United States Mobile Advertising Market Size, Share, Trends and Forecast by Format Type, Industry Vertical, and Region, 2026-2034

United States Mobile Advertising Market Size, Share, Trends & Forecast (2026-2034)

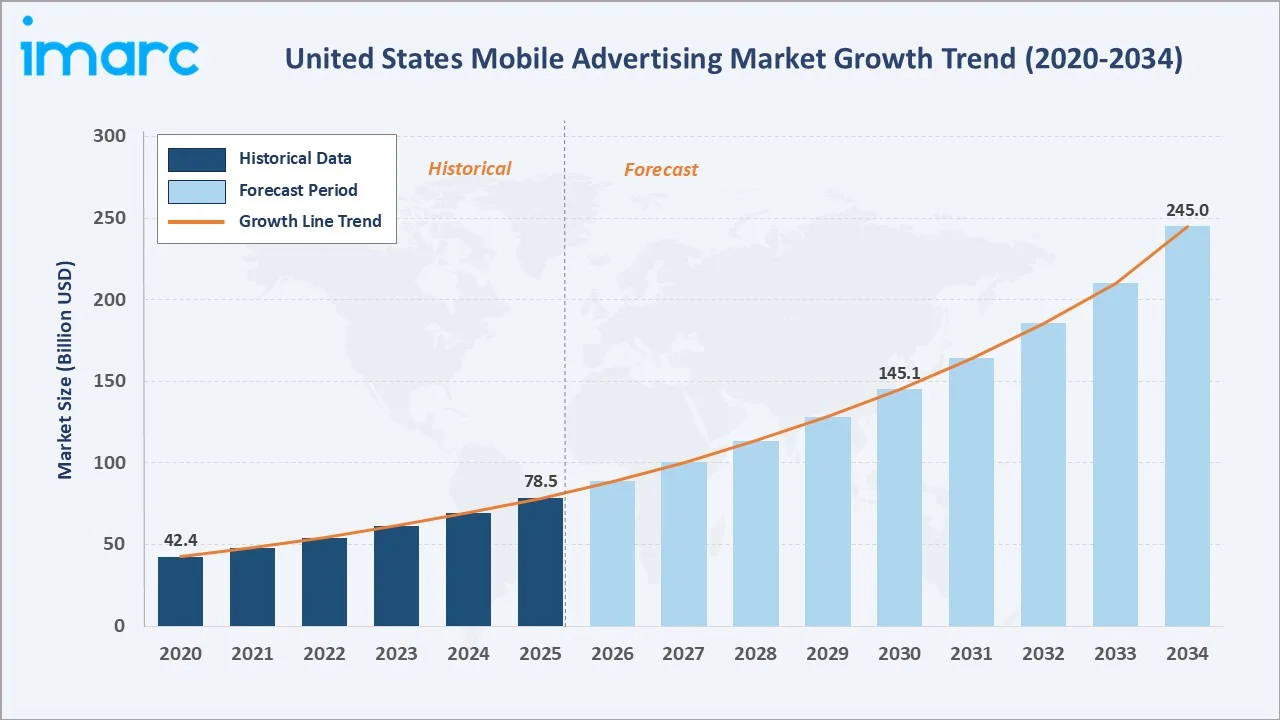

The United States mobile advertising market size increased from USD 78.5 Billion in 2025 to USD 88.72 Billion in 2026 and is projected to reach USD 245.0 Billion by 2034, growing at a CAGR of 13.09% during 2026-2034. The market is driven by the widespread adoption of smartphones, rising mobile internet usage, considerable growth in the popularity of mobile apps, advanced targeting and personalization capabilities offered by mobile advertising, and rapid modernization of ad formats.

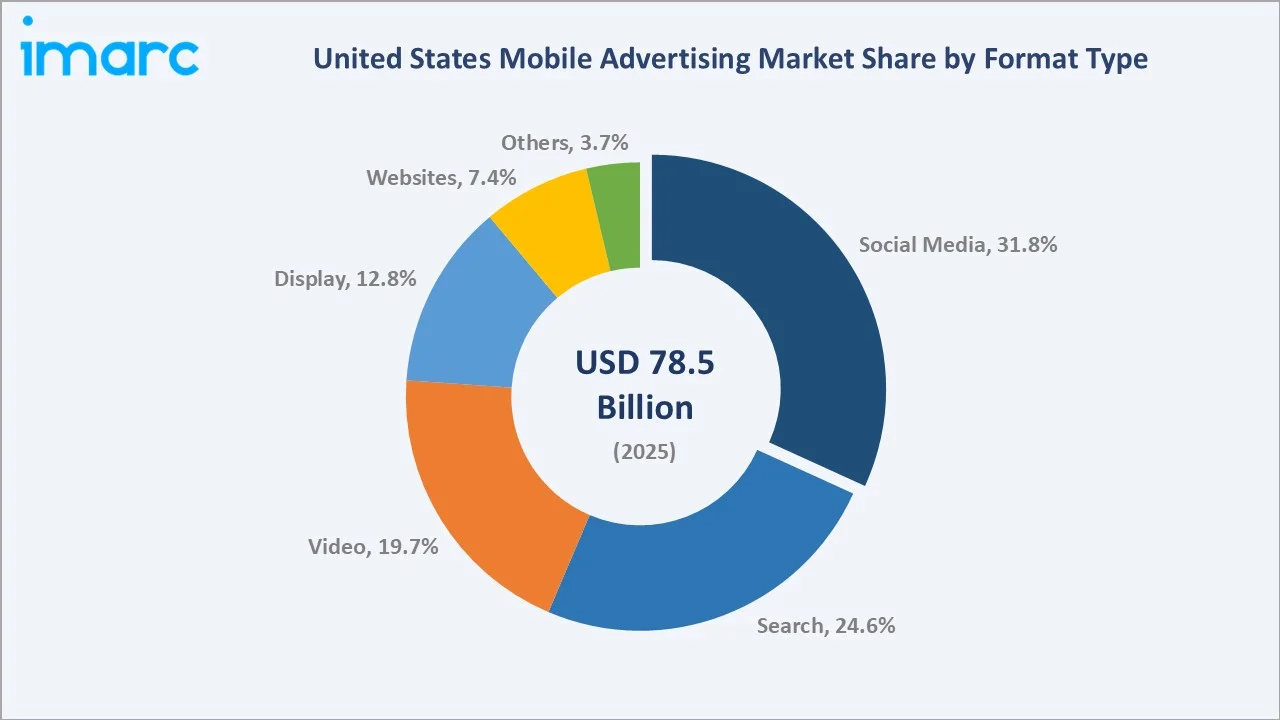

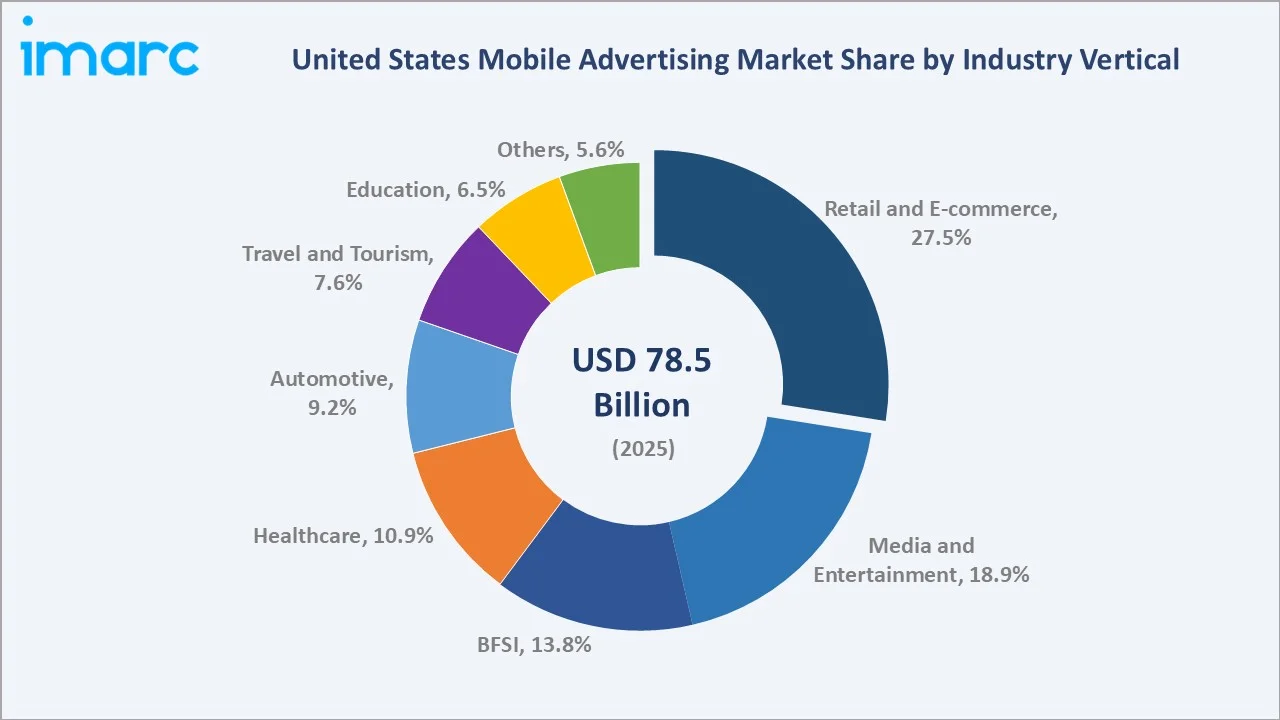

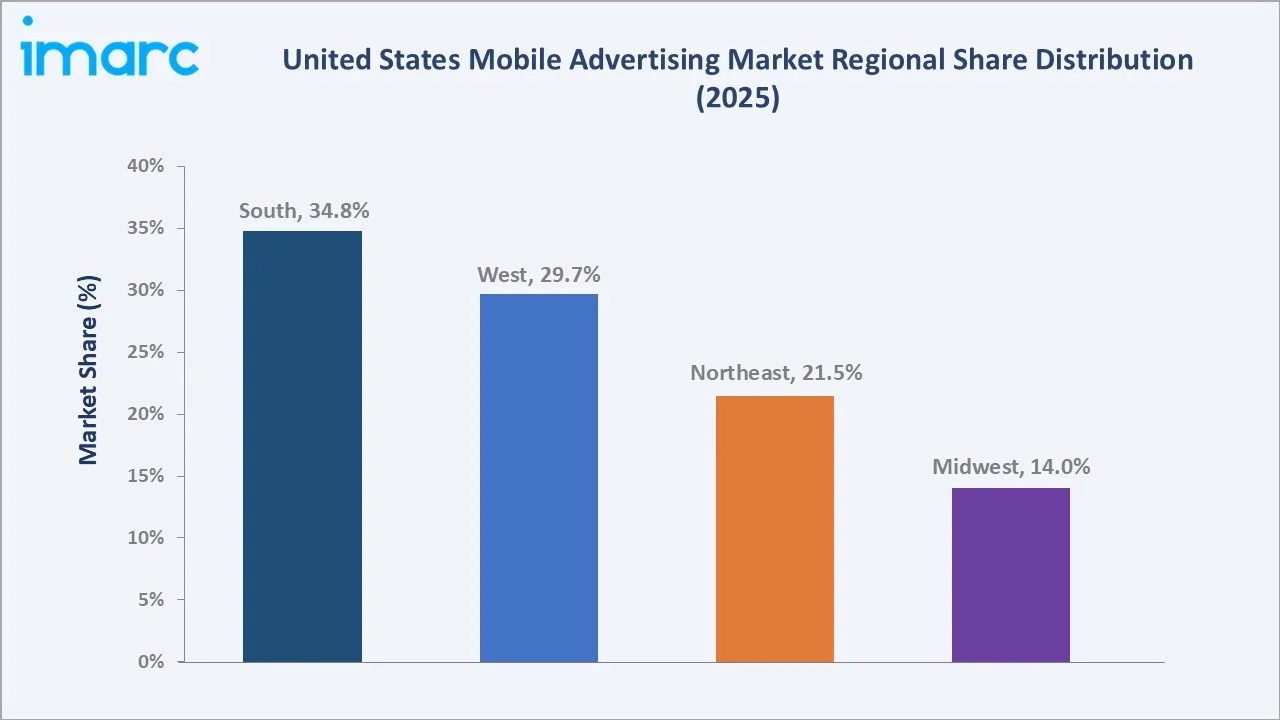

Social Media leads format type at 31.8%. Retail and E-commerce dominate industry verticals at 27.5%. The South region leads at 34.8% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Base Year Market Size (2025) |

USD 78.5 Billion |

|

Market Size (2026) |

USD 245.0 Billion |

|

Forecast Market Size (2034) |

USD 245.0 Billion |

|

CAGR (2026-2034) |

13.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Format Type |

Social Media (31.8%, 2025) |

|

Leading Industry Vertical |

Retail and E-commerce (27.5%, 2025) |

|

Leading Region |

South (34.8%, 2025) |

The market market grew from USD 42.4 Billion in 2020 to USD 78.5 Billion in 2025, reaching an estimated USD 245.0 Billion in 2026. anchored at USD 145.1 Billion in 2030 and forecast to reach USD 245.0 Billion by 2034. The COVID-19 pandemic accelerated the shift to digital advertising channels, with mobile capturing a disproportionate share of reallocated budgets as consumers shifted to smartphone-first content consumption behaviors that persisted and strengthened through the recovery period.

To get more information on this market, Request Sample

