India Male Grooming Products Market Size, Share, Trends and Forecast by Product, Price Range, Distribution Channel, and Region, 2026-2034

India Male Grooming Products Market Size, Share, Trends & Forecast (2026-2034)

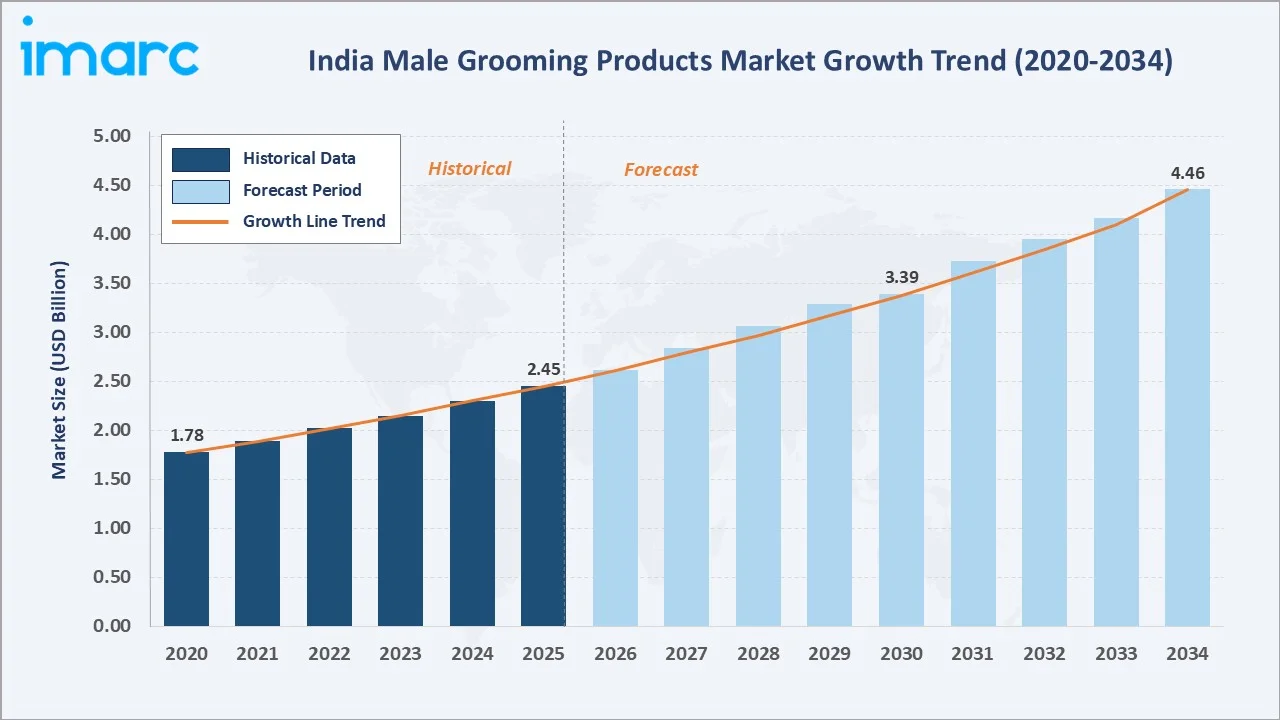

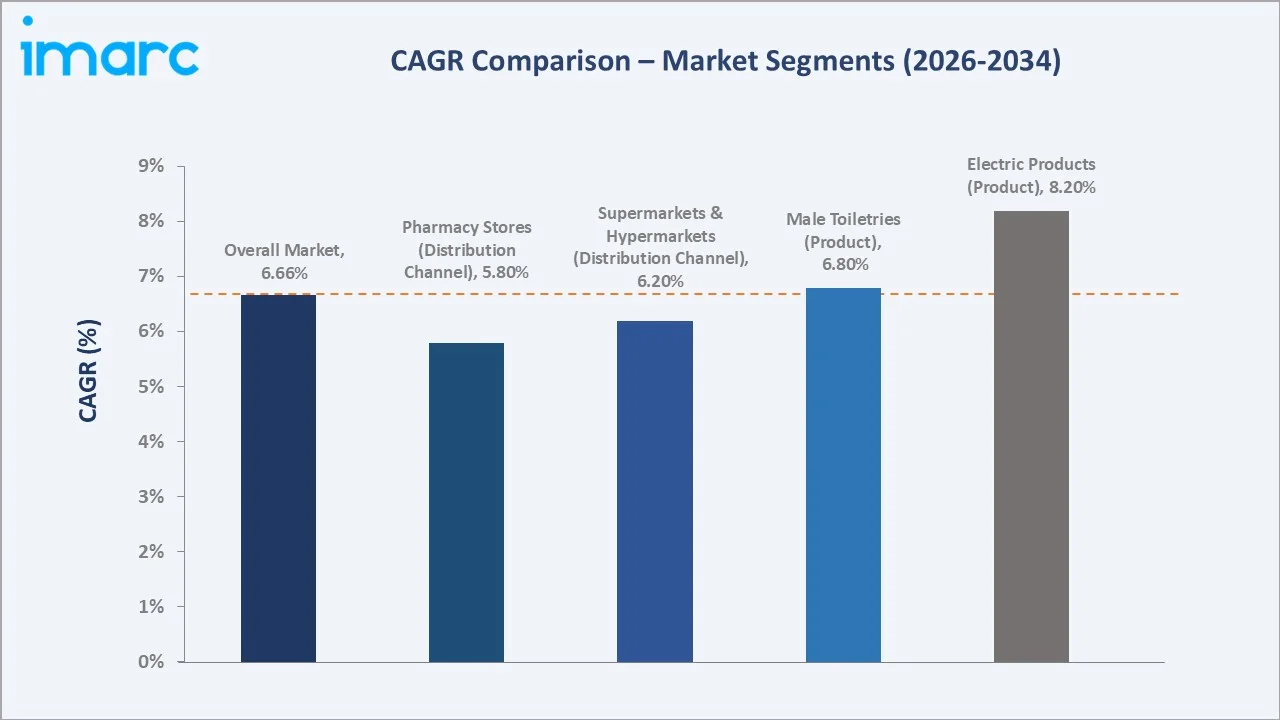

The India male grooming products market size increased from USD 2.45 Billion in 2025 to to USD 2.62 Billion in 2026 and is projected to reach USD 4.46 Billion by 2034, growing at a CAGR of 6.66% during 2026-2034. Rising disposable income and improving living standards, growing consciousness among men about personal wellness and appearance, rapid expansion of unisex and male salons, increasing influence of social media and fitness culture, and the expansion of organized retail channels and e-commerce platforms are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Base year Market Size (2025) |

USD 2.45 Billion |

|

Market Size 2026 |

USD 2.62 Billion |

|

Forecast Market Size (2034) |

USD 4.46 Billion |

|

CAGR (2026-2034) |

6.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

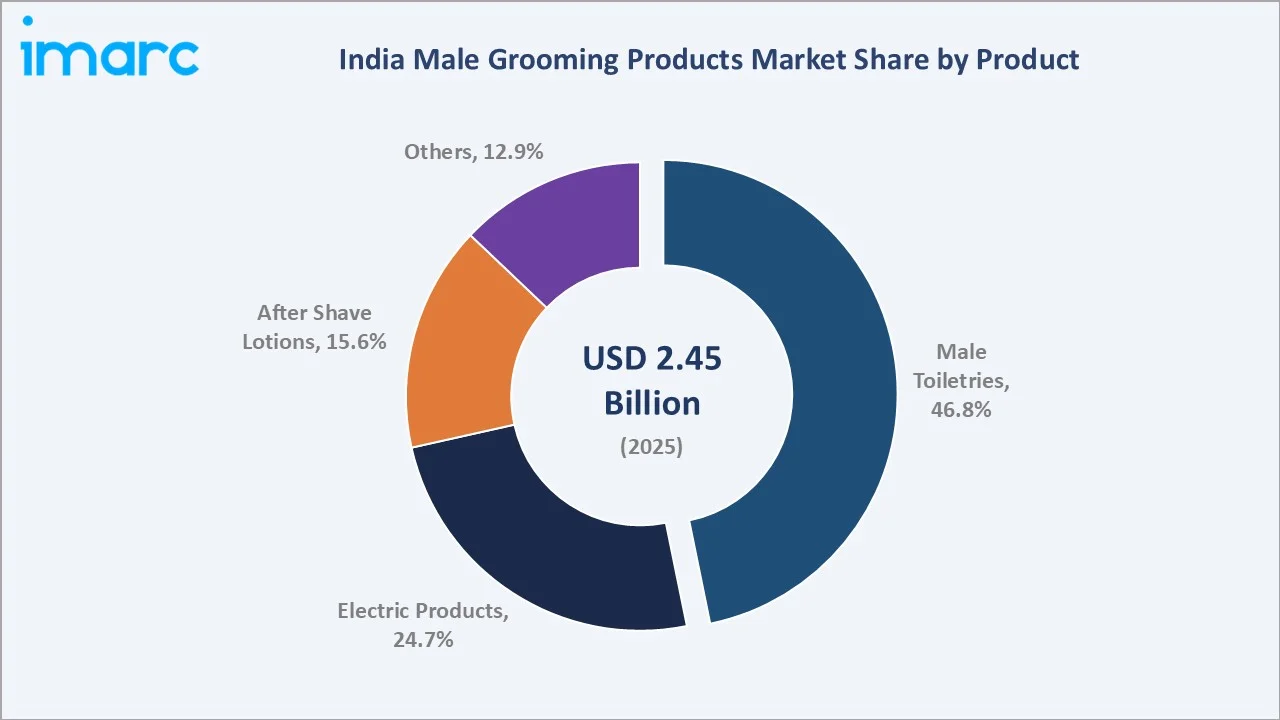

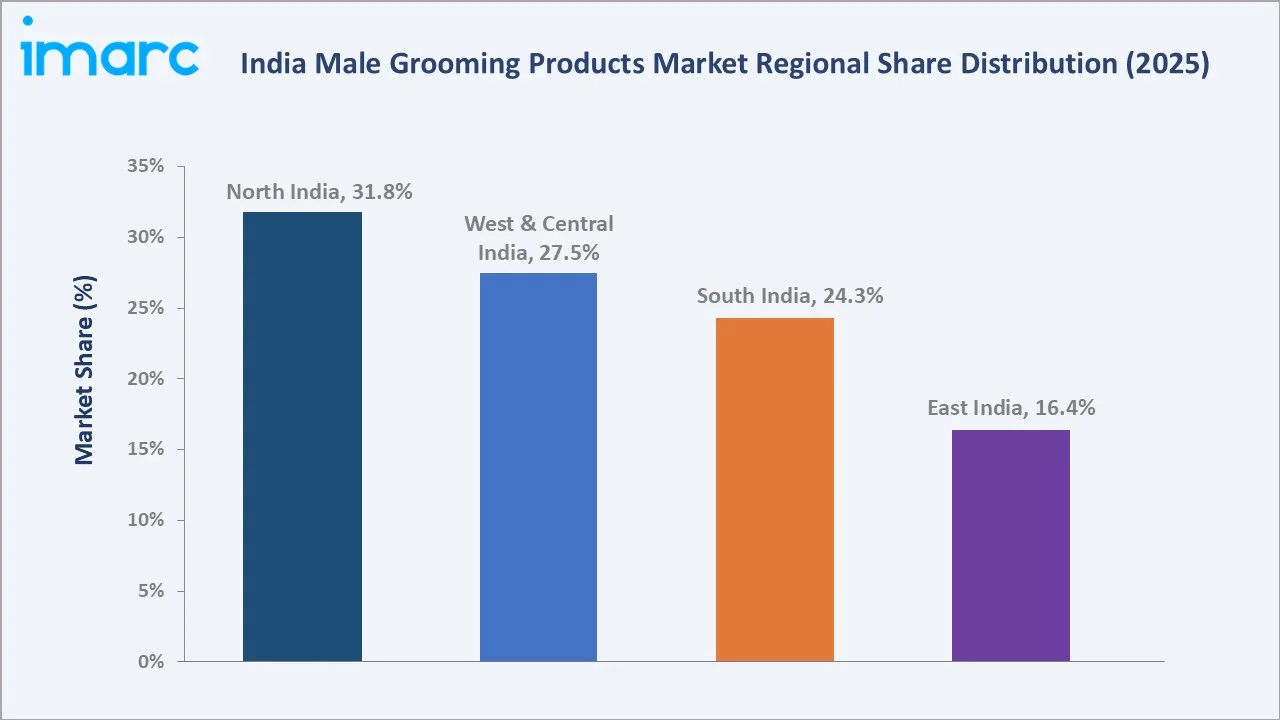

North India leads regionally, holding a 31.8% market share in 2025, underpinned by the region’s high concentration of supermarkets, hypermarkets, and convenience stores across Delhi NCR and Tier-1 cities. Male toiletries command the dominant 46.8% product share, driven by the expansion of hotels and male and unisex salons across India and the broad inclusivity of this category spanning shampoos, deodorants, body washes, and skincare essentials.

To get more information on this market, Request Sample

India’s male grooming products market is underpinned by three structural forces: the metrosexual man trend normalizing skincare routines among Indian males, the explosive growth of direct-to-consumer (D2C) grooming brands enabled by e-commerce, and the rising influence of fitness and wellness culture driving demand for specialized post-workout and lifestyle grooming products. Each force independently sustains multiple product categories, collectively supporting above-GDP-growth CAGR through 2034.

Executive Summary

The India male grooming products market is experiencing robust, broad-based expansion driven by the convergence of rising aspirational consumption, digital retail growth, and shifting male grooming attitudes. The market grew from USD 2.45 Billion in 2025, to USD 2.62 Billion in 2026. It is further projected to attain USD 4.46 Billion by 2034, growing at a CAGR of 6.66%. This trajectory is anchored by India’s young and digitally connected male population, growing interest in personal appearance, and the expansion of organized retail and online channels facilitating product discovery and purchase.

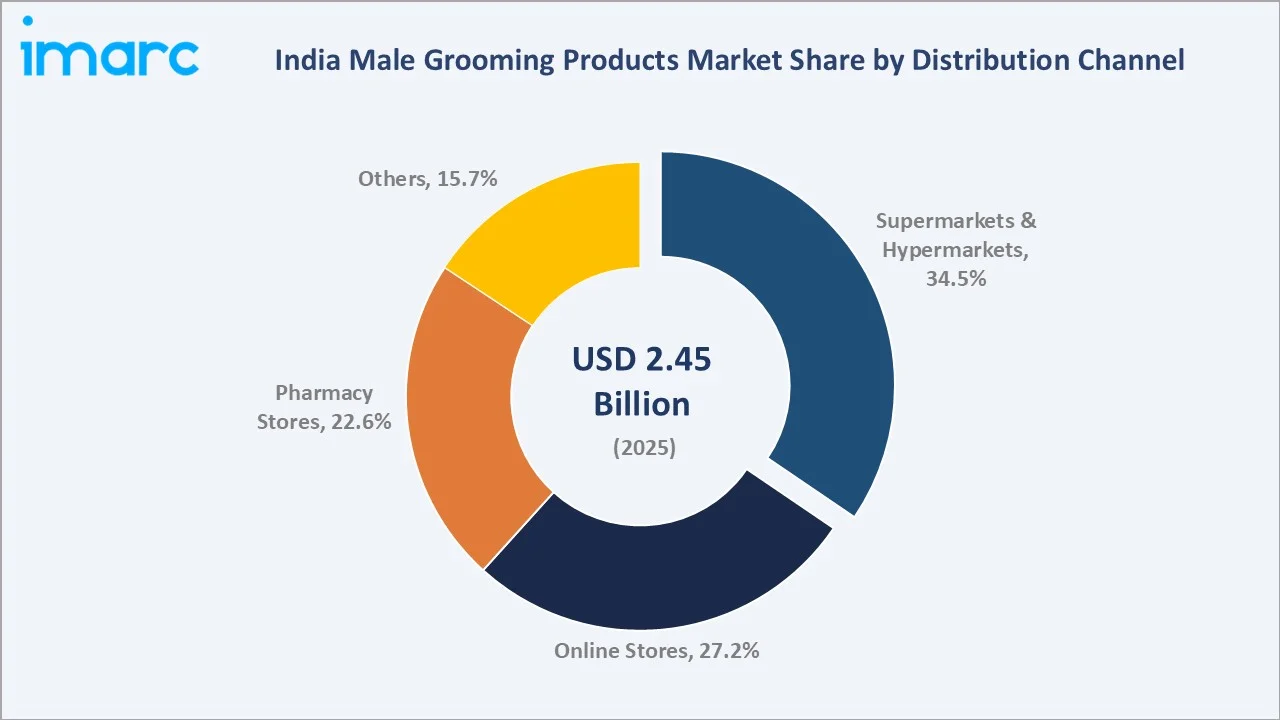

Male toiletries dominate the product segment with a 46.8% share in 2025, while supermarkets and hypermarkets lead distribution at 34.5%, followed closely by online stores at 27.2% and growing. North India leads regionally at 31.8%, driven by dense urban retail infrastructure. Key players include Unilever, L’Oréal S.A., Emami Ltd., Procter & Gamble, and Marico.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Male Toiletries – 46.8% share (2025) |

|

Fastest Growing Product Segment |

Electric Products – ~8.2% CAGR (2026-2034) |

|

Largest Distribution Channel |

Supermarkets & Hypermarkets – 34.5% share (2025) |

|

Fastest Growing Channel |

Online Stores – ~9.5% CAGR (2026-2034) |

|

Leading Region |

North India – 31.8% share (2025) |

|

Top Companies |

Unilever, L’Oréal S.A., Emami Ltd., Procter & Gamble, and Marico |

Key Analytical Observations Supporting the Above Data:

- Male Toiletries’ 46.8% share (2025) reflects the category’s broad inclusivity, encompassing shampoos, conditioners, body washes, deodorants, face washes, moisturizers, and sunscreens. The expansion of hotel hospitality, organized salons (estimated 13,000 organized salons across India in 2025), and rising daily skincare adoption among urban men collectively sustain this segment’s dominant position.

- Electric Products’ fastest-growth trajectory (~8.2% CAGR) is driven by rising adoption of cordless electric shavers, trimmers, and grooming kits among young urban males. The premiumization of electric grooming devices, led by brands such as Philips and Braun, is supported by growing gifting culture and the normalization of beard grooming across age groups and geographies.

- Online Stores’ fastest distribution channel growth (~9.5% CAGR) reflects the D2C e-commerce revolution in Indian grooming. Brands like Beardo, The Man Company, and Bombay Shaving Company, which sell 60–80% of their volume through Amazon, Flipkart, and their own websites, are benefiting from rising digital penetration, easy payment methods, subscription models, and algorithm-driven product discovery.

- North India’s 31.8% share (2025) reflects the region’s highest concentration of organized retail infrastructure, high per-capita urban consumer spending in Delhi NCR and Punjab cities, and strong brand penetration of both mass (Emami, Marico) and premium (L'Oréal, Beiersdorf) grooming portfolios.

India Male Grooming Products Market Overview

Male grooming products encompass a broad range of personal care products designed specifically for male consumers, including toiletries (shampoos, body washes, deodorants, face washes, moisturizers, sunscreens), electric grooming devices (shavers, trimmers, beard stylers), aftershave lotions and balms, and premium lifestyle grooming products (beard oils, serums, anti-ageing creams, hair styling products).

Macroeconomic drivers include India’s per-capita income growing from USD 2,812 to over USD 3,074 between 2026 and 2027, the explosion of digital connectivity with 900+ million smartphone users, and the rising influence of social media platforms Instagram and YouTube. The Bureau of Indian Standards (BIS) Quality Control Order for cosmetics and the Drugs and Cosmetics Act regulate product safety, while increasingly stringent labelling requirements for ingredient disclosure are driving premiumization toward natural and organic formulations.

Market Dynamics

To evaluate market opportunities, Request Sample

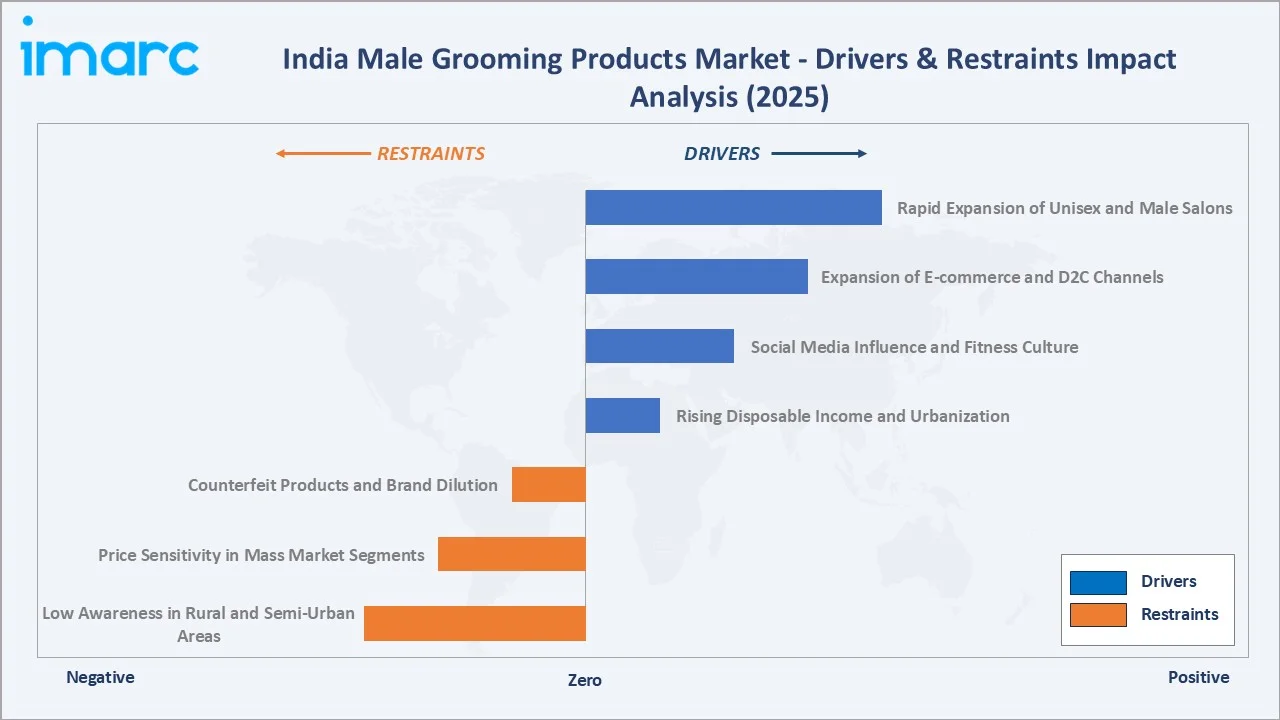

Market Drivers

- Rising Disposable Income and Urbanization: India’s rapidly growing middle class, with household incomes between INR 5–25 Lakh per annum, represents the core demographic for male grooming product premiumization. Urban migration of young men from Tier-2 and Tier-3 cities to metro employment centers introduces them to organized retail channels and branded grooming products.

- Social Media Influence and Fitness Culture: Instagram reels, YouTube grooming tutorials, and the fitness influencer ecosystem have fundamentally normalized male skincare and multi-step grooming routines. Celebrity-led brand associations have direct and measurable impact on product trial and brand recall among Indian male consumers aged 18–35.

- Expansion of E-commerce and D2C Channels: The e-retail market in India has more than doubled over the past five years, while the number of online shoppers has also doubled to reach 290-300 million. D2C platforms enable brands like Beardo, The Man Company, and Bombay Shaving Company to offer subscription kits, personalized product recommendations, and exclusive variants not available in physical retail, creating loyal repeat-purchase communities.

- Rapid Expansion of Unisex and Male Salons: Looks Salon executive stated that male footfall has increased from around 25% to nearly 33-34% of the company’s overall business, providing professional male grooming experiences. Chains like Looks, Jean-Claude Biguine, and Naturals are driving salon standardization and product sell-out from professional grooming environments.

Market Restraints

- Low Awareness in Rural and Semi-Urban Areas: Despite rapid urbanization, approximately 65–70% of India’s population resides in semi-urban and rural areas where grooming product awareness remains limited to basic toiletries. Fragmented distribution, limited media exposure, and low brand investment in rural outreach constrain market penetration.

- Price Sensitivity in Mass Market Segments: India’s mass male grooming category is characterized by intense price competition, with consumers reluctant to pay premiums for features they cannot tangibly evaluate. Global premium brands face margin pressure from domestic mass brands that leverage extensive distribution networks and competitive pricing to capture high-volume, lower-margin consumers.

- Counterfeit Products and Brand Dilution: The Indian grooming market faces significant challenges from counterfeit and duplicate products, particularly in tier-2 and tier-3 markets where brand monitoring is difficult. Fake versions of premium brands, including Gillette, Beardo, and Bombay Shaving Company products, sold through local kirana stores at steep discounts damage brand equity and consumer trust.

Market Opportunities

- Premiumization and Natural/Organic Formulations: Consumer demand for paraben-free, sulphate-free, and natural ingredient grooming products is growing within the Indian male grooming segment. Brands formulating with ayurvedic ingredients, cold-pressed oils, and certified organic actives are commanding 30–60% price premiums versus conventional equivalents, offering superior margin profiles.

- Men’s Skincare Segment Expansion: India’s men’s dedicated skincare segment, encompassing SPF moisturizers, BB creams, eye serums, and anti-ageing formulations, is growing at 18–22% annually, significantly faster than the overall male grooming market. L’Oréal Men Expert and Nivea Men are investing heavily in educating Indian men about structured skincare routines through social media, dermatologist partnerships, and quiz-based recommendation engines.

Market Challenges

- Ingredient Regulatory Complexity: The Bureau of Indian Standards’ Quality Control Order for cosmetics, implemented in 2023, requires BIS certification for a range of beauty and personal care products including face washes, sunscreens, and shampoos. Compliance with BIS certification timelines, testing costs, and renewal requirements adds operational complexity for both Indian and foreign brands, potentially delaying new product launches.

- Consumer Education Gap: Despite the rise of social media grooming content, significant knowledge gaps persist around product ingredient literacy, skin type identification, and appropriate product selection among Indian male consumers. Brands investing in consumer education initiatives face the dual challenge of building category awareness and driving specific brand preference simultaneously, requiring sustained marketing investment across multiple consumer touchpoints.

Emerging Market Trends

1. D2C Brand Proliferation and Subscription Commerce

According to Mintel data, one in five beauty and personal care launches in India between 2017 and 2022 targeted men, the highest share in the Asia-Pacific region. India also surpassed China and Japan in the share of new men’s facial care product launches. In August 2024, Emami acquired full ownership of The Man Company by buying the remaining 49.6% stake in Helios Lifestyle.

2. Men’s Skincare Premiumization

L’Oréal’s Men Expert hydrating gel range, Beiersdorf’s Nivea Men multi-action skincare, and premium natural brands targeting melanin-rich Indian male skin tones are driving average selling price inflation of 8–12% annually within the skincare sub-segment. Brands partnering with dermatologists for ingredient validation and clinical efficacy claims are winning consumer trust in an increasingly skeptical, ingredient-aware consumer cohort.

3. Electric Grooming Device Adoption

Electric shavers and beard trimmers are transitioning from luxury to mainstream among Indian urban men, with Philips launching its most advanced premium shaver, highlighting that demand in the premium segment has outpaced supply, with growth exceeding 75%. The gifting occasion market, including Diwali, birthdays, and the wedding season, drives disproportionate volumes for electric grooming kits priced between INR 2,000–10,000.

4. Ayurvedic and Natural Male Grooming

The Dude entered India’s men’s grooming market with an Ayurveda-inspired portfolio designed for Indian skin, hair textures, climate, and daily grooming routines. Its range includes beard oil, beard wash, beard softener, wax, face wash, scrub, and men’s cream. The brand aims to differentiate itself through chemical-free, nature-led formulations that combine traditional Indian ingredients with modern men’s grooming needs.

Industry Value Chain Analysis

The India male grooming products value chain spans active ingredient sourcing through end-consumer purchase across multiple physical and digital retail touchpoints.

|

Stage |

Description |

|

Raw Material Sourcing |

Active ingredients, fragrance compounds, surfactants, emollients, and packaging materials sourced from domestic and international suppliers |

|

Formulation & Manufacturing |

R&D laboratories developing male-specific formulations; mass production at FMCG manufacturing facilities; BIS certification and quality control testing |

|

Branding & Marketing |

Celebrity and influencer endorsements; digital and television advertising; social media grooming tutorials; salon professional channel education |

|

Distribution & Logistics |

National distribution network covering millions of retail outlets; D2C warehousing and last-mile fulfilment; e-commerce marketplace seller operations |

|

Retail Channels |

Supermarkets and hypermarkets; pharmacy and chemist stores; online stores and D2C; salons, specialty stores, and others |

|

End Consumers |

Urban professionals aged 22–45; gym-goers and fitness enthusiasts; grooming-conscious millennials and Gen Z; semi-urban aspirational male consumers |

Technology Landscape in the India Male Grooming Products Industry

AI-Powered Personalized Grooming Recommendations

Leading D2C male grooming brands are deploying artificial intelligence and machine learning-powered recommendation engines that analyze consumer skin type questionnaires, purchase history, and regional climate data to recommend personalized grooming regimens. Bombay Shaving Company’s digital quiz and subscription personalization platform, and L’Oréal India’s virtual try-on and skin diagnosis tools, exemplify the technology-led consumer engagement strategies enabling higher average order values and reduced product return rates.

Advanced Formulation Technologies for Male-Specific Skin

Male skin physiology differs from female skin in texture (approximately 20% thicker), sebum production rate (1.5–2x higher), and collagen density. Leading brands are investing in male-specific formulation science, including non-comedogenic, fast-absorbing moisturizer bases, salicylic acid and niacinamide formulations targeting male acne and large pore concerns, and UV-filtering SPF moisturizers designed for India’s high-solar-radiation climate.

Connected and Smart Electric Grooming Devices

Electric grooming device manufacturers are integrating Bluetooth connectivity, AI-guided beard shaping algorithms, and smartphone application ecosystems into premium grooming devices. Philips India’s Connected Grooming range enables consumers to receive step-by-step beard styling guidance via smartphone, while precision trimmer technology with sub-millimeter accuracy settings is driving trade-up from manual razors to electric devices across premium product lines.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Male Toiletries |

46.8% |

2025 |

|

Distribution Channel |

Supermarkets & Hypermarkets |

34.5% |

2025 |

|

Price Range |

🔒 |

🔒 |

2025 |

|

Region |

North India |

31.8% |

2025 |

By Product

Male toiletries dominate the India male grooming products market with a 46.8% share in 2025. This segment encompasses the broadest product range within male grooming: face washes, shampoos and conditioners, body washes, deodorants, moisturizers, sunscreens, and daily skincare essentials. The segment’s market leadership reflects the fundamental hygiene-to-lifestyle continuum of Indian male consumer behavior.

To access detailed market analysis, Request Sample

Electric products at 24.7% represent the second-largest and fastest-growing product segment, encompassing electric shavers, beard trimmers, hair clippers, nose and ear trimmers, and multi-grooming kits. After Shave Lotions at 15.6% span from mass-market balms to premium botanical and alcohol-free post-shave formulations.

By Distribution Channel

Supermarkets and hypermarkets hold a 34.5% share in 2025, providing consumers with broad product discovery, competitive pricing, and the physical experience of product evaluation. Major chains including Reliance Smart, D-Mart, and Spencer’s offer dedicated male grooming aisles or sections that consolidate category visibility and enable impulse purchasing across multiple grooming categories simultaneously.

Online stores at 27.2% are the fastest-growing channel, driven by the combination of e-commerce marketplace convenience, D2C brand websites, and social commerce through Instagram and YouTube affiliate links. Pharmacy stores at 22.6% serve as the trusted channel for dermatologist-recommended grooming products including medicated face washes, prescription-strength anti-acne formulations, and SPF-rated skincare.

Regional Market Insights

North India’s market leadership (31.8%, 2025) reflects the region’s dense urban retail infrastructure across Delhi NCR, Chandigarh, Jaipur, Lucknow, and Amritsar, the highest per-capita fashion and personal care spending among Indian regions, and the strong cultural emphasis on personal appearance and social grooming standards among North Indian male consumers.

South India at 24.3% is experiencing above-average growth, driven by Bengaluru and Hyderabad’s large young male technology professional population that is digitally engaged, brand-aware, and willing to invest in premium grooming routines.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

31.8% |

Highest organized retail density, high per-capita consumer spending, strong brand penetration of both mass and premium grooming portfolios |

|

West & Central India |

27.5% |

Premium grooming consumer base, significant pharmacy channel, growing D2C e-commerce adoption, and Maharashtra’s strong male salon culture |

|

South India |

24.3% |

Tech-educated young male consumer base driving premium skincare and D2C adoption, strong pharmacy channel, and high personal care spending per capita |

|

East India |

16.4% |

Established premium grooming market, growing online channel adoption, and expanding organized retail driving incremental penetration. |

Competitive Landscape

India’s male grooming market exhibits moderate-to-high concentration at the mass market level, with Unilever, Procter & Gamble, Emami, L’Oréal collectively commanding approximately 55–60% of revenue. A rapidly growing long-tail of D2C brands, including Bombay Shaving Company, is disrupting traditional brand hierarchies through digital-first marketing and community-led growth.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Unilever |

Dove, Axe, Pears, Clear Men, Dove Men+Care |

Market Leader |

Largest FMCG distributor in India; dominant deodorant and male toiletries presence; skincare premiumization strategy |

|

L’OREAL S.A. |

L’Oréal Men Expert, Garnier Men |

Market Leader |

Global skincare science expertise; Men Expert skincare range; digital skin diagnosis tools; strong pharmacy and e-commerce channel |

|

Emami Ltd. |

Smart & Handsome, The Man Company, HE |

Strong Challenger |

Ayurvedic heritage brand strength in face fairness; full-stack male grooming via The Man Company (D2C acquisition in 2024) |

|

Procter & Gamble |

Gillette, Old Spice, Braun |

Strong Challenger |

Dominant shaving and after-shave portfolio; Braun electric grooming devices; Old Spice deodorant and body wash |

|

Marico |

Beardo |

Challenger |

Pioneer D2C male grooming brand; beard care specialist; strong Instagram community |

Established players benefit from wide retail distribution and brand trust, whereas newer brands focus on personalization, natural ingredients, Ayurveda-inspired formulations, and youth-centric digital campaigns. As male grooming becomes a lifestyle-driven category, companies are increasingly competing on pricing, product efficacy, digital reach, salon partnerships, and premiumization.

Key Company Profiles

Unilever

Unilever, operating through Hindustan Unilever Limited (HUL), is one of the largest fast-moving consumer goods companies and the dominant player in the India male grooming products market. HUL’s male grooming, distributed across India’s 9+ million retail outlets through its unparalleled direct distribution network.

- Product Portfolio: Dove Men+Care (body wash, moisturizer, face wash), Axe (deodorants, body spray, hair styling), Clear Men (anti-dandruff shampoo, scalp care), and Pears (body wash, soap).

- Recent Developments: In May 2025, Hindustan Unilever launched Nexxus in India. The brand uses Trillion Protein Transfusion Technology to repair visible hair damage, offering products such as shampoos, treatment masks, and Oil Resurrection Serum for Indian hair and climate conditions for men haircare.

- Strategic Focus: Axe category leadership in male deodorants through limited editions and celebrity partnerships and Clear Men expansion into scalp health and hair growth segments.

L’OREAL S.A.

L’Oréal S.A. (France) operates L’Oréal India Pvt Ltd, one of the leading premium male grooming and skincare players in India. L’Oréal’s dedicated men’s grooming line L’Oréal Men Expert is distributed through pharmacy stores, premium supermarkets, and direct-to-consumer e-commerce channels.

- Product Portfolio: L’Oréal Men Expert (Pure Charcoal face wash, Hydra Energetic moisturizer, Vita Lift anti-ageing range, UV Defender SPF 50+ sunscreen), Garnier Men (Oil Clear clay face wash, Power White range, Turbo Bright whitening serum).

- Recent Developments: In July 2024, Garnier Men launched its “The Right Fit for Your Face” campaign to promote personalized men’s skincare. The campaign highlights the need to move beyond soap-based face cleansing, addressing concerns such as acne, oiliness, and dullness through face washes, moisturizers, and hair care solutions.

- Strategic Focus: Clinical science-backed skincare positioning for Men Expert; dermatologist partnership ecosystem for consumer trust building; AI-powered skin diagnosis tools on L’Oréal’s website enabling personalized product recommendations.

Emami Ltd.

Emami Ltd. is one of India’s largest FMCG companies with a strong legacy in ayurvedic and natural personal care products. Emami’s male grooming portfolio is uniquely positioned at the intersection of traditional Indian grooming heritage and modern male skincare, with Smart & Handsome serving the mass face care segment and The Man Company targeting the premium D2C male grooming consumer.

- Product Portfolio: Smart & Handsome (Advanced Multi-Benefit face cream, Advanced Brightening face wash), The Man Company (beard oil, face wash, shampoo, serum, grooming kits), and HE.

- Recent Developments: In August 2024, Emami entered a binding agreement to acquire the remaining 49.60% stake in Helios Lifestyle, the parent company of The Man Company, raising its ownership to 100%.

- Strategic Focus: Natural and ayurvedic formulation leadership leveraging Emami’s ingredient heritage; expansion of The Man Company’s offline retail presence in organized grooming retail and salon channels.

Market Concentration Analysis

India’s male grooming market exhibits moderate-to-high concentration at the mass segment level but increasing fragmentation at the premium and D2C segment level. Unilever, L’Oréal S.A. and Marico collectively hold approximately 40–45% of mass male toiletries revenue. The premium skincare and beard care segment is characterized by rapid new entrant activity, with D2C brands competing for the same digitally-engaged urban male consumer cohort through performance marketing and social media brand building.

Consolidation is actively occurring in the D2C segment, with Emami’s acquisition of The Man Company, Marico’s 100% stake acquisition in Beardo, and Wipro Consumer Care’s investments in premium grooming reflecting the strategic imperative of established FMCG players to acquire digitally-native brand equity and D2C consumer relationship management capabilities.

Investment & Growth Opportunities

Fastest Growing Segments

Online-only male grooming subscription kits (~15–18% CAGR), natural and organic male skincare (~12–15% CAGR), electric grooming devices (~8.2% CAGR), and men’s premium anti-ageing skincare (~18–22% CAGR within the category) represent the highest-growth investment vectors through 2034. Together, these sub-categories address a combined incremental addressable market of approximately USD 800 Million–1 Billion within the Indian male grooming ecosystem by 2034.

Emerging Market Expansion

India’s Tier-2 cities (Lucknow, Jaipur, Indore, Coimbatore, Visakhapatnam) and Tier-3 cities are experiencing accelerating growth in male grooming product adoption driven by digital connectivity, rising incomes, and the normalization of personal care as an aspirational consumption category. E-commerce brands reaching these cities through pan-India logistics networks at sub-INR 100 delivery costs are the primary channel for market expansion beyond the Top-10 metro consumer clusters.

Venture and Institutional Investment Trends

- India’s D2C male grooming segment attracted over USD 200 Million in cumulative venture capital funding between 2018 and 2025, with Beardo (Marico-backed), The Man Company (Emami-acquired), and Bombay Shaving Company (Reckitt investment) representing the most prominent exits and strategic consolidation events.

- The rapid expansion of Nykaa Man, Amazon’s dedicated men’s grooming store, and Myntra’s beauty and personal care segments provides a growing institutional retail platform for emerging male grooming brands to access millions of pre-qualified consumers at scale without the prohibitive cost of physical retail shelf space.

- Private label male grooming ranges from Reliance Retail (Tira Beauty) and Tata-backed platforms represent a growing institutional investment theme, with large retail groups developing proprietary grooming brands that leverage captive consumer bases and deep supply chain integration to compete against established FMCG players.

Future Market Outlook (2026-2034)

India’s male grooming products market is positioned for sustained, above-GDP-growth expansion through 2034. From a base of USD 2.45 Billion in 2025, to USD 2.62 Billion in 2026 and the market is projected to reach USD 4.46 Billion by 2034, representing incremental value creation of USD 2.01 Billion at a CAGR of 6.66%. This trajectory is structurally underpinned by India’s young demographic dividend (median age 28 years) and rising aspirational consumption.

The technology transition from product-only selling to personalized grooming ecosystem building, enabled by AI skin diagnostics, subscription models, and connected device ecosystems, will define the competitive landscape by 2034. Brands investing in consumer relationship management technology, data-driven personalization, and sustainability-linked natural formulations will command premium valuations and loyalty metrics that compound into durable competitive advantages in India’s rapidly maturing male grooming market.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 120 industry participants in 2024–2025, including FMCG brand managers, D2C founders, salon chain operators, pharmacy retail buyers, e-commerce category managers, and institutional investors specializing in India’s beauty and personal care sector.

Secondary Research

Secondary research encompassed company annual reports (HUL, Emami, Marico, P&G Hygiene), Ministry of Commerce export-import data for cosmetics (HS Codes 3305, 3307), BIS certified products database, IBEF retail and FMCG reports, and trade publications including Cosmetics & Toiletries, Drug Store News India, and Retail Asia.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating male consumer spend on grooming by income cohort, category penetration by geography, average selling price trajectories by product segment, and distribution channel growth rates. A base-case CAGR of 6.66% reflects consensus estimates validated against company revenue disclosures and consumer panel data from FY 2020 to FY 2025.

India Male Grooming Products Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Repot |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Male Toiletries, Electric Products, After Shave Lotions, Others |

| Price Ranges Covered | Mass Products, Premium Products |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Pharmacy Stores, Online Stores, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | Unilever, L’OREAL S.A., Emami Ltd., Procter & Gamble, Marico, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Male Grooming Products Market Report

The India male grooming products market reached USD 2.45 Billion in 2025 to USD 2.62 Billion in 2026 and is projected to reach USD 4.46 Billion by 2034.

The market is expected to grow at a CAGR of 6.66% during 2026-2034, driven by rising disposable income, social media influence, D2C e-commerce expansion, and growing male skincare awareness.

North India leads with a 31.8% share in 2025, anchored by Delhi NCR’s dense organized retail infrastructure, high per-capita consumer spending, and strong brand penetration across mass and premium male grooming categories.

Male toiletries dominate with a 46.8% share in 2025, encompassing face washes, shampoos, body washes, deodorants, moisturizers, and sunscreens across mass and premium price ranges.

Supermarkets and hypermarkets hold the largest share at 34.5%, offering broad product discovery, competitive pricing, and the physical product evaluation experience that drives purchase decisions for new-to-category male grooming consumers.

Key players include Unilever, L’Oréal S.A., Emami Ltd., Procter & Gamble, and Marico.

Online Stores are growing at approximately 9.5% CAGR because India’s e-commerce revolution in beauty and personal care has made digital the preferred channel for D2C brands to reach consumers, with platform-based discounts, subscription kits, and algorithm-driven product discovery driving high repeat-purchase rates.

Key challenges include low grooming awareness and penetration in rural and semi-urban areas, price sensitivity limiting premiumization in mass segments, counterfeit product proliferation in tier-2 and tier-3 markets, and the complexity of BIS cosmetics certification requirements for new product launches.

Men’s premium skincare, natural and ayurvedic formulations, electric grooming devices, D2C subscription models, and tier-2 city market expansion represent the highest-growth investment opportunities.

The metrosexual trend is the single most important structural driver of the market. It has expanded the average male consumer’s grooming product basket from 2–3 items (shampoo, soap, razors) to 6–8 items (face wash, moisturizer, sunscreen, deodorant, beard care, electric trimmer).

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade