Dairy Industry in Uttar Pradesh Market Size, Share, Trends and Forecast by Product Type 2026-2034

Dairy Industry in Uttar Pradesh Size, Share, Trends & Forecast (2026-2034)

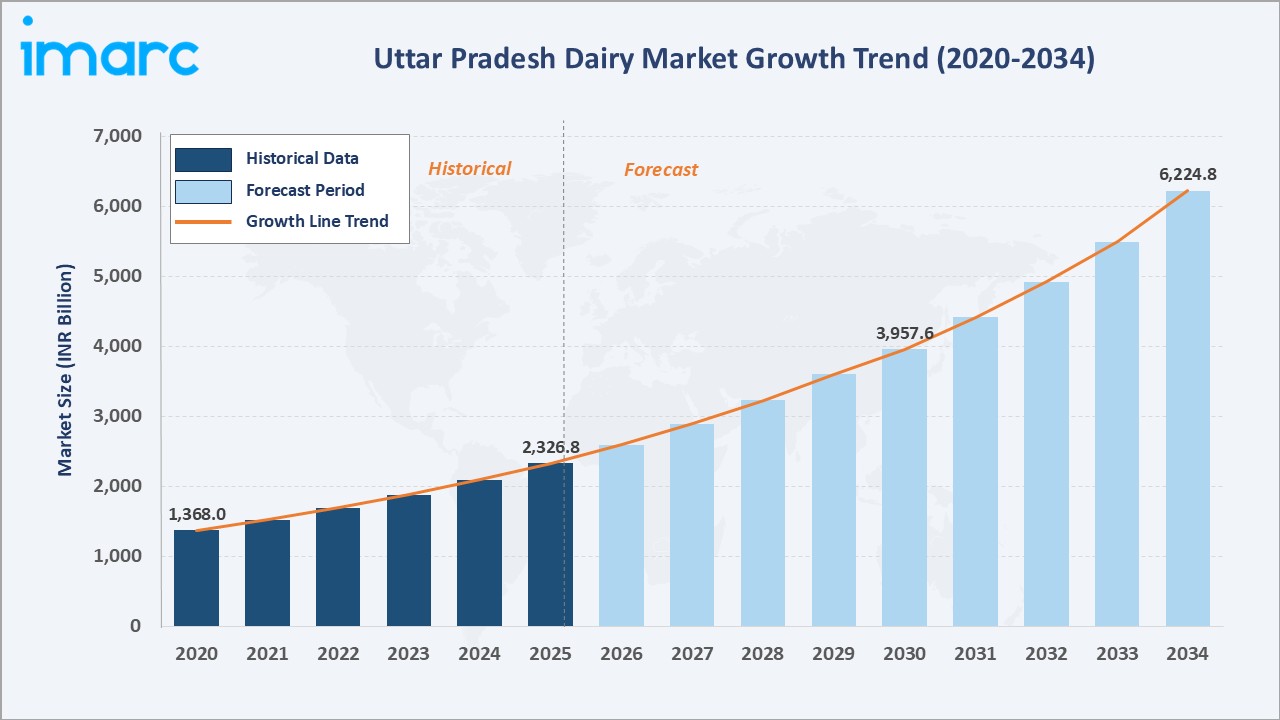

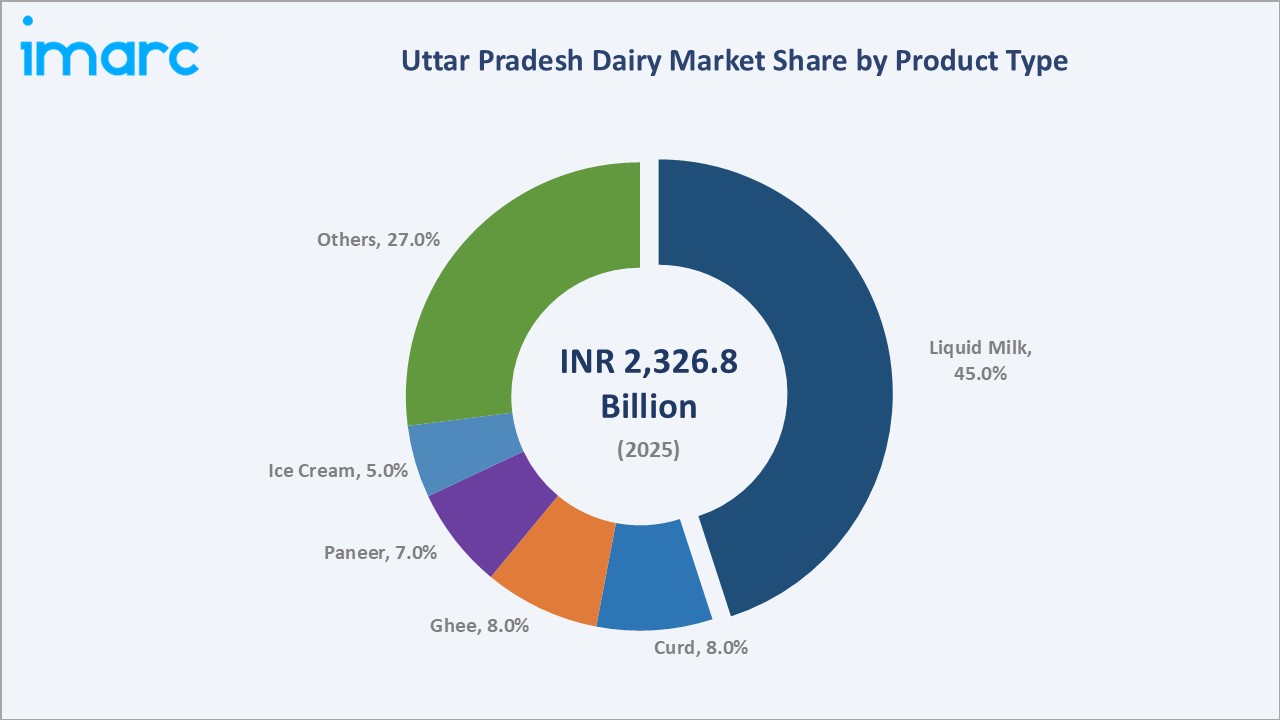

The dairy industry in Uttar Pradesh reached INR 2,326.8 Billion in 2025 and is projected to reach INR 6,224.8 Billion by 2034, growing at a CAGR of 11.21% during 2026-2034. The market is driven by rising demand for value-added dairy products, expanding cooperative networks, rapid urbanisation, and supportive government policy frameworks.

Liquid milk leads product segments with a 45.0% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 2,326.8 Billion |

|

Forecast Market Size (2034) |

INR 6,224.8 Billion |

|

CAGR (2026-2034) |

11.21% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Segment |

Liquid Milk (45.0%, 2025) |

The market expanded from INR 1,368.0 Billion in 2020 to INR 2,326.8 Billion in 2025 – a near 70% increase in five years – anchored at INR 3,957.6 Billion in 2030 and forecast to reach INR 6,224.8 Billion by 2034. The compound trajectory reflects structural shifts including cooperative modernisation, cold chain investment, and deepening penetration of quick-commerce dairy retail in Tier-I and Tier-II cities across Uttar Pradesh.

