How Big Will be the B2B Payments Market by 2033?

The Global Payment Ecosystem Is Transforming at an Unprecedented Scale:

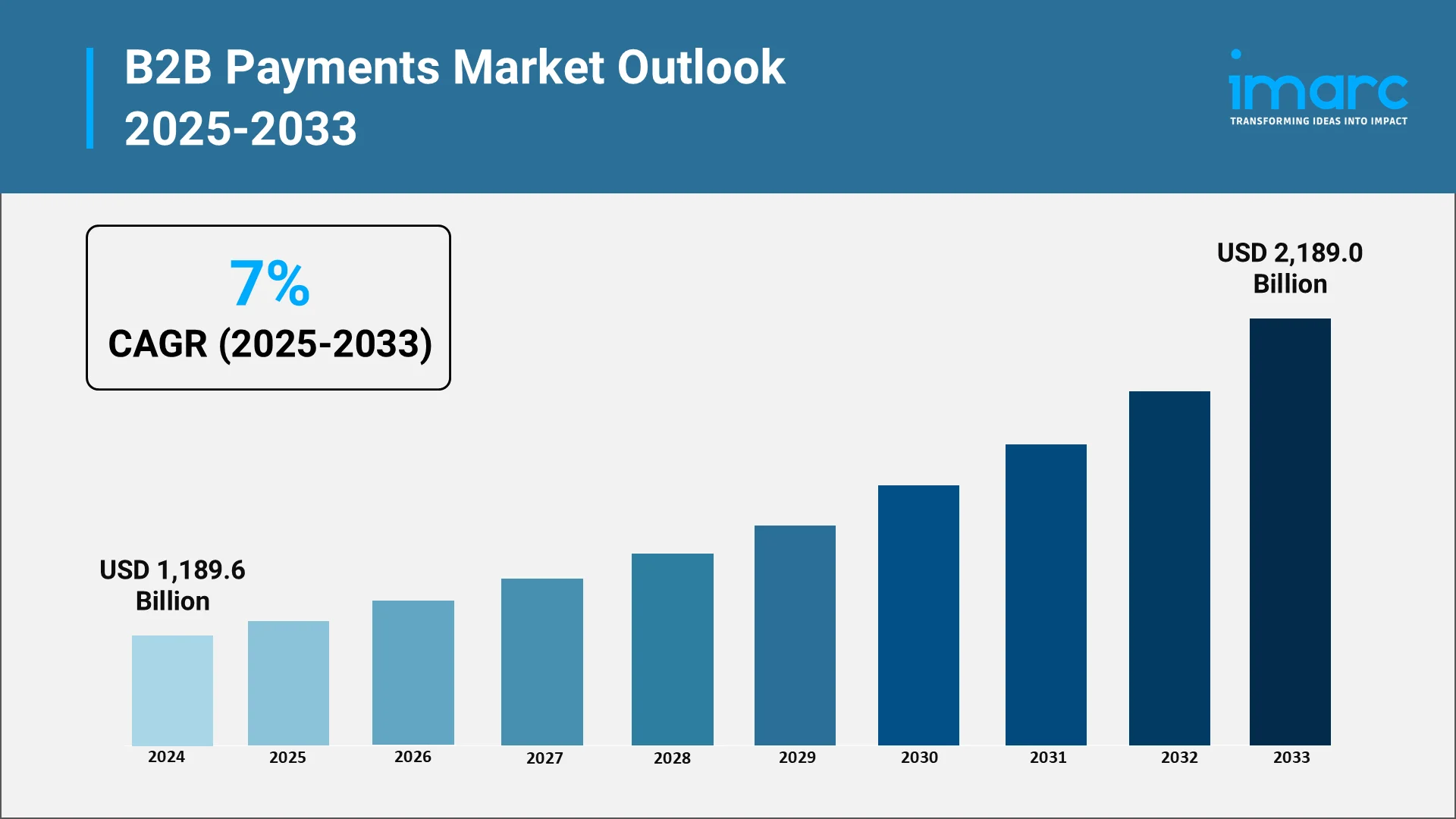

The global business-to-business (B2B) payments landscape is experiencing a fundamental transformation that is reshaping how enterprises conduct financial transactions across borders and industries. The market valued at USD 1,189.6 Billion in 2024 is projecting remarkable growth with expectations to reach USD 2,189.0 Billion by 2033, exhibiting a CAGR of 7% from 2025-2033. This exponential expansion is signaling a paradigm shift in commercial finance, driven by technological innovation, changing business expectations, and the urgent need for more efficient payment infrastructures.

The complexity inherent in B2B transactions is distinguishing this sector from consumer-facing payment systems. Business-to-business payments are promoting safer transactions for merchants requiring recurring, periodic transactions while offering a variety of functions to end users, including accounts receivable, accounts payable, payroll, and acquisition departments.

Explore in-depth findings for this market, Request Sample

Digital Revolution and Cross-Border Commerce Are Powering Market Expansion:

Multiple converging forces are propelling the B2B payments market toward unprecedented growth, with digitalization emerging as the primary catalyst transforming the commercial finance landscape. The increasing digitalization and automation in the B2B payment system is expanding demand among business owners for networking and connecting with various suppliers, distributors, and retailers worldwide, while the market is being driven by the increasing adoption of digital payment solutions, automation, and cloud-based financial systems.

The global expansion of electronic commerce is creating substantial momentum for B2B digital payments innovation. The rise of e-commerce platforms is driving the demand for seamless cross-border payments. As businesses are expanding their supplier networks across international boundaries, the necessity for payment solutions capable of handling multiple currencies, navigating diverse regulatory frameworks, and providing real-time transaction visibility is becoming increasingly critical. For example, NTT Data, OneHotel, and Mastercard together launched a simplified payment processing between online travel agents (OTA) and hotels in Thailand. This solution streamlines and digitizes the hotel payment process, automating the handling of incoming virtual card payments, removing the necessity for manual reconciliation of separate transactions, and enabling seamless processing of payments from OTAs.

The acceleration of automation technologies is revolutionizing accounts payable and accounts receivable processes across industries. Organizations are recognizing that manual payment processes are not only time-consuming but also prone to errors and vulnerable to fraud. The the rise of digital transformation and the widespread use of online payment platforms instead of traditional paper-based methods that require manual printing, mailing, processes, and administrative costs are enhancing the B2B payments market. Advanced automation systems are now enabling approval workflows, instant payment processing, and real-time tracking capabilities that were impossible with legacy systems.

Market Projections Signaling Explosive Growth Across All Segments:

The global B2B payments industry is experiencing robust growth at an impressive pace, fueled by ongoing digital transformation and the growing convergence of finance and technology. Over the next decade, the market is expected to multiply in value as businesses across all sectors migrate from traditional, paper-based transactions to fully digital ecosystems. The adoption of innovative payment solutions, real-time processing, and intelligent automation is significantly increasing transaction speed, transparency, and efficiency.

This transformation is being driven by the widespread use of cloud-based platforms, fintech partnerships, and integrated payment technologies that are simplifying complex financial workflows. Companies are now embedding payment functionalities directly into their enterprise systems, allowing seamless management of invoices, approvals, and settlements. As a result, digital transactions are rapidly becoming the standard for corporate payments worldwide.

By 2033, the global B2B payments landscape is expected to operate almost entirely within a digital framework, characterized by interconnected systems, advanced analytics, and enhanced B2B payment security standards. Businesses that are embracing this evolution today are positioning themselves at the forefront of an increasingly automated and globally unified payment environment.

Regional Dynamics Are Reshaping the Global Payment Architecture:

The geographical distribution of B2B payments growth is revealing fascinating patterns that are reflecting broader economic trends and technological adoption rates across different regions. Asia-Pacific is emerging as the undisputed leader in both current market share and future growth potential.

Asia-Pacific is a major shareholder in the market. This exceptional growth rate is being driven by several converging factors. Numerous enterprises specializing in financial technology across China, Japan, and India are providing advanced payment technologies to businesses, creating a highly competitive and innovative ecosystem. The region's large population, rapidly expanding middle class, and increasing digital literacy are combining to create ideal conditions for payment innovation.

Europe and North America are also dominating the B2B payments transaction market due to high government spending on transaction network security, advanced infrastructure, and standard rules and regulations. The European market is benefiting from increasing adoption of instant payment technology among businesses, improvements in commercial cash management systems, and rising use of digital banking services in the corporate sector.

North America is leveraging its established financial infrastructure and technological leadership to maintain a strong market position. The collaboration between traditional financial institutions and agile fintech companies is creating sophisticated hybrid solutions that are addressing the complex needs of modern enterprises.

.webp)

Blockchain, Real-Time Systems, and AI Are Redefining Payment Capabilities:

The technological landscape underpinning B2B payments is undergoing a revolutionary transformation, with multiple innovations converging to create unprecedented capabilities. Blockchain technology is emerging as one of the most disruptive forces reshaping the payment infrastructure.

B2B cross-border transactions conducted on blockchain technology is rising globally. The distributed ledger technology inherent in blockchain is offering businesses enhanced transparency, reduced transaction costs, and near-instant settlement times. Traditional cross-border payments can take days to settle, while blockchain technology is allowing for near-instant international transfers and transactions operating seamlessly. Moreover, Stablecoins, a type of digital currency represented as tokens on a blockchain, have arisen as a worldwide substitute for traditional payment systems. Stablecoin circulation, primarily issued in US dollars, has increased twofold in the last 18 months but enables only around $30 billion in transactions each day, accounting for under 1 percent of worldwide monetary movements. In 2025, the Bank of North Dakota revealed intentions to introduce the Roughrider coin, marking the state’s inaugural stablecoin.

Real-time payment systems are experiencing explosive growth as businesses demand immediate transaction processing and settlement. The traditional model of multi-day settlement periods is becoming increasingly unacceptable in a business environment that demands immediate access to working capital and real-time visibility into cash positions. In 2024, payabl., a top financial services provider in Europe, has unveiled its Payment Accounts, a cloud-driven, API-first solution aimed at assisting businesses of any size in managing their daily payment requirements on a single, user-friendly platform. payabl. virtual business cards offer enterprises enhanced control, security, and insight into their expenditures.

Artificial intelligence (AI) and machine learning (ML) technologies are revolutionizing fraud detection, payment routing optimization, and process automation. AI-enhanced software helps protect businesses from unauthorized transactions, optimizing cash flow management, minimizing manual errors, and boosting productivity. These intelligent systems are identifying anomalies that might indicate fraudulent activity, analyzing transaction patterns in real-time, and automatically implementing preventive measures.

The rise of virtual cards is providing businesses with enhanced security and control over payment processes. Virtual cards are offering dynamic card numbers for each transaction, spending limits that can be adjusted in real-time, and detailed transaction data that simplifies reconciliation.

Emerging B2B Payments Opportunities Are Creating New Value Propositions:

The evolving B2B payments landscape is unveiling numerous opportunities for businesses willing to embrace innovation and adapt to changing market dynamics. The shift toward digital payments is creating demand for integrated solutions that address multiple pain points simultaneously.

Payment-as-a-Service models are gaining traction as businesses seek to outsource payment complexity to specialized providers. These comprehensive platforms are offering end-to-end solutions encompassing invoice processing, payment execution, reconciliation, and reporting within unified interfaces.

The expansion of embedded finance is opening new channels for payment innovation. Businesses are increasingly expecting payment capabilities to be integrated directly into the software platforms they use for procurement, inventory management, and supplier relationship management. This integration is eliminating friction points and enabling straight-through processing from purchase order to payment execution.

The B2B payments market in emerging economies, particularly in Asia-Pacific regions, is expanding as SMEs are using digital payment systems to improve workflows and enter global markets. Small and medium-sized enterprises (SMEs) that previously lacked access to sophisticated payment infrastructure are now gaining capabilities that were once exclusive to large corporations. This democratization of payment technology is leveling the competitive playing field and enabling smaller businesses to participate in global supply chains.

Security Threats and Legacy Systems Are Challenging Rapid Adoption:

Security threats and legacy infrastructure are slowing down the shift to modern payment systems. The rise in payment fraud is one of the biggest problems companies face. The 2025 AFP Payments Fraud and Control Survey, sponsored by Truist, found that 79% of organizations experienced attempted or actual payments fraud incidents in 2024. Human error adds to the issue, with businesses losing an estimated 1–3% of their budgets annually from mistakes in vendor or supplier payments. Because B2B transactions often involve high values, they are prime targets for cybercriminals.

Complex workflows and multiple approval steps make B2B payments especially vulnerable. Legacy systems, large transaction volumes, and multi-step verification chains create weak points that attackers exploit. Business email compromise scams, where criminals impersonate executives or vendors to trigger fake payments, are now harder to detect.

Legacy systems are another obstacle. Many firms still use hybrid setups where old enterprise software connects with newer payment platforms. These outdated systems often lack modern security features, leaving integration points exposed. Fully replacing legacy systems is costly, so many companies delay modernization despite the risks.

Internal resistance is another barrier. Many finance teams hesitate to leave behind long-standing systems. The learning curve, fear of disruptions, and uncertainty about cost savings slow progress.

Strategic Imperatives for Businesses Navigating Payment Transformation:

Organizations seeking to capitalize on the opportunities presented by evolving B2B payment systems must adopt comprehensive strategies that balance innovation with risk management. The imperative to digitize is clear, but successful implementation requires careful planning and execution.

Building security into payment infrastructure from the outset is essential rather than treating it as an afterthought. The best companies are continuously reevaluating their risks, with compliance built into the architecture of products and services rather than bolted on later. This proactive approach requires organizations to conduct regular risk assessments, implement multi-layered security controls, and foster cultures where employees are empowered to report suspicious activities without fear of repercussion.

Embracing automation while maintaining appropriate human oversight represents a delicate balance. While automated systems are offering substantial efficiency gains and reduced error rates, completely removing human judgment from payment processes can create new risks.

Strategic partnerships between traditional financial institutions and innovative fintech companies are creating synergies that accelerate innovation while leveraging established infrastructure and regulatory expertise. Banks are bringing deep industry knowledge, extensive customer relationships, and regulatory compliance capabilities, while fintechs are contributing technological agility, user experience design expertise, and innovative business models. For example, in 2025, FAB collaborated with Oracle and Mastercard to introduce MENA’s inaugural embedded B2B payment solution, improving efficiency, security, and transparency for enterprises. This partnership merges the capabilities of two industry frontrunners to transform B2B finance and payment procedures for FAB customers, improving efficiency, security, financial clarity, and supplier connections.

The future trajectory of the B2B payments market is pointing toward continued rapid evolution driven by technological innovation, changing business expectations, and the inexorable shift toward digital-first commerce. Organizations that are strategically positioning themselves to capitalize on these trends, by investing in modern payment infrastructure, prioritizing security and compliance, and fostering cultures of continuous innovation, are positioning themselves for competitive advantage in an increasingly digital global economy.

Unlocking Growth: IMARC Group’s Outlook on the Global B2B Payments Market by 2033:

IMARC Group is providing essential analysis on the Global B2B Payments Market, guiding financial institutions, enterprises, and fintech firms toward opportunities emerging through 2033. Our research supports strategic planning in digital transformation, payment innovation, and regulatory compliance through:

- Market Intelligence: Detailed insights into the digitalization of B2B payments, automation trends, and cross-border transaction innovations across industries such as manufacturing, retail, and services.

- Strategic Forecasting: Projections on market growth, transaction volumes, and adoption of advanced technologies including AI, blockchain, and embedded finance that are reshaping efficiency and transparency.

- Competitive Benchmarking: Evaluation of key global and regional players—banks, fintechs, and processors—focusing on product innovation, partnerships, and market positioning.

- Regulatory Analysis: Assessment of AML, KYC, and data protection frameworks affecting B2B payment operations, ensuring alignment with international compliance standards.

- Consulting Solutions: Customized strategies that enhance digital payment infrastructure, strengthen fraud prevention, and optimize working capital.

IMARC Group’s insights help businesses anticipate growth opportunities, mitigate risks, and lead in the rapidly evolving B2B payments landscape by 2033.

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

The smart medical devices market is entering a decade defined by connected care, real-time diagnostics, and patient empowerment. Valued at USD 45.9 Billion in 2024, the market is projected to reach USD 82 Billion by 2033, expanding at a compound annual growth rate (CAGR) of 6.33% between 2025 and 2033 by IMARC Group. This steady rise reflects growing confidence in data-driven healthcare systems, integration of IoT in medical environments, and the increasing role of artificial intelligence in clinical decision-making.

Active Pharmaceutical Ingredients (APIs) are the bioactive molecules of any drug used in pharmaceuticals, which cause the desired therapeutic action in the body of a human being. APIs are the central core of all drugs, chemical or biological and are responsible for the efficacy, strength, and safety of the drug. APIs are synthesized by various complex chemical synthesis, fermentation, biotechnological, or extraction processes based on the type of drug.

A bio medical incinerator is a high-temperature combustion system specialized for biomedical waste disposal by hospitals, clinics, laboratories, and research institutions. Biomedical waste usually consists of infectious waste, pathological waste, sharps, pharmaceuticals, and contaminated disposables that are very hazardous to human health and the environment if not treated.

Obesity, once viewed primarily as a lifestyle choice, is now widely recognized as a complex and chronic disease characterized by excessive body fat accumulation. Its global prevalence is escalating at an alarming rate posing a significant and growing challenge to public health systems worldwide.

Gonorrhea, a sexually transmitted infection caused by the bacterium Neisseria gonorrhoeae, is a major public health issue globally. Reports show that over one million new cases of curable STIs are contracted every day by individuals aged 15 to 49 years, with the majority being asymptomatic.

The 7 major allergic conjunctivitis markets reached a value of USD 2.1 Billion in 2024. Looking forward, IMARC Group expects the 7MM to reach USD 2.9 Billion by 2035, exhibiting a growth rate (CAGR) of 3.00% during 2025-2035.

The healthcare sector is changing rapidly because of the growing demand for better ways to manage chronic diseases. As we move toward 2025 and beyond, digital tools are playing an important role in dealing with conditions like diabetes, heart disease, cancer, and respiratory problems.

The global multivitamin gummies market consists of chewable dietary supplements that are charged with key vitamins and minerals aimed at maintaining general health and wellness. The gummies present a handy, enjoyable, and easy-to-swallow option to classic pills or tablets, hence are predominantly preferred by children and adults who do not like taking pills.

India's pharmaceutical sector is evolving rapidly, supported by the integration of artificial intelligence (AI) across the value chain. As of 2023, India ranked as the third-largest pharmaceutical producer by volume, accounting for 20% of global generic drug exports.

As Lung Cancer Awareness continues to build global momentum in 2025, Artificial Intelligence (AI) is proving to be a transformative force—not only in clinical diagnostics but also in public education and preventive health efforts. Given that lung cancer remains one of the world’s deadliest cancers, accounting for over 1.8 million deaths each year and a five-year survival rate of just 28.4%, the integration of AI marks a critical turning point.

Observed on May 19, Hepatitis Testing Day 2025 emphasizes the need to "Test. Treat. Eliminate," highlighting the gap in diagnosing hepatitis B and C, which cause over 1.3 million deaths annually. Hepatitis remains a major global health threat, on par with HIV, tuberculosis, and malaria. The growing viral hepatitis market <Viral Hepatitis Market Size | Share, Trends - 2034 > reflects rising demand for better diagnostics, treatments, and integrated care. The WHO warns that without faster testing and treatment, the goal of eliminating hepatitis by 2030 may not be achieved, with disparities in diagnostics, particularly in low- and middle-income countries, hindering progress.

Observed on May 8, World Ovarian Cancer Day 2025 carries the theme “No Woman Left Behind,” reinforcing the urgent need to close the gaps in access, diagnosis, treatment, and care across all regions and socioeconomic groups. Ovarian cancer remains one of the deadliest gynecological cancers, often detected too late due to vague symptoms and limited screening tools. The World Ovarian Cancer Coalition projects a 55% rise in annual cases and nearly 70% more deaths by 2050, with the heaviest burden falling on low- and middle-income countries. Equitable access to early diagnostics, genetic testing, and targeted therapies is critical.

In clinics around the world, a concerning pattern is becoming increasingly evident: a growing number of patients are experiencing wheezing, breathlessness, and persistent coughing. This surge reflects a broader global trend. According to the World Health Organization (WHO), more than 260 million people are currently living with asthma, making it one of the most widespread and persistent chronic respiratory conditions globally.

Observed on April 25, World Malaria Day 2025 carries the theme “Accelerating Equity in Malaria Prevention and Cure,” underscoring the urgent need to reach communities still lacking access to life-saving vaccines and diagnostics. While global malaria death rates have seen modest declines, the disease continues to claim the life of one child every minute, highlighting the critical need for swift, equity-driven action

Sulfamethoxazole is a common synthetic antibacterial that is a member of the sulfonamide class of antibiotics. This substance plays a very significant role in modern medicine due to the amazing capabilities offered by the substance for curing infections and bacterial diseases. Trimethoprim and sulfamethoxazole are frequently used together to create the well-known antibiotic co-trimoxazole, which is well-known for its potency against a variety of bacterial infections. It works by preventing the manufacture of folic acid, which is necessary for the growth of bacteria. Sulfamethoxazole is an essential part of modern antibiotic therapy since it has been used to treat lung infections, urinary tract infections, and other common bacterial illnesses.

Healthcare consumables are necessary medical supplies used for patient treatment, diagnostics, and cleanliness in clinics, hospitals, and home care settings. These consist of supplies such as surgical masks, bandages, gloves, syringes, catheters, and disinfectants. Usually, they are disposable or single use to preserve sterility and stop infections. Healthcare consumables are an essential component of the global healthcare ecosystem and are in high demand due to expanding healthcare needs, an increase in operations, infection control measures, and technological improvements.

Catheters are flexible, tubular medical devices designed to access various body cavities, organs, or blood vessels for diagnostic or therapeutic purposes. They can be broadly classified into types based on their application, including urinary catheters, cardiac catheters, and intravenous (IV) catheters. Catheters are commonly used in diverse healthcare settings for managing chronic conditions, enabling fluid drainage, delivering medications, or facilitating minimally invasive surgeries.

Bioinformatics involves applying computational techniques and tools to study and understand biological systems at the molecular level. It is a field of study that combines mathematics, biology, computer science, and statistics to research genomic data and biological networks. The goal is to interpret information from large biological data sets, such as DNA sequences, protein structures, gene expressions, and other high-throughput experimental data. This field provides various products and services, such as knowledge management tools, bioinformatics platforms, and services.

A non-animal model refers to an experimental system or method used in scientific research or testing that does not involve the use of animals. These models are developed to simulate biological processes, test hypotheses, or study diseases without the need for live animals. The aim is often to reduce the reliance on animal testing, which has ethical implications and raises concerns about animal welfare.

Cell therapy involves the transplantation and manipulation of living cells to replace and repair damaged tissue. Its primary branches include stem cell therapy and non-stem cell therapy. Stem cell therapy utilizes stem cells to repair, replace, or rejuvenate damaged or diseased cells and tissues as they possess the ability to differentiate into various specialized cell types, making them valuable for regenerative medicine. Non-stem cell-based therapies typically involve somatic cells isolated from the human body. These cells are propagated, expanded, selected, and then administered to patients for curative, preventive, or diagnostic purposes. On the other hand, gene therapy seeks to treat diseases by introducing, replacing, or inactivating genes within cells.