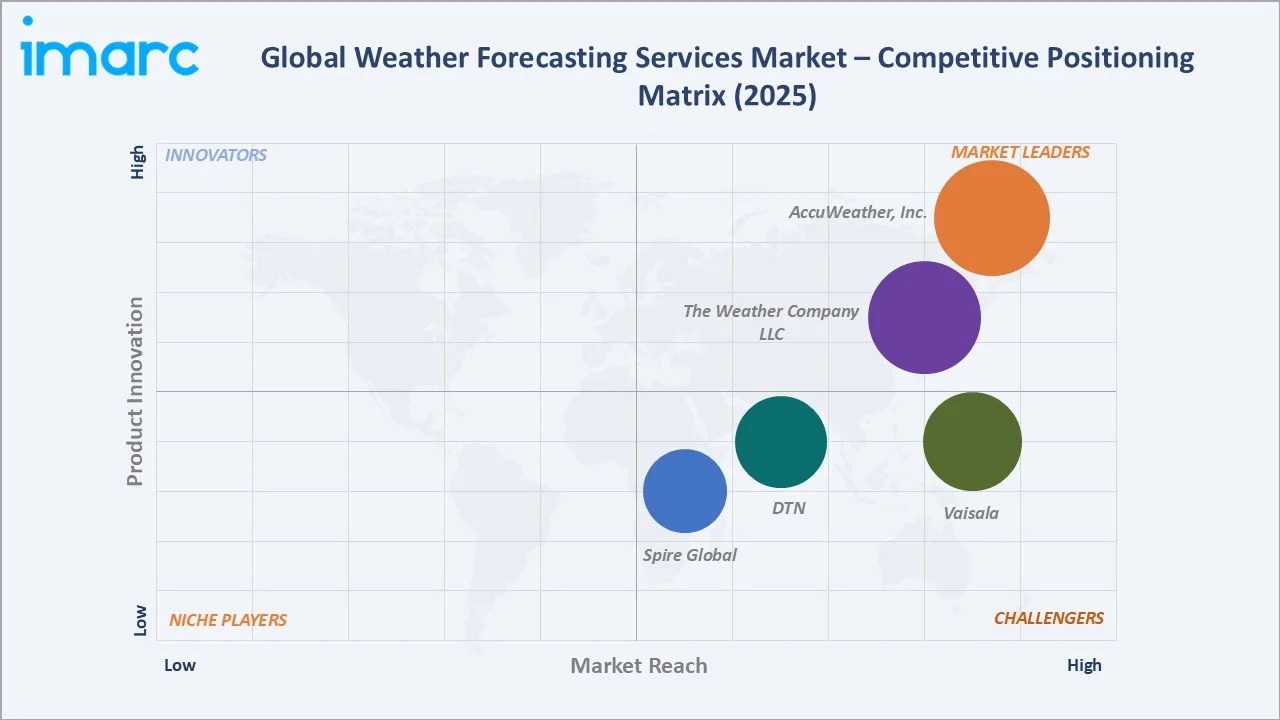

Competitive Landscape

The global weather forecasting services market exhibits a moderately concentrated structure at the premium enterprise tier, with the leading operators, AccuWeather, Inc., The Weather Company LLC, Vaisala, DTN, and Spire Global, collectively holding approximately 42–48% of global market revenue in 2025.

|

Company |

Services/ Brand/Platform/ |

Market Position |

Core Strength |

|

AccuWeather, Inc. |

AccuWeather Enterprise APIs, AccuWeather Connect |

Market Leader |

World's largest commercial weather media company; enterprise API leader; Superior Accuracy™ AI forecast system |

|

The Weather Company LLC |

Enterprise Weather Forecasting Services, GRAF |

Market Leader |

25B+ daily forecasts; B2B enterprise API platform across numerous countries |

|

Vaisala |

AviMet, WindCube, Xweather |

Strong Challenger |

Environmental measurement leader; global surface station network; AI-integrated Xweather enterprise data platform |

|

DTN |

DTN Weather Hub |

Strong Challenger |

Agriculture, energy, and logistics precision weather leader |

|

Spire Global |

DeepInsights, DeepVision

|

Challenger |

120+ satellite constellation; USD 13.69M NOAA commercial data contracts |

A diverse layer of specialized operators serving specific vertical markets, geographies, and technology niches accounts for the remaining revenue. Competitive differentiation is driven by proprietary observation network coverage, AI model accuracy benchmarks, sector-specific product depth, and enterprise integration capabilities.

Key Company Profiles

AccuWeather, Inc.

AccuWeather, Inc., headquartered in State College, Pennsylvania, is the world’s largest commercial weather media company, serving 1.5 billion users worldwide through consumer apps, enterprise APIs, and media broadcast services. Its MinuteCast technology delivers minute-by-minute precipitation forecasts at individual address resolution.

- Product Portfolio: AccuWeather Enterprise APIs and AccuWeather Connect.

- Recent Developments: In January 2024, AccuWeather and Ambient Weather announced a partnership to advance hyperlocal weather reporting by integrating AccuWeather’s forecast data into Ambient Weather’s station network, giving users enhanced precision and real‑time local insights.

- Strategic Focus: Enterprise API revenue growth; global emerging market user acquisition; AI accuracy leadership; sector-specific vertical products for aviation, agriculture, and energy.

The Weather Company LLC

The Weather Company LLC, headquartered in Atlanta, Georgia, operates Weather.com, the Weather Channel apps, and enterprise weather intelligence APIs delivering over 25 billion forecasts daily to consumer and enterprise clients across numerous countries.

- Product Portfolio: Enterprise Weather Forecasting Services, and GRAF.

- Recent Developments: In April 2026, MITRE and The Weather Company LLC announced a strategic collaboration to advance global weather intelligence by integrating MITRE’s high‑resolution Weather 1K AI training dataset into The Weather Company’s forecasting systems.

- Strategic Focus: B2B enterprise API expansion; AI nowcasting leadership through GRAF platform; integration with cloud-native enterprise SaaS ecosystems.

Vaisala

Vaisala, headquartered in Vantaa, Finland, is a global leader in environmental and industrial measurement. Vaisala’s meteorological product portfolio encompasses weather stations, radiosondes, lightning detection networks, and the Xweather commercial weather data platform serving enterprise clients across aviation, energy, transport, and industrial sectors.

- Product Portfolio: AviMet, Windcube, and Xweather.

- Recent Developments: In February 2026, Vaisala launched Vaisala Care, its new Maximal Uptime and Lifetime Weather Measurement Systems service. The offering includes proactive maintenance and lifecycle support to ensure continuous and high‑quality environmental data collection for critical weather and climate applications.

- Strategic Focus: Xweather platform global expansion; AI integration enabling; renewable energy weather services; aviation ground truth data leadership.

Market Concentration Analysis

The weather forecasting services market exhibits moderate concentration, with the top five global operators accounting for approximately 42–48% of total revenue in 2025. Below the tier-one operators, a fragmented ecosystem of 100+ regional specialists, government-affiliated commercial entities, and AI-native startups serves niche verticals and geographies.

Between 2020 and 2025, seven significant transactions reshaped the competitive landscape, as technology platforms, private equity funds, and data companies acquired specialized weather intelligence capabilities to expand into adjacent enterprise software markets.

Investment & Growth Opportunities

Fastest Growing Segments

AI-powered forecasting platforms (estimated CAGR 14.5%), renewable energy weather intelligence services (CAGR 11.2%), and parametric insurance weather data (CAGR 9.8%) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable sub-market of approximately USD 1.8 billion by 2030.

Emerging Market Expansion

South and Southeast Asia, Sub-Saharan Africa, and Latin America collectively represent an incremental USD 420 million weather forecasting services opportunity by 2034, driven by growing agricultural sector digitalization, expanding aviation infrastructure, and government investments in national early warning systems aligned with the UN’s Early Warnings for All initiative.

Venture and Institutional Investment Trends

- Key investment themes include commercial satellite observation networks, AI-native weather model startups, climate risk analytics platforms, and parametric insurance weather data infrastructure.

- Strategic acquirers from energy, agriculture technology, logistics, and insurance sectors are acquiring weather intelligence capabilities as critical operational infrastructure, valuing precision forecast accuracy as a competitive advantage rather than a commodity data service.

Future Market Outlook (2026-2034)

The global weather forecasting services market is positioned for sustained, broad-based growth through 2034. From a base of USD 2.50 Billion in 2025, the market is projected to reach USD 4.70 Billion by 2034, representing total incremental value creation of approximately USD 2.20 Billion over the forecast decade, at a CAGR of 6.90%.

Three structural macro-themes underpin this trajectory: the accelerating transition to renewable energy requiring precision atmospheric modeling; the mounting economic cost of climate change-driven extreme weather creating insatiable demand for early warning intelligence; and the AI revolution in numerical weather prediction enabling commercial operators to deliver superior forecast quality at dramatically reduced cost.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 130 industry participants in 2024–2025, including weather forecasting service operators, enterprise procurement officers, national meteorological agency officials, AI research teams, renewable energy developers, agricultural technology specialists, and insurance underwriting professionals across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, NOAA, ECMWF and WMO technical publications, AI model benchmark studies, regulatory filings, industry trade publications (Weather Business, AMS Bulletin), satellite operator data filings, and publicly available financial data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating global weather-sensitive industry revenue growth rates, commercial meteorological data spending benchmarks by sector, historical market evolution from 2020–2025, and consensus analyst estimates validated against operator-reported revenue growth data.

Weather Forecasting Services Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Forecasting Types Covered | Short-range Forecasting, Medium-range Forecasting, Long-range Forecasting |

| Purposes Covered | Operational Efficiency, Safety, Others |

| Organization Sizes Covered | Large Enterprises, Small and Medium-Sized Enterprises |

| End Users Covered | Transportation, Aviation, Energy and Utilities, Banking, Financial Services and Insurance (BFSI), Agriculture, Media, Manufacturing, Retail, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AccuWeather, Inc., The Weather Company LLC, Vaisala, DTN, Spire Global, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the weather forecasting services market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global weather forecasting services market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the weather forecasting services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Weather Forecasting Services Market Report

The global weather forecasting services market reached USD 2.50 Billion in 2025. It is projected to reach USD 4.70 Billion by 2034.

The weather forecasting services market is expected to grow at a CAGR of 6.90% during the forecast period from 2026 to 2034, supported by AI-driven forecast accuracy improvements and expanding enterprise demand for precision weather intelligence.

North America leads the market with a 28.9% share in 2025, driven by NOAA’s open data ecosystem, advanced commercial meteorological infrastructure, and strong enterprise weather data adoption across energy, agriculture, and logistics sectors.

Medium-range forecasting dominates with a 39.6% share in 2025, valued at approximately USD 990 Million, driven by its optimal 3–10 day forecast horizon that enables advance operational planning across aviation, agriculture, energy, and logistics industries.

Large enterprises hold the dominant position at 71.2% share in 2025, reflecting their substantial operational weather risk exposure and capacity to invest in enterprise-grade weather intelligence platforms and API integrations.

Key players include AccuWeather, Inc., The Weather Company LLC, Vaisala, DTN, and Spire Global.

Key drivers include escalating extreme weather events from climate change, AI and ML integration dramatically improving forecast accuracy, surging renewable energy sector demand for precision atmospheric modeling, and expanding government investment in early warning infrastructure.

High-value opportunities include AI-native forecast model platforms, commercial satellite radio-occultation networks, parametric insurance weather data infrastructure, renewable energy weather intelligence APIs, and government early warning system modernization contracts across developing markets in South Asia, Africa, and Latin America.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)