To get more information on this market, Request Sample

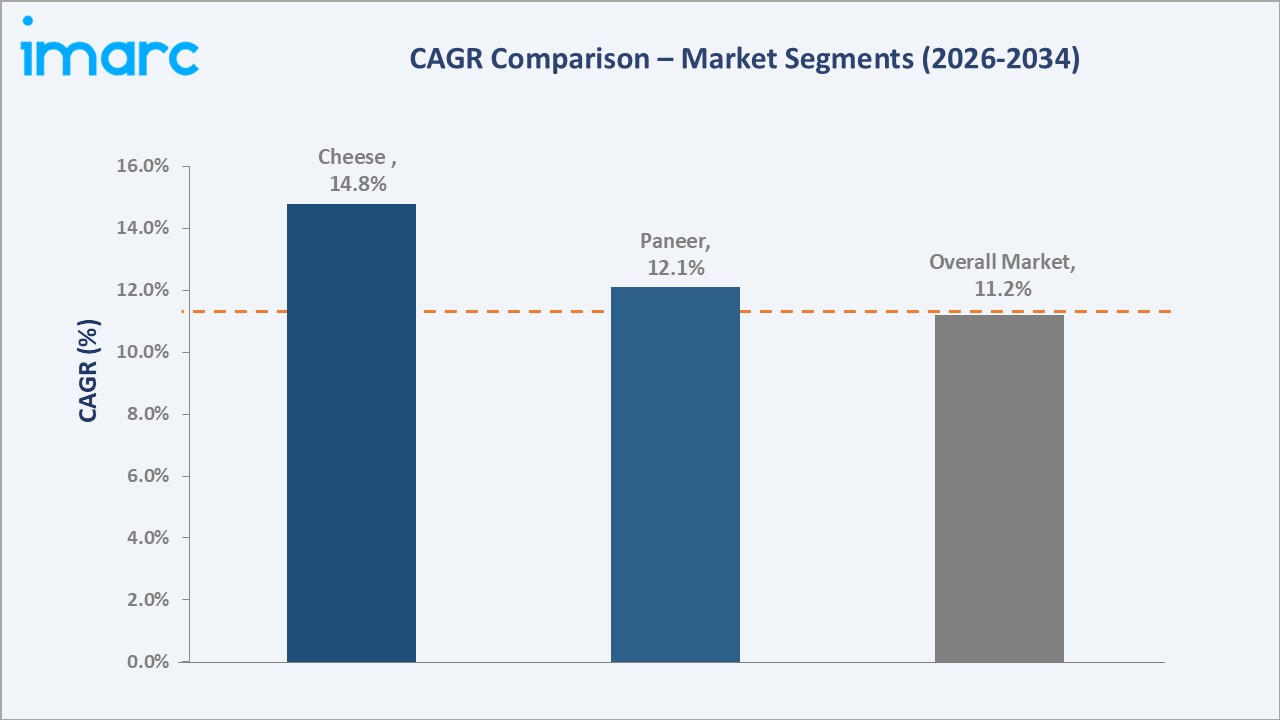

Cheese (~14.8%), UHT milk (~15.1%), and flavoured milk (~14.2%) are the highest-growth segments, growing above the overall market CAGR of 11.21%. Liquid milk grows at ~10.2%, reflecting its maturity as a staple category despite strong volume expansion driven by rising population and packaged format penetration.

Executive Summary

The dairy industry in Uttar Pradesh reached INR 2,326.8 Billion in 2025, representing India’s one of India's largest dairy economies. The market is projected to reach INR 6,224.8 Billion by 2034.

Liquid milk at 45.0% anchors total revenue through its role as the primary daily dairy staple across all consumer segments. Cheese, UHT milk, and flavoured milk represent the fastest-growing categories, driven by urban premiumisation and modern retail expansion.

Key Market Insights

|

Insight |

Data |

|

Dominant Segment |

Liquid Milk – 45.0% share (2025) |

|

Fastest-Growing Segment |

Cheese, UHT Milk, Flavoured Milk (>13% CAGR) |

|

Market Opportunity |

Value-added dairy: cheese, probiotic drinks, yoghurt, UHT milk |

|

Key Growth Driver |

Urbanisation, cooperative modernisation, D2C retail expansion |

Key Analytical Observations:

- Liquid Milk at 45.0%: Liquid milk dominates as the primary staple dairy product consumed across all consumer segments in Uttar Pradesh. High daily consumption frequency, deep cooperative procurement networks, and extensive organised retail distribution reinforce segment dominance.

- Value-Added Segments: Cheese, UHT milk, flavoured milk, and frozen yoghurt are growing above the market CAGR, supported by rising urban incomes, changing dietary preferences, and modern retail expansion in Lucknow, Kanpur, Agra, and Varanasi.

Dairy Industry in Uttar Pradesh – Overview

The dairy industry in Uttar Pradesh encompasses the procurement, processing, and distribution of milk and milk-derived products including liquid milk, curd, ghee, paneer, ice cream, cheese, and other value-added items. The state accounts for the highest share of India’s milk production, supported by a large bovine population and an established cooperative procurement infrastructure.

The ecosystem integrates dairy farmers and rural cooperative societies, state and national cooperative federations, private dairy processors, cold chain operators, organised retail chains, and quick-commerce delivery platforms. Macroeconomic factors include rising per capita incomes, urbanisation, government nutrition programmes, and FSSAI quality regulations.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

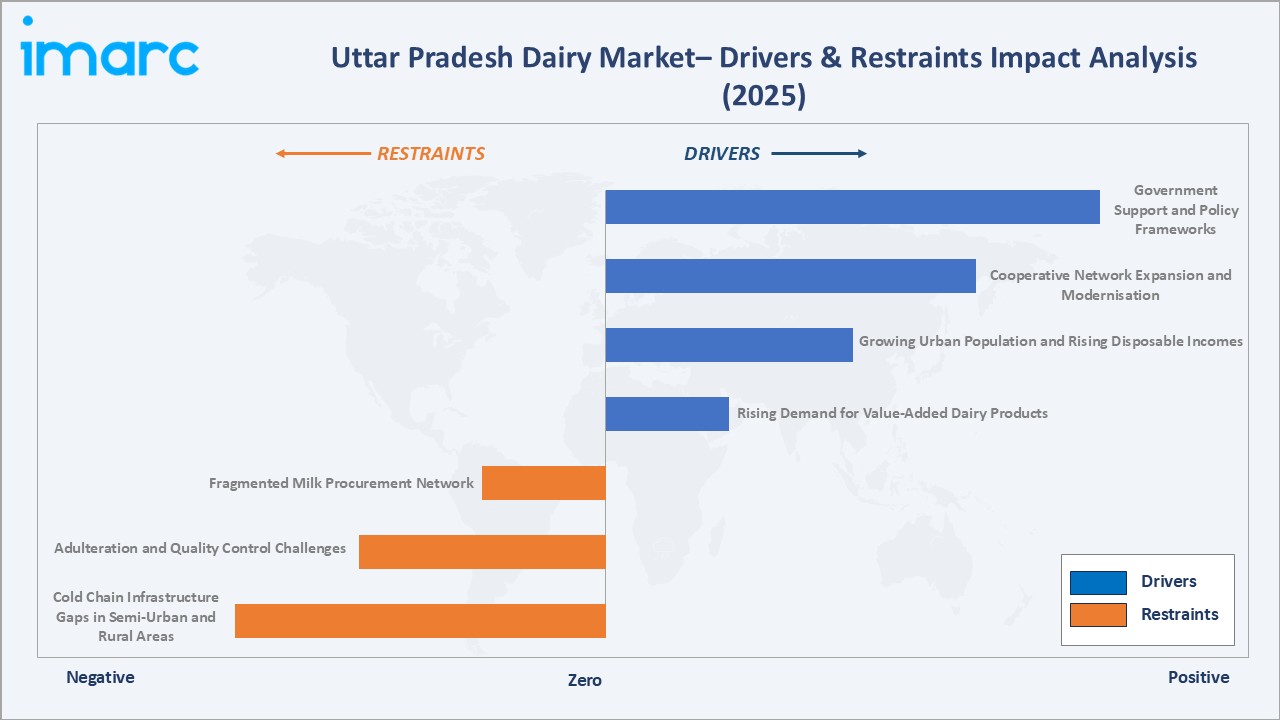

- Rising Demand for Value-Added Dairy Products: Increasing consumer preference for value-added dairy products such as cheese, probiotic curd, UHT milk, and flavoured beverages is structurally expanding the market beyond commodity liquid milk. Health awareness, dietary diversification, and organised retail availability are the primary consumption drivers accelerating category premiumisation across Uttar Pradesh’s urban centres.

- Growing Urban Population and Rising Disposable Incomes: Uttar Pradesh is urbanising rapidly, with Lucknow, Kanpur, Agra, Varanasi, and Noida emerging as high-consumption dairy markets. Rising household incomes are enabling consumers to shift from loose milk to packaged, branded, and value-added dairy products, expanding the organised dairy market and improving per-unit revenue for processors.

- Cooperative Network Expansion and Modernisation: The Pradeshik Cooperative Dairy Federation (PCDF) and National Dairy Development Board (NDDB) are actively expanding village-level bulk milk cooler installations and procurement centres across rural Uttar Pradesh. Cooperative modernisation improves milk quality, reduces procurement losses, and increases formal sector milk supply to processors, supporting volume growth.

- Government Support and Policy Frameworks: Government initiatives, including the National Programme for Dairy Development (NPDD), PM Kisan Sampada Yojana, and NDDB infrastructure grants, are accelerating dairy processing capacity, cold chain development, and farmer income support in Uttar Pradesh.

Market Restraints

- Cold Chain Infrastructure Gaps in Semi-Urban and Rural Areas: Inadequate cold chain infrastructure in semi-urban districts of Uttar Pradesh results in significant post-procurement milk spoilage and limits the geographic reach of perishable value-added products such as paneer, curd, and fresh cream. Cold chain gaps constrain organised market expansion and reduce processor margins, slowing premium segment growth.

- Adulteration and Quality Control Challenges: Milk adulteration remains a persistent structural challenge in Uttar Pradesh’s unorganised dairy segment, eroding consumer trust and creating market fragmentation. Substandard quality milk procurement complicates processing consistency and increases food safety compliance costs for organised players operating under FSSAI standards.

- Fragmented Milk Procurement Network: A large proportion of milk procurement in Uttar Pradesh remains fragmented across informal local traders and small aggregators, limiting scale efficiencies for organised processors. The fragmented procurement structure increases raw material cost variability and reduces processor bargaining power relative to informal sector operators.

Market Opportunities

- Quick-Commerce and D2C Digital Dairy Distribution: Rapid expansion of quick-commerce platforms including Blinkit, Zepto, and Swiggy Instamart in Uttar Pradesh’s Tier-I cities is creating new D2C distribution channels for packaged and premium dairy products. Digital platforms bypass traditional retail intermediaries, improving processor margins and enabling faster consumer reach for premium and value-added categories.

- Export-Oriented Processing Hub Development: Uttar Pradesh’s large milk surplus and existing processing infrastructure create a structural opportunity for developing export-oriented dairy processing facilities targeting ghee, skimmed milk powder, and casein export markets in the Middle East and Southeast Asia. The state’s geographic connectivity supports bulk commodity dairy export logistics.

Market Challenges

- Seasonal Milk Procurement Variability Creating Supply Chain Risk: Pronounced seasonal variation in milk procurement volumes – peak flush season (October–February) and lean season (March–September) – creates production planning complexity for Uttar Pradesh dairy processors. Managing lean-season supply shortfalls while avoiding flush-season inventory surplus requires significant cold storage and powder conversion capacity investment.

- Competitive Pressure from Unorganised Sector on Commodity Pricing: The large and entrenched unorganised dairy sector in Uttar Pradesh, accounting for an estimated 60–65% of total milk sales, exerts sustained downward pricing pressure on commodity liquid milk. Organised players face structural margin compression in commodity categories while competing on price against local operators with significantly lower overhead costs.

Emerging Market Trends

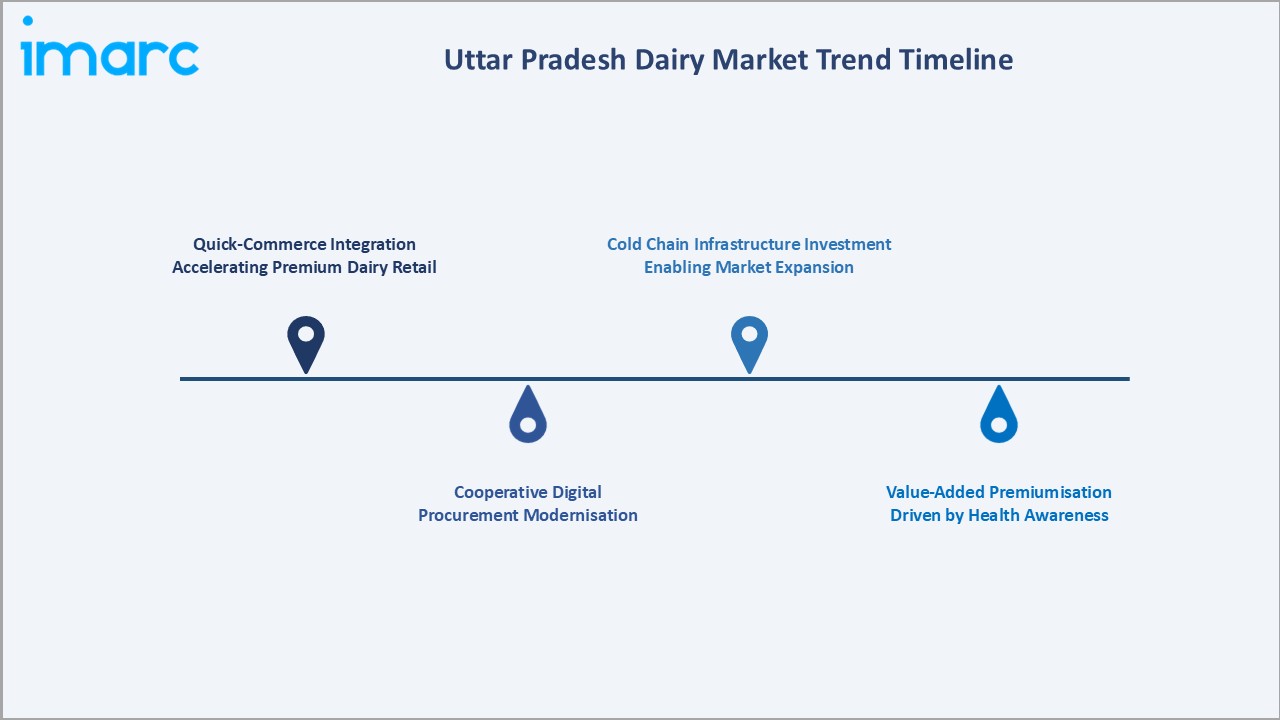

1. Quick-Commerce Integration Accelerating Premium Dairy Retail

Platforms like Blinkit and Zepto are transforming dairy distribution in Uttar Pradesh’s major cities, enabling 10–30-minute delivery of perishable products. This trend is expanding the addressable market for premium and value-added dairy categories and reducing consumer dependence on proximity to traditional retail channels.

2. Cooperative Digital Procurement Modernisation

PCDF is digitising milk procurement through mobile-based payment systems and GPS-enabled bulk milk cooler monitoring. Digital modernisation improves procurement transparency, reduces intermediary costs, and enables direct farmer income support, strengthening cooperative supply chain reliability across Uttar Pradesh.

3. Value-Added Premiumisation Driven by Health Awareness

Growing consumer awareness of protein intake, gut health, and calcium nutrition is accelerating demand for probiotic curd, paneer, flavoured milk, and high-protein dairy beverages in Uttar Pradesh’s urban markets. Premiumisation is expanding per-unit revenue and enabling organised players to differentiate effectively against the informal sector.

4. Cold Chain Infrastructure Investment Enabling Geographic Market Expansion

Government-backed bulk milk cooler installations and private player cold chain investments are progressively enabling organised dairy to reach into Uttar Pradesh’s semi-urban and rural districts. Improving cold chain coverage is expanding the footprint of perishable packaged dairy products and reducing post-procurement losses.

Industry Value Chain Analysis

The Uttar Pradesh dairy value chain integrates raw milk procurement from dairy farmers and cooperative societies, chilling and transportation via bulk milk coolers and insulated tankers, processing and pasteurisation at dairy plants, packaging and branding for organised retail, distribution across modern trade, general trade, and digital channels, and consumer end use across household, institutional, and food service segments.

|

Stage |

Key Activities |

|

Raw Milk Procurement |

Collection of raw milk from dairy farmers and cooperative societies through village-level procurement centres |

|

Chilling & Transportation |

Preservation of milk quality through bulk milk coolers and insulated tanker transport to processing facilities |

|

Processing & Pasteurisation |

Pasteurisation, standardisation, homogenisation, and further processing into value-added dairy products |

|

Packaging & Branding |

Packaging of liquid milk, curd, ghee, paneer, and other products under branded formats for organised retail |

|

Distribution & Retail |

Supply through cooperative channels, modern trade outlets, general trade, and quick-commerce digital platforms |

|

Consumer End Use |

Household consumption, hotel and restaurant procurement, institutional buyers, and food service operators |

Technology Landscape in the Dairy Industry

UHT Processing Technology

Ultra-high temperature (UHT) processing technology enables shelf-stable liquid milk and flavoured milk with 6–12-month ambient shelf life, supporting wider distribution reach across Uttar Pradesh’s semi-urban and rural markets without cold chain dependence. UHT milk is the fastest-growing packaged format in the state’s organised dairy sector.

Probiotic Fermentation Technology

Advanced probiotic fermentation technologies are enabling the development of functional curd and yoghurt products with standardised live bacterial cultures. Probiotic dairy products command significant price premiums over commodity curd and are driving value-added segment growth in Uttar Pradesh’s urban markets, supported by growing health and nutrition awareness.

Cold Chain and IoT Monitoring Technology

Real-time IoT temperature monitoring systems for bulk milk coolers and transportation tankers are improving cold chain integrity in Uttar Pradesh’s procurement network. Digital monitoring reduces milk quality loss, enables early intervention on temperature excursions, and supports FSSAI traceability compliance for organised dairy processors.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Liquid Milk |

45.0% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Liquid milk leads at 45.0% in 2025, anchoring the Uttar Pradesh dairy market through daily household consumption across all income segments. The segment benefits from deep cooperative distribution penetration and government nutrition programme demand. Curd at 8.0% and ghee at 8.0% are the next-largest segments, followed by paneer at 7.0% and ice cream at 5.0%.

