Molybdenum Market Size, Share, Trends and Forecast by Product Type, Sales Channel, End Use, and Region, 2026-2034

Global Molybdenum Market Size, Share, Trends & Forecast (2026-2034)

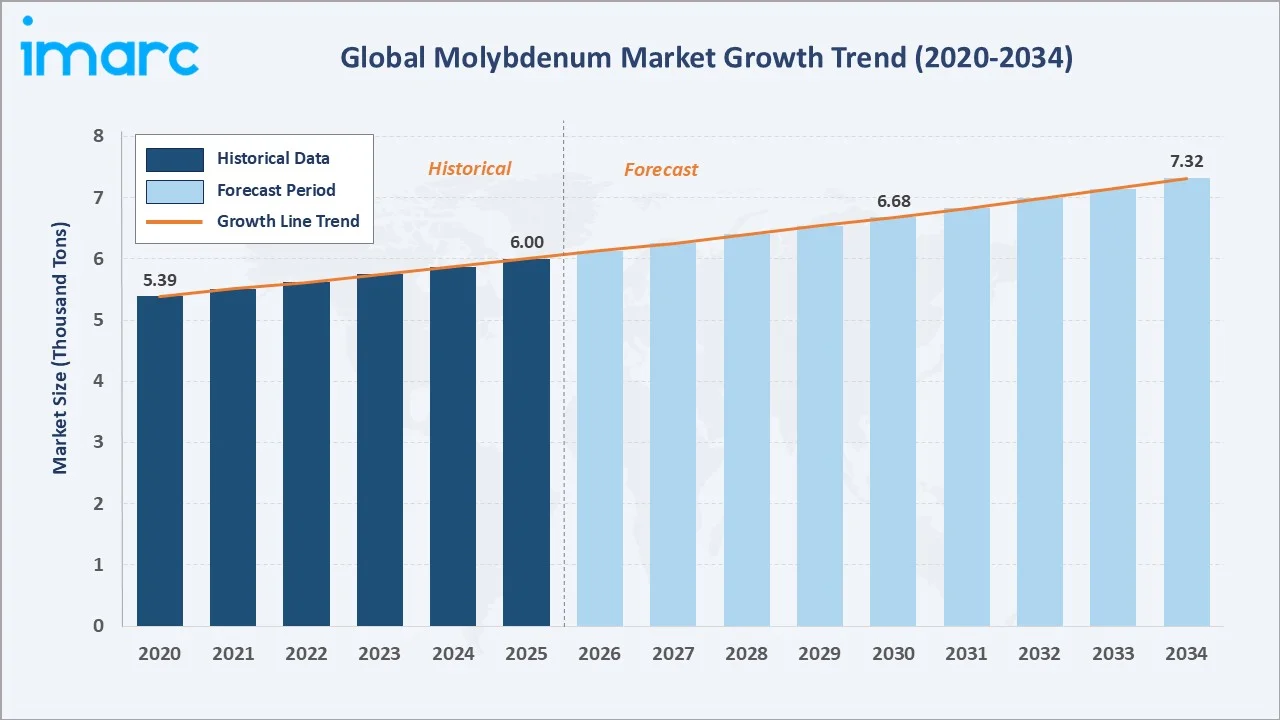

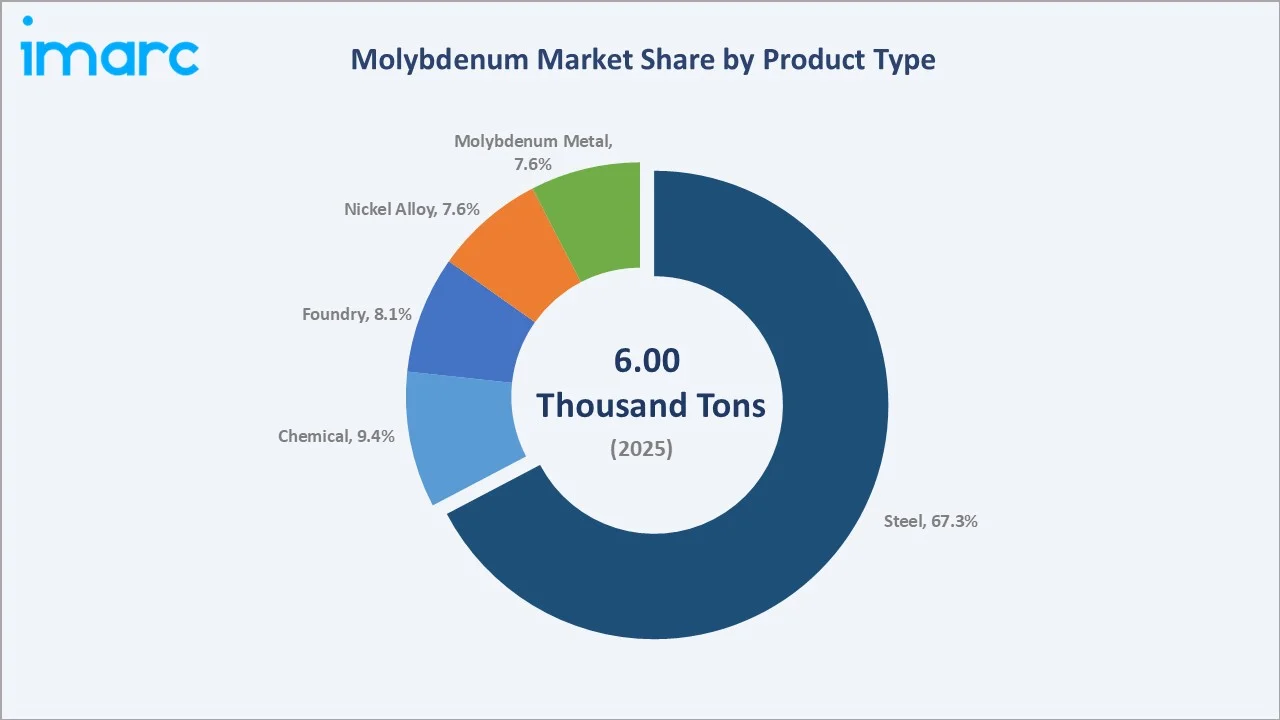

The global molybdenum market size reached 6.00 Thousand Tons in 2025 and is projected to reach 7.32 Thousand Tons by 2034, exhibiting a CAGR of 2.16% during 2026-2034. Strong steel industry demand, rising renewable energy adoption, and expanding infrastructure investments across emerging economies are the primary forces driving market growth.

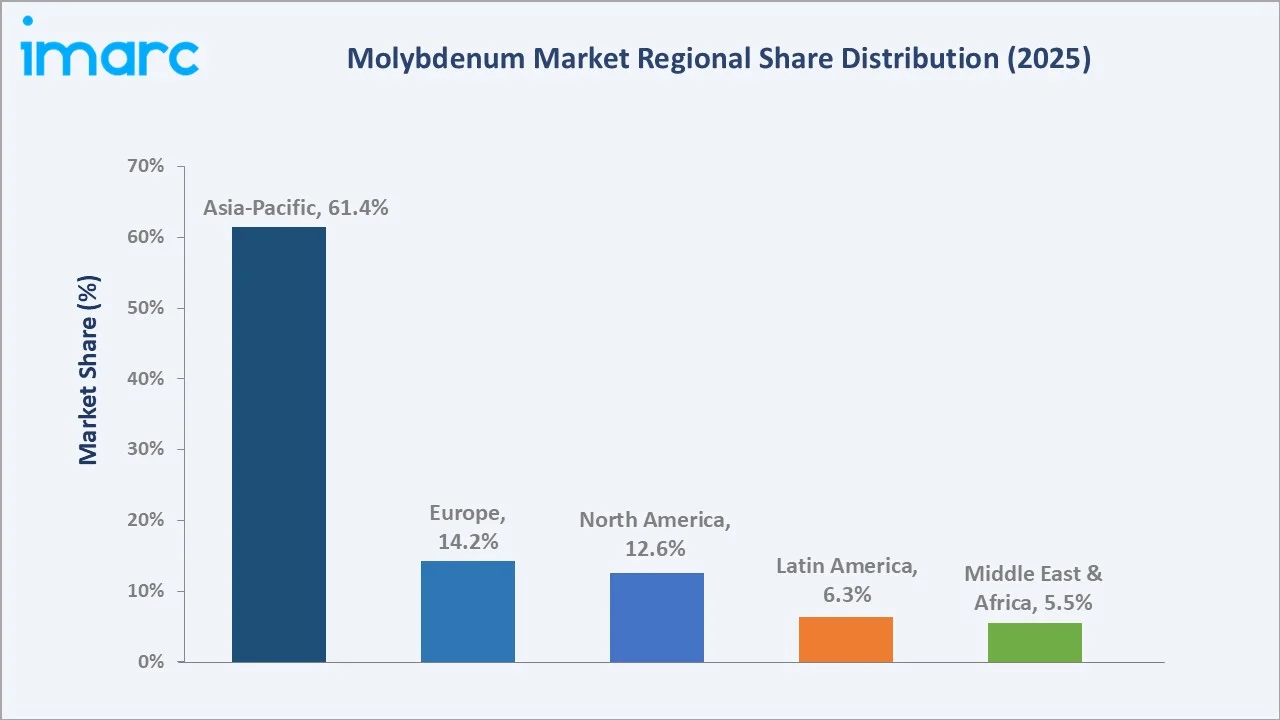

Steel dominates product type at 67.3% in 2025, while Asia-Pacific commands a dominant 61.4% regional share in 2025, reflecting China's unparalleled position as both a major producer and consumer of molybdenum.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

6.00 Thousand Tons |

|

Forecast Market Size (2034) |

7.32 Thousand Tons |

|

CAGR (2026-2034) |

2.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (61.4% share, 2025) |

|

Second Largest Region |

Europe (14.2% share, 2025) |

|

Leading Product Type |

Steel (67.3%, 2025) |

|

Leading Sales Channel |

Manufacturer/Distributor (88.2%, 2025) |

The global molybdenum market growth trajectory from 2020 through 2034, with historical expansion to 6.00 Thousand Tons in 2025, reflects consistent infrastructure- and steel-driven demand, while the forecast to 7.32 Thousand Tons captures accelerating renewable energy investment, semiconductor manufacturing expansion, and Asia-Pacific industrialization-led demand through the forecast period.

To get more information on this market, Request Sample

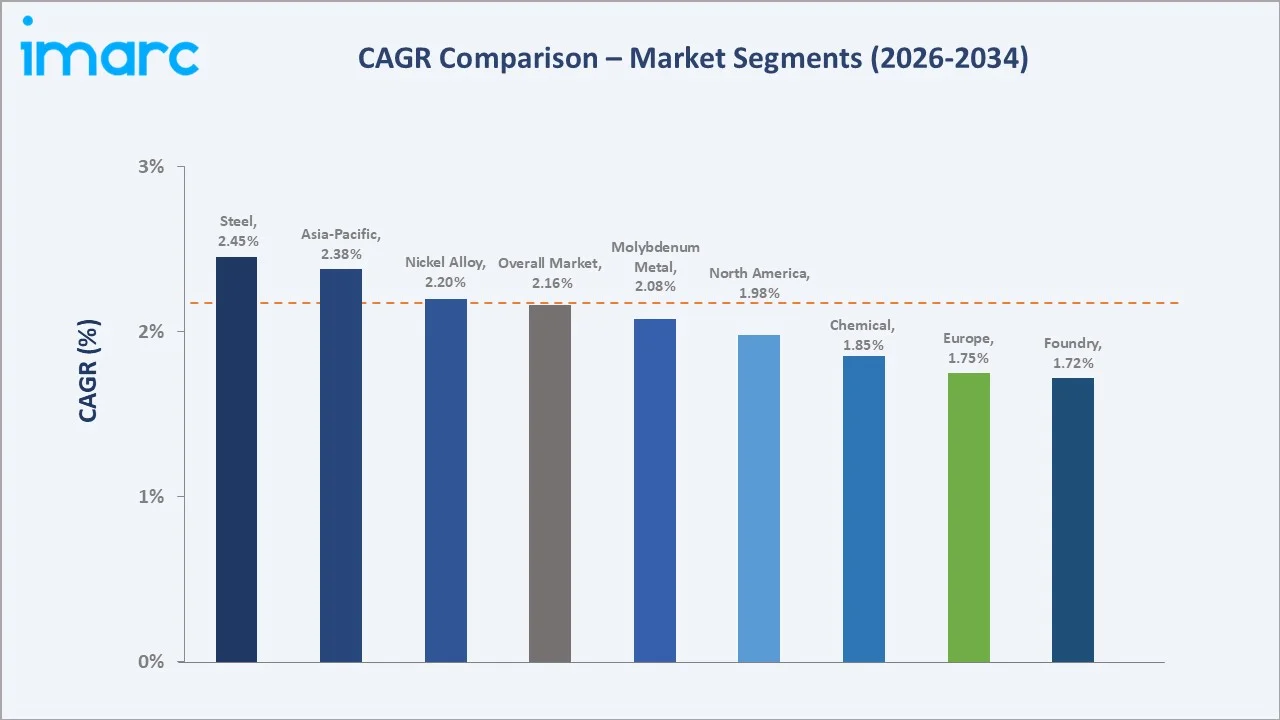

The CAGR trajectories across key product type, sales channel, and regional sub-segments – with Steel at ~2.45% CAGR and Asia-Pacific at ~2.38% CAGR – are among the fastest-growing categories within the global molybdenum industry through 2034. The overall market CAGR of 2.16% underscores steady, industrial-demand-driven growth rather than cyclical commodity speculation.

Executive Summary

The global molybdenum market is on a sustained growth trajectory from 6.00 Thousand Tons in 2025 to 7.32 Thousand Tons by 2034. Molybdenum, an essential refractory metal and alloying element deployed across steel manufacturing, chemical processing, foundry operations, and advanced alloys, benefits from the non-discretionary nature of its industrial demand and diverse end-use applications.

Steel dominates product type at 67.3% in 2025, owing to molybdenum's indispensable role in producing high-strength, corrosion-resistant steel grades for automotive, construction, and pipeline infrastructure sectors. Chemical applications (9.4%) are critical for hydrodesulfurization catalysts in petroleum refining and fertilizer production. Foundry uses (8.1%) leverage molybdenum for high-performance cast alloys.

Asia-Pacific dominates at 61.4% in 2025, reflecting China's position as both the world's largest steel producer and a leading molybdenum mining nation. Europe (14.2%) and North America (12.6%) follow, driven by specialty steel manufacturing, aerospace and defense procurement, and semiconductor fabrication expansion respectively.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Steel – 67.3% share (2025) |

|

Second Product Type |

Chemical – 9.4% share (2025) |

|

Leading Sales Channel |

Manufacturer/Distributor – 88.2% (2025) |

|

Leading Region |

Asia-Pacific – 61.4% share (2025) |

|

Second Largest Region |

Europe – 14.2% share (2025) |

|

Top Companies |

CMOC, Freeport-McMoRan, Jinduicheng Molybdenum Co., Ltd, Rio Tinto |

Key Analytical Observations Expanding on the Above Data:

- Steel Segment: Steel's 67.3% dominance in 2025 is underpinned by molybdenum's indispensable role in high-strength low-alloy (HSLA) steels and stainless-steel grades used in oil & gas pipelines, chemical processing equipment, and structural construction globally.

- Sales Channel: Manufacturer/distributor channel accounts for 88.2% because major mining companies supply directly to steel mills and industrial chemical producers under long-term offtake agreements, ensuring stable volume commitments and price transparency.

- Asia-Pacific Dominance: Asia-Pacific's 61.4% share reflects China's combined role as the world's top steel producer and a major molybdenum mining nation, creating deeply integrated domestic supply and demand dynamics unavailable in any other global region.

Global Molybdenum Market Overview

Molybdenum is a refractory metal characterized by a high melting point of 2,623°C, exceptional strength-to-weight ratio, and outstanding corrosion resistance. It is primarily produced as a byproduct of copper mining and as a primary product from dedicated molybdenite mines, with China, Chile, and the United States as the dominant producing nations accounting for over 80% of global mined output.

The global ecosystem integrates primary mining companies, roasting and conversion facilities, ferromolybdenum and molybdic oxide producers, steel mills, chemical manufacturers, specialty alloy producers, and diverse end-use industries spanning oil and gas, aerospace and defense, power generation, automotive, construction, and electronics sectors across all major world regions.

Market Dynamics

To evaluate market opportunities, Request Sample

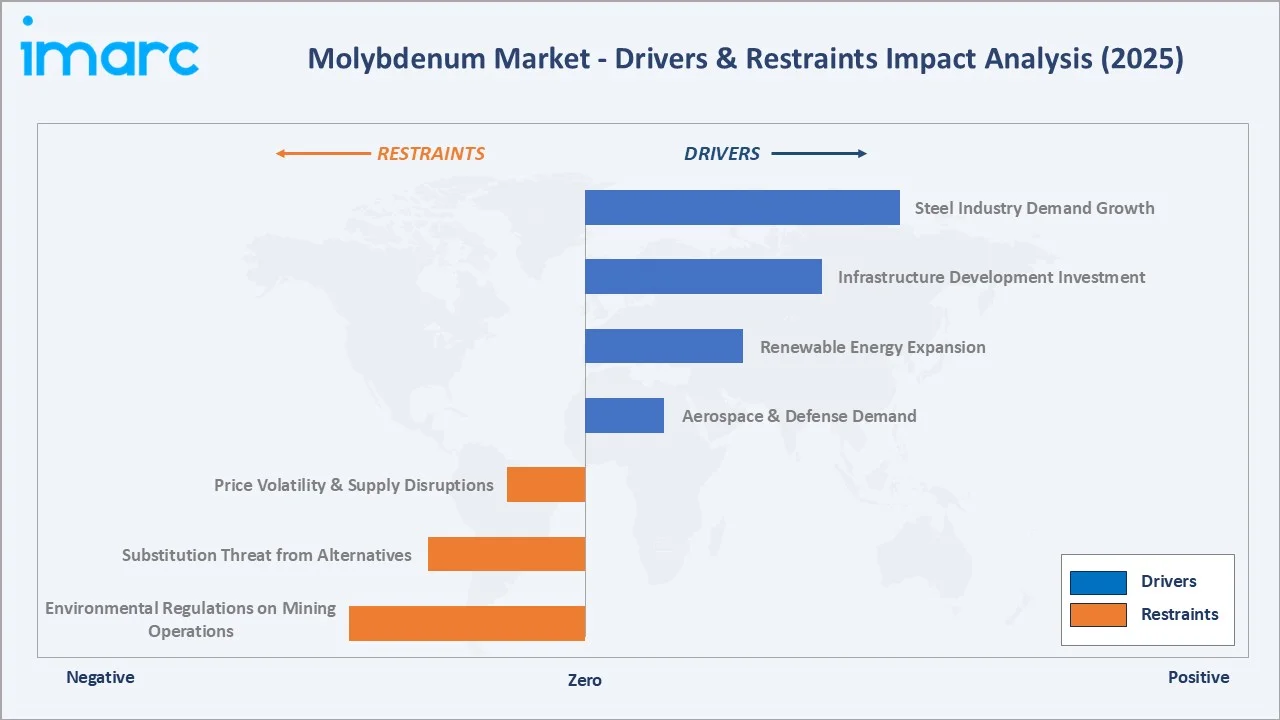

Market Drivers

- Steel Industry Demand Growth: Global crude steel output reached approximately 1.89 billion Tons in 2023, with molybdenum-alloyed steels capturing growing specification share in HSLA, stainless, and tool steel grades. Expanding automotive lightweighting requirements and global pipeline infrastructure investment drive consistent, predictable molybdenum demand.

- Infrastructure Development Investment: Global infrastructure investment needs of USD 94 Trillion through 2040, as estimated by the World Bank, are creating large-scale procurement of molybdenum-alloyed structural steels, pressure vessels, and corrosion-resistant pipelines across bridges, power plants, and water treatment facilities in both developed and developing markets.

- Renewable Energy Expansion: IEA data shows global energy-related CO₂ emissions exceeded 36.8 Gt in 2022, accelerating renewable energy investment. Wind turbine shafts, solar panel mounting systems, and green hydrogen electrolysis equipment demand high-performance molybdenum-bearing alloys that provide the necessary durability in harsh operating environments and thermal cycling conditions.

- Aerospace & Defense Demand: Aerospace sector dependence on molybdenum-based superalloys for engine turbine components exposed to extreme temperatures, combined with growing global defense procurement, establishes a high-value, specification-driven demand stream that remains insulated from commodity price cycles due to rigorous qualification requirements.

Market Restraints

- Price Volatility & Supply Disruptions: The molybdenum market continues to experience periodic price fluctuations due to changing mining activity, global economic conditions, and geopolitical uncertainties. Such volatility creates challenges for procurement planning and cost management among steel producers and alloy manufacturers, particularly those operating under long-term or fixed-price contracts. In addition, supply chain disruptions and variations in raw material availability can impact production schedules and purchasing strategies across downstream industries.

- Substitution Threat from Alternative Alloying Elements: Vanadium and niobium offer competitive performance in certain HSLA steel applications at potentially lower cost points, incentivizing steel producers to reformulate alloy chemistries when molybdenum prices spike, creating demand elasticity that can moderate long-term pricing power for molybdenum producers.

- Environmental Regulations on Mining Operations: Increasingly stringent mining regulations in Chile, China, and the United States, including water use restrictions, tailings management standards, and mandatory carbon reporting requirements, raise operating costs and constrain capacity expansion timelines for primary molybdenum mining operations.

Market Opportunities

- Capacity Expansion in Copper-Molybdenum Mining: Major copper mine expansions such as Freeport-McMoRan's USD 7.5 Billion El Abra project in Chile will produce significant molybdenum byproduct, while new applications in green hydrogen infrastructure and electric vehicle motor alloys create incremental demand streams that diversify the market beyond its traditional steel dependency.

- Emerging High-Value Technology Applications: Advanced alloy development for 3D-printed aerospace components, next-generation nuclear reactor pressure vessels, and ultra-deepwater oil drilling equipment is creating premium application demand that requires molybdenum's unique combination of high-temperature strength, corrosion resistance, and machinability.

Market Challenges

- Byproduct Supply Dependency: A significant share of global molybdenum supply is generated as a byproduct of large-scale copper mining operations. As a result, production levels are often influenced by trends and investment activity in the copper industry rather than direct demand for molybdenum itself. This dependency can lead to supply-demand imbalances, creating market uncertainty and affecting availability, pricing dynamics, and long-term supply stability for end-use industries.

- Geopolitical Concentration Risk: China's dominant position in both molybdenum mining and downstream processing creates supply concentration risk for Western industrial consumers, particularly relevant given ongoing trade policy tensions and the growing strategic focus on critical mineral supply chain security among major industrialized economies.

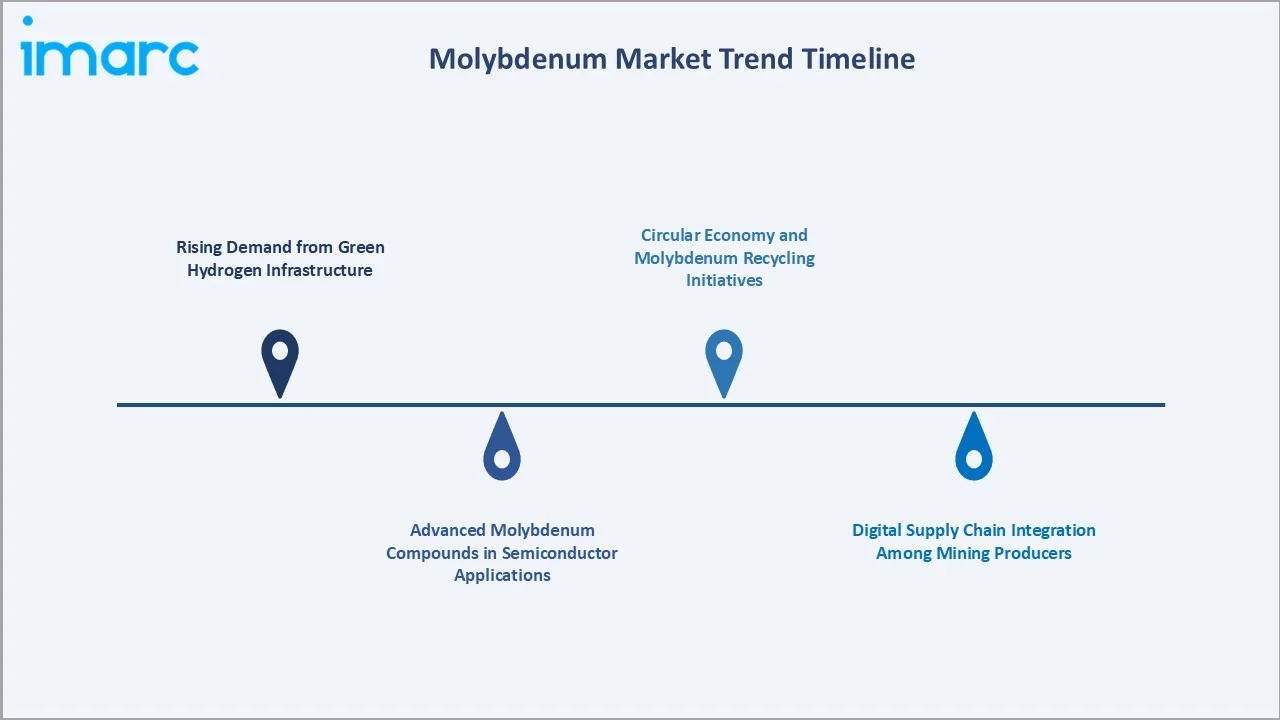

Emerging Market Trends

1. Rising Demand from Green Hydrogen Infrastructure

Global green hydrogen investment is accelerating, with molybdenum-bearing stainless steel and nickel alloys essential for electrolysis cells, high-pressure storage vessels, and hydrogen distribution pipelines. This structurally new demand stream is independent of traditional steel construction cycles and supports premium pricing for high-purity molybdenum products meeting hydrogen sector material specifications.

2. Advanced Molybdenum Compounds in Semiconductor Applications

Molybdenum disulfide (MoS₂) is emerging as a key two-dimensional material for next-generation transistors, dry lubricant coatings, and photovoltaic cells. Semiconductor manufacturing capacity expansion under major government subsidy programs globally is increasing demand for high-purity molybdenum sputtering targets used in thin-film deposition processes across advanced logic and memory chip fabrication.

3. Circular Economy and Molybdenum Recycling Initiatives

Growing emphasis on critical mineral recycling is prompting steel recyclers and specialty alloy producers to recover molybdenum from end-of-life steel scrap. Secondary molybdenum recovery from spent catalysts in petroleum refineries is increasing, reducing primary mining dependency and improving supply chain resilience for industrial consumers prioritizing sustainable procurement practices.

4. Digital Supply Chain Integration Among Mining Producers

Leading molybdenum producers are implementing IoT-enabled processing optimization, AI-driven ore grade prediction, and blockchain-based provenance tracking across their mining and processing operations. These investments reduce unit processing costs, improve molybdenum recovery rates from ore, and meet increasingly stringent ESG due diligence requirements from major industrial buyers in regulated markets.

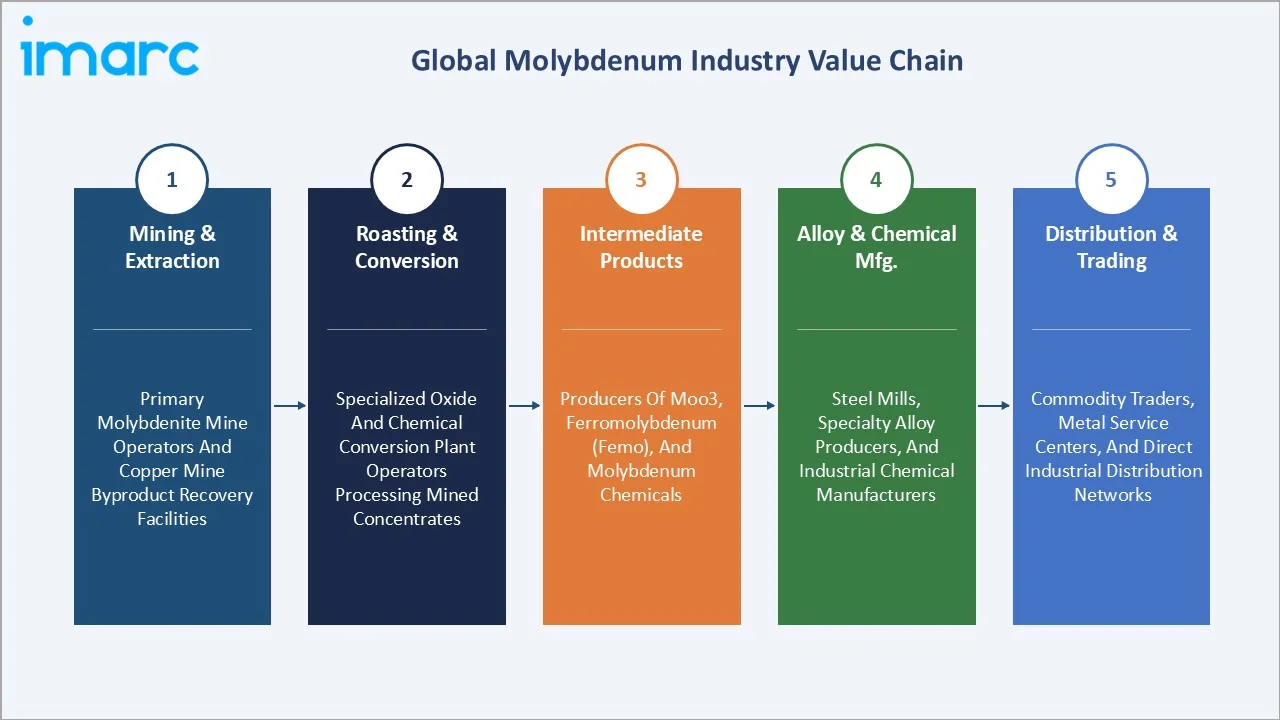

Industry Value Chain Analysis

The molybdenum value chain spans five stages from ore extraction through to end-use manufacturing. Roasting and chemical conversion capture the highest processing margins, while primary mining scale determines overall cost competitiveness in commodity-grade supply segments. Vertically integrated producers achieving captive coverage across multiple stages maintain the strongest competitive positions in price-sensitive markets.

|

Stage |

Description |

|

Mining & Extraction |

Primary molybdenite mine operators and copper mine byproduct recovery facilities |

|

Roasting & Conversion |

Specialized oxide and chemical conversion plant operators processing mined concentrates |

|

Intermediate Products |

Producers of molybdic oxide (MoO₃), ferromolybdenum (FeMo), and molybdenum chemicals |

|

Alloy & Chemical Mfg. |

Steel mills, specialty alloy producers, and industrial chemical manufacturers |

|

Distribution & Trading |

Commodity traders, metal service centers, and direct industrial distribution networks |

Technology Landscape in the Molybdenum Industry

Advanced Hydrometallurgical Processing

Pressure oxidation and solvent extraction-electrowinning (SX-EW) technologies are progressively improving molybdenum recovery rates from low-grade copper porphyry ores. These processes achieve recovery efficiencies above 85%, reducing mining waste and improving economics for byproduct molybdenum operations attached to large-scale copper mining complexes in Chile, Peru, and the United States.

High-Purity Molybdenum for Semiconductor Applications

Demand for 99.999% purity molybdenum sputtering targets for semiconductor fab deposition processes is driving investment in zone-refining and electron beam melting technologies. Leading specialty metal producers have developed proprietary purification processes meeting SEMI standards for critical electronic material specifications required by advanced logic chip fabrication at sub-5nm process nodes.

Additive Manufacturing with Molybdenum Alloys

Selective laser melting (SLM) and electron beam melting (EBM) of molybdenum powder enable production of complex refractory components for aerospace and nuclear applications previously impossible through conventional machining methods. These technologies reduce material waste by up to 70% compared to subtractive manufacturing and enable design geometries with internal cooling channels critical for turbine applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Steel |

67.3% |

2025 |

|

Sales Channel |

Manufacturer/Distributor |

88.2% |

2025 |

|

End Use |

🔒 |

🔒 |

2025 |

|

Region |

Asia-Pacific |

61.4% |

2025 |

By Product Type

Steel dominates the molybdenum market at 67.3% in 2025, reflecting its indispensable role as an alloying element in high-strength low-alloy (HSLA), tool, and stainless steels. The automotive, construction, and oil & gas industries' continuous demand for high-performance steel with enhanced corrosion resistance and mechanical properties underpins this segment's structural dominance through the forecast period.

To access detailed market analysis, Request Sample

Chemical applications (9.4%) in 2025 are essential for hydrodesulfurization catalysts in petroleum refining, fertilizer production, and specialty dye manufacturing. Foundry applications (8.1%) utilize molybdenum in high-strength cast iron and superalloy castings for demanding mechanical engineering environments requiring exceptional fatigue resistance and dimensional stability at elevated operating temperatures.

By Sales Channel

Manufacturer/distributor channel dominates at 88.2% in 2025, reflecting the structure of molybdenum's industrial supply chain where major mining companies supply directly to steel mills and chemical producers under long-term bilateral contracts or through specialized commodity traders handling physical delivery, quality assurance, and logistics for bulk industrial volumes across global markets.

Aftermarket channel (11.8%) represents secondary market transactions including spot trading, recycled molybdenum recovered from spent catalysts and scrap steel, and small-volume specialty chemical purchases. Growing catalyst recycling programs at petroleum refineries and increasing scrap steel molybdenum recovery are gradually expanding aftermarket share as circular economy practices intensify across industries.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

61.4% |

Leading steel and alloy demand; dominant molybdenum production base; electronics and infrastructure growth |

|

Europe |

14.2% |

Specialty steel and superalloy manufacturing; renewable energy investment; high-value chemical applications |

|

North America |

12.6% |

Aerospace and defense procurement; semiconductor manufacturing expansion; energy sector demand |

|

Latin America |

6.3% |

Copper-molybdenum byproduct mining operations; growing domestic steel consumption |

|

Middle East & Africa |

5.5% |

Industrial diversification programs; oil & gas sector alloy demand; infrastructure construction |

Asia-Pacific's 61.4% dominance in 2025 is driven by the region's unparalleled combination of molybdenum production capacity and consumption depth. The region's steel industry, led by China's molybdenum resource of about 8.3 million tonnes and an annual production capacity of about 100,000 tonnes, requires significant molybdenum additions for HSLA and stainless grades, while growing electronics and chemical sectors expand non-steel demand applications.

Europe (14.2%) benefits from a highly specialized demand profile, with specialty steel producers in Germany, France, Sweden, and Austria using molybdenum extensively in tool steels, stainless grades, and superalloys for automotive, aerospace, and energy applications. European Union decarbonization policy continues to drive green steel investment that sustains molybdenum specification demand into the forecast period.

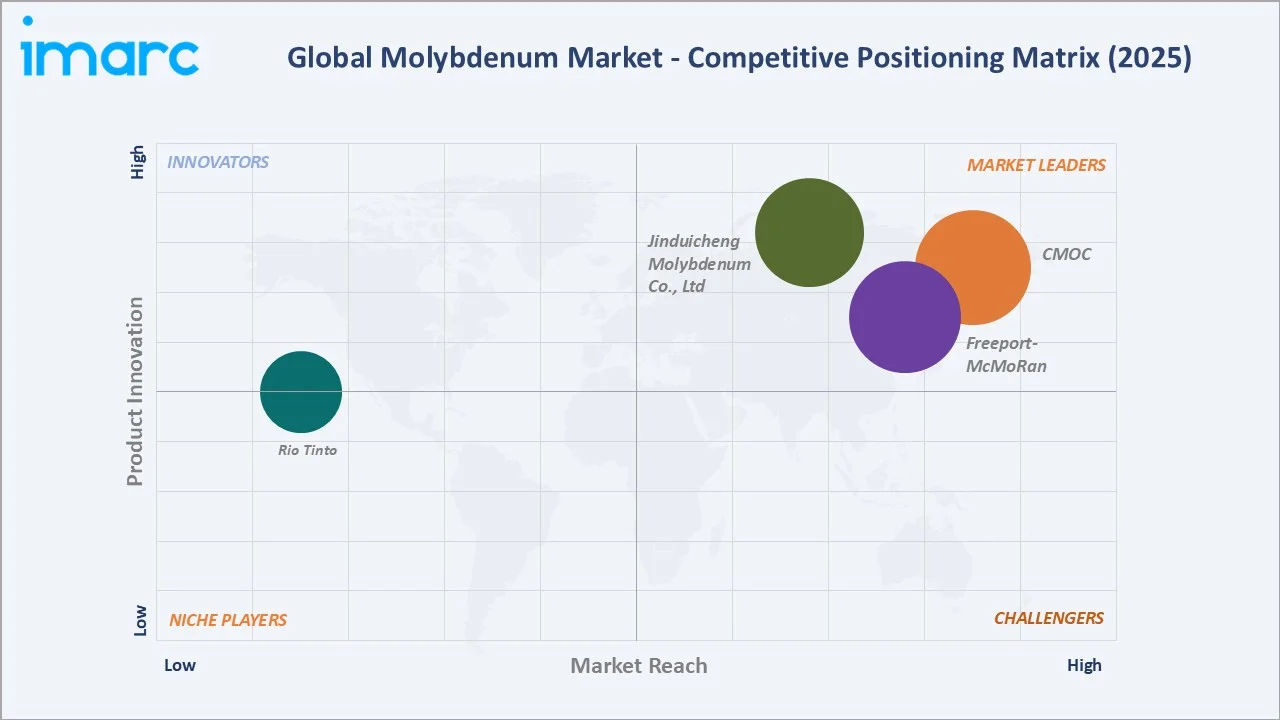

Competitive Landscape

The global molybdenum market is moderately concentrated, with a small number of large mining companies holding significant production share through integrated copper-molybdenum mining operations in Chile, the United States, China, and Mexico. Primary molybdenum producers compete on production cost, product quality and consistency, and supply reliability under long-term industrial customer contracts.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

CMOC |

Molybdenum |

Leader |

Asia-Pacific & global; diversified mining; integrated processing |

|

Freeport-McMoRan |

Molybdenum |

Leader |

Market leader; dedicated primary molybdenum mines |

|

Jinduicheng Molybdenum Co., Ltd |

Molybdenum chemical, Molybdenum metal |

Leader |

China domestic leader; primary moly mine; vertically integrated |

|

Rio Tinto |

Unroasted Molybdenum Concentrate, Roasted Molybdenum Concentrate (Oxide Powder), Roasted Molybdenum Concentrate (Briquettes) |

Emerging |

Global diversified miner; molybdenum from Kennecott copper-molybdenum mine (Utah) |

Key players include CMOC, Freeport-McMoRan, Jinduicheng Molybdenum Co., Ltd, Rio Tinto, and others.

Key Company Profiles

Freeport-McMoRan

Freeport-McMoRan is one of the world's largest publicly traded copper companies and molybdenum producers. The company operates the only two dedicated primary molybdenum mines in the United States, the Climax and Henderson mines in Colorado, via its subsidiary Climax Molybdenum Company

- Product Portfolio: Offers Molybdenum

- Strategic Focus: Freeport's molybdenum strategy leverages its unique position as the operator of dedicated primary molybdenum mines to maintain supply continuity independent of copper market cycles, while expanding byproduct recovery and targeting specialty alloy customers requiring traceable, high-purity North American molybdenum supply.

CMOC

CMOC Group is one of the world's largest diversified mining companies, with operations spanning molybdenum, tungsten, copper, cobalt, and niobium. CMOC operates major molybdenum mines domestically while managing large-scale copper-cobalt operations in the Democratic Republic of Congo, creating a globally diversified critical minerals portfolio.

- Product Portfolio: Offers Molybdenum

- Strategic Focus: CMOC's strategy focuses on vertical integration from primary mining through chemical conversion, leveraging China's deep domestic steel industry as a captive end-market while expanding global reach through targeted acquisitions and positioning CMOC as a full-service molybdenum supplier for both commodity and specialty grade requirements.

Market Concentration Analysis

The global molybdenum market is moderately concentrated, with five to seven major producers accounting for approximately 65–70% of global primary molybdenum supply. Asia-Pacific, representing 61.4% of demand, is served substantially by domestic producers, while the Americas market is dominated by major integrated copper-molybdenum mining companies operating large-scale mines in Chile, the United States, and Mexico.

China's dual role as both the largest producer and consumer creates a structurally segmented global market. Domestic supply is largely captive to domestic steel and chemical industries, while international trade flows are determined by primary producers in Chile and the United States supplying European and North American specialty steel markets. M&A activity is increasing as industrial conglomerates acquire regional specialists.

Investment & Growth Opportunities

Fastest-Growing Segments

Molybdenum metal applications growing at ~2.08% CAGR through 2034 represent the highest-value segment, driven by semiconductor sputtering targets, high-temperature furnace components, and advanced aerospace alloys. Chemical applications at ~1.85% CAGR benefit from petroleum refining catalyst demand and emerging green chemical processing requirements that mandate high-performance catalytic materials.

Emerging Markets

Middle East and Africa at ~2.8% CAGR represents the fastest-growing region through 2034. Industrial diversification programs, manufacturing expansion, and South African mining infrastructure development are creating new molybdenum demand centers beyond traditional Asian and Western industrial market concentrations, offering expansion opportunities for global molybdenum suppliers.

Investment Trends

Strategic investment in molybdenum production is accelerating at the mining level, with multi-billion dollar copper mine expansions generating additional byproduct supply capacity. Green hydrogen infrastructure and semiconductor manufacturing represent the two highest-growth demand vectors, attracting technology-focused investment and premium pricing opportunities within the broader molybdenum market.

Future Market Outlook (2026-2034)

The global molybdenum market is forecast to expand from 6.00 Thousand Tons in 2025 to 7.32 Thousand Tons by 2034 at a CAGR of 2.16%, adding 1.32 Thousand Tons in incremental annual market volume over the forecast period. This consistent, sustained growth reflects the market's industrial-demand-driven characteristics and structural reliance on global steel production, infrastructure investment, and energy sector activity.

Three forces will most significantly shape the molybdenum industry landscape through 2034: green hydrogen infrastructure investment requiring corrosion-resistant molybdenum alloys, semiconductor fabrication expansion creating high-purity sputtering target demand, and continued Asia-Pacific urbanization sustaining baseline steel and foundry application consumption that forms the structural foundation of global molybdenum demand.

Research Methodology

Primary Research

Primary research encompassed structured interviews with molybdenum industry stakeholders including senior commercial managers at mining companies, procurement specialists at steel mills and alloy producers, and industry association data teams. Primary data validated market sizing, product type and sales channel segment shares, regional demand estimates, and technology adoption timelines for the forecast period.

Secondary Research

Key secondary sources include USGS Mineral Commodity Summaries (Molybdenum, 2020–2025), International Molybdenum Association (IMOA) statistical yearbooks, IEA World Energy Investment Report (2024), World Steel Association Steel Statistical Yearbook, SEC filings and annual reports of publicly traded molybdenum producers, and trade publications including Metal Bulletin and Mining Journal.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models, incorporating GDP growth indices, steel production forecasts, infrastructure investment pipelines, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for molybdenum price volatility and geopolitical supply disruption risk.

Molybdenum Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousand Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Steel, Chemical, Foundry, Molybdenum Metal, Nickel Alloy |

| Sales Channels Covered | Manufacturer/Distributor, Aftermarket |

| End Uses Covered | Oil and Gas, Automotive, Heavy Machinery, Energy, Aerospace and Defense, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | CMOC, Freeport-McMoRan, Jinduicheng Molybdenum Co., Ltd, Rio Tinto, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the molybdenum market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global molybdenum market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the molybdenum industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Molybdenum Market Report

The global molybdenum market reached 6.00 Thousand Tons in 2025, reflecting consistent demand from the global steel industry, infrastructure development programs, renewable energy expansion, and growing aerospace and defense procurement requirements across key industrial economies.

The market is projected to reach 7.32 Thousand Tons by 2034, growing at a CAGR of 2.16% during 2026-2034, driven by rising steel consumption in emerging economies, expansion of renewable energy infrastructure, and increasing adoption of molybdenum in semiconductor and advanced alloy applications.

Steel dominates with a 67.3% product type share in 2025, reflecting molybdenum's indispensable role in producing high-strength, corrosion-resistant steel alloys used across automotive, construction, pipeline, and industrial machinery applications globally.

The Manufacturer/Distributor channel leads at 88.2% in 2025, as major mining companies supply directly to steel mills and industrial chemical producers under long-term bilateral offtake contracts, ensuring stable volume commitments, quality assurance, and predictable pricing for bulk industrial consumers.

Asia-Pacific commands a dominant 61.4% market share in 2025, driven by China's position as both a major molybdenum producer and the world's largest steel manufacturing nation, combined with growing industrial and infrastructure demand across India, Japan, South Korea, and Southeast Asian economies.

Leading companies include CMOC, Freeport-McMoRan, Jinduicheng Molybdenum Co., Ltd, Rio Tinto, among others.

Key end-use industries include steel manufacturing, oil and gas exploration and processing, aerospace and defense, automotive, chemical processing, power generation, electronics, and construction. The steel industry alone accounts for over two-thirds of total molybdenum consumption globally in 2025.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)