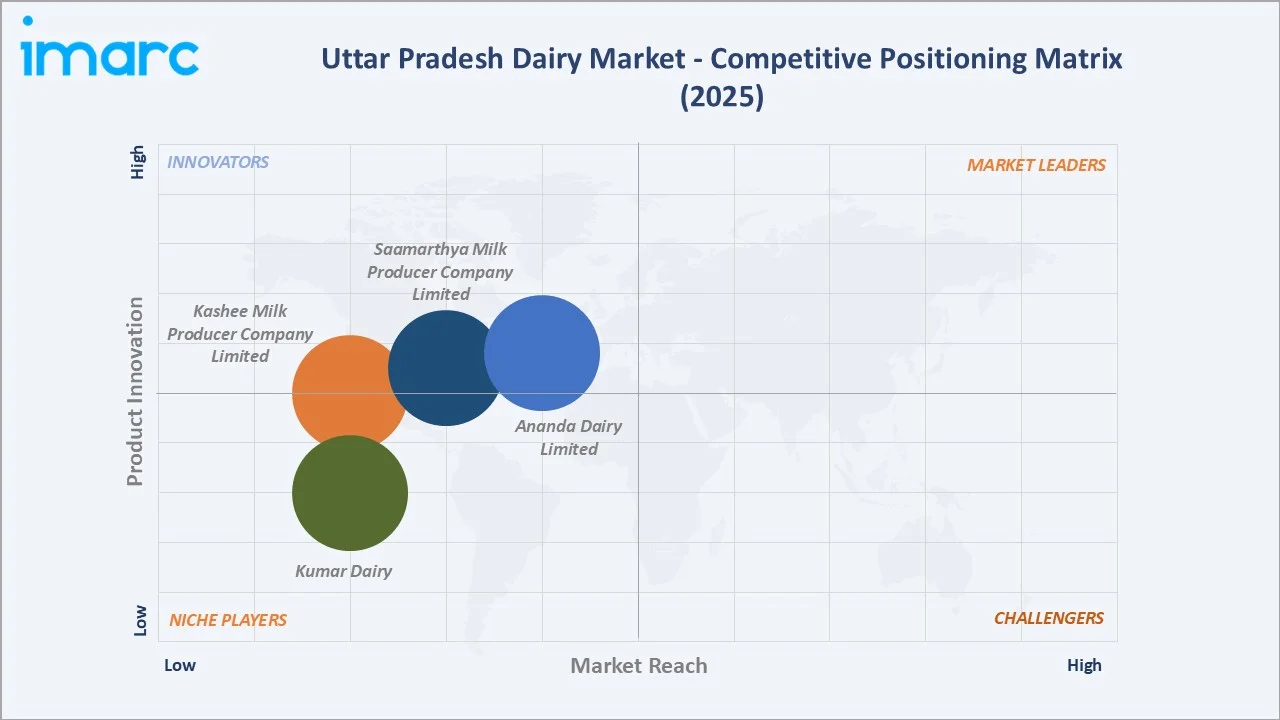

Competitive Landscape

The Uttar Pradesh dairy market competitive landscape is moderately fragmented, with a dominant organised sector led by national cooperative players and strong regional dairy brands, alongside a large unorganised sector of local dairy operators, small processors, and informal milk traders accounting for an estimated 60–65% of total market volume.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Ananda Dairy Limited |

Liquid Milk, Curd, Ghee, Paneer, Lassi |

Regional Leader |

Strong value-added dairy presence across northern India including UP; recognised brand in curd and paneer premium segments. |

|

Kashee Milk Producer Company Limited |

Curd, Buttermilk, Butter, Cheese |

Emerging Player |

A women-owned dairy farmers' cooperative operating across seven districts of eastern Uttar Pradesh |

|

Saamarthya Milk Producer Company Limited |

Milk, Skimmed Milk Powder, Cow Ghee, and Pure Buffalo Ghee |

Emerging Player |

Women-led milk producer company based in Raebareli |

|

Kumar Dairy |

Milk, Chhach, Paneer, Curd, Ghee, Milk Powder |

Niche Player |

Strong branded milk presence across western and central UP |

Key players include Ananda Dairy Limited, Kashee Milk Producer Company Limited, Saamarthya Milk Producer Company Limited, Kumar Dairy, and others.

Key Company Profiles

Ananda Dairy Limited

Ananda Dairy Limited is a leading private dairy company headquartered in Noida, Uttar Pradesh. With multiple processing plants across Uttar Pradesh and an extensive village-level procurement network, Ananda is one of the largest private dairy brands in northern India.

- Key Products: Liquid Milk, Curd, Ghee, Paneer, Lassi

- Strategic Focus: Expanding processing capacity across its UP plants, deepening milk procurement through village-level collection centres, and diversifying into value-added and adjacent food categories to strengthen its presence across high-growth urban markets in northern India.

Kumar Dairy

Kumar Dairy Private Limited is a private dairy manufacturer headquartered in Shikohabad, Firozabad, Uttar Pradesh. It is among the pioneering private dairy companies in the Firozabad district, operating an extensive village-level procurement network and a wide distributor base across western and central Uttar Pradesh.

- Key Products: Milk, Chhach, Paneer, Curd, Ghee, Milk Powder

- Strategic Focus: Strengthening branded milk distribution through booth and retail channel expansion, growing the distributor network to increase geographic coverage across Uttar Pradesh, and leveraging in-house dairy technology expertise to develop its cultured and value-added dairy product range.

Market Concentration Analysis

The organised dairy market in Uttar Pradesh is moderately concentrated, with the top 3-4 players collectively accounting for an estimated 55–65% of organised sector dairy revenue. The unorganised sector, comprising local doodhwallahs, small dairies, and informal processors, accounts for approximately 60–65% of total state dairy by value.

Market concentration in the organised segment is gradually increasing as cooperative modernisation and organised retail expansion progressively displace informal channels in urban markets. Value-added categories, including cheese, UHT milk, and probiotic curd, exhibit significantly higher organised market concentration relative to commodity liquid milk.

Investment & Growth Opportunities

Highest Growth Segments

Cheese (~14.8% CAGR), UHT milk (~15.1% CAGR), flavoured milk (~14.2% CAGR), frozen/flavoured yoghurt (~16%+ CAGR from a small base), and probiotic curd (~11.8% CAGR) represent the highest-growth investment vectors in Uttar Pradesh’s dairy sector through 2034, driven by urban premiumisation and modern retail expansion.

Emerging Investment Opportunities

Cold chain infrastructure investment across semi-urban districts of eastern Uttar Pradesh represents the market’s highest-impact structural investment opportunity, enabling organised dairy market expansion into currently underserved population centres. The INR 2,857.2 Billion incremental market growth between 2025 and 2034 creates significant capacity investment requirements across processing, packaging, and distribution infrastructure.

Investment Themes

- Value-Added Processing Capacity Expansion: Investment in paneer, curd, and cheese processing plants in Lucknow, Varanasi, and Gorakhpur to serve growing organised retail demand and capture premiumisation revenue in a combined INR 558.3 Billion addressable value-added segment.

- Quick-Commerce Cold Chain Integration: Last-mile cold chain infrastructure enabling 10–30-minute perishable dairy delivery in Tier-I and Tier-II cities, capitalising on the rapid growth of quick-commerce platforms creating new distribution access for premium dairy products.

Future Market Outlook (2026-2034)

The dairy industry in Uttar Pradesh is projected to grow from INR 2,326.8 Billion in 2025 to INR 6,224.8 Billion by 2034, delivering a CAGR of 11.21% over the forecast period. The market’s anchor value of INR 3,957.6 Billion in 2030 represents a dairy industry at a critical premiumisation and digital retail inflection point, with organised sector share progressively displacing informal channels.

Three structural forces define market growth with high confidence: urbanisation-driven packaged dairy premiumisation replacing loose milk in Tier-I and Tier-II cities; cooperative procurement modernisation expanding organised milk supply and improving raw material quality; and quick-commerce digital distribution enabling organised dairy penetration into previously underserved consumer segments across Uttar Pradesh.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025), including dairy cooperative federation representatives, private dairy company executives, cold chain logistics operators, quick-commerce category managers, and FSSAI regulatory officials across Uttar Pradesh.

Secondary Research

Secondary research encompassed FSSAI dairy sector compliance reports, National Sample Survey dairy consumption data, Uttar Pradesh government agricultural statistics, and company annual reports. Over 50 secondary sources were reviewed for this analysis.

Forecasting Models

Market revenue forecasts were developed using a bottom-up model: (i) product segment volume projections based on consumption data; (ii) average realisation price by product category and distribution channel; (iii) organised versus unorganised sector share trajectory; (iv) value-added segment premiumisation adjustment factors.

Dairy Industry in Uttar Pradesh Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Liquid Milk, Ghee, Curd, Paneer, Ice-Cream, Table Butter, Skimmed Milk Powder, Frozen/Flavoured Yoghurt, Fresh Cream, Lassi, Butter Milk, Cheese, Flavoured Milk, UHT Milk, Dairy Whitener, Sweet Condensed Milk, Infant Food, Malt Based Beverages |

| Companies Covered | Ananda Dairy Limited, Kashee Milk Producer Company Limited, Saamarthya Milk Producer Company Limited, Kumar Dairy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Dairy Industry in Uttar Pradesh Report

The dairy industry in Uttar Pradesh reached INR 2,326.8 Billion in 2025, driven by liquid milk dominance at 45.0%, strong cooperative procurement infrastructure, and rising organised market penetration across the state.

The market is expected to grow at a CAGR of 11.21% during 2026-2034, reaching INR 6,224.8 Billion by 2034.

Liquid milk leads at 45.0% market share, reflecting its role as the primary daily dairy staple across all consumer segments in Uttar Pradesh.

Key drivers include rising demand for value-added dairy products, growing urban population and disposable incomes, cooperative network expansion and modernisation, and government policy support through NDDB and NPDD programmes.

Major players include Ananda Dairy Limited, Kashee Milk Producer Company Limited, Saamarthya Milk Producer Company Limited, Kumar Dairy, and others.

The fastest-growing segments are cheese, UHT milk, flavoured milk, and frozen/flavoured yoghurt, all growing above the market CAGR of 11.21%, driven by urban premiumisation and modern retail expansion across Uttar Pradesh.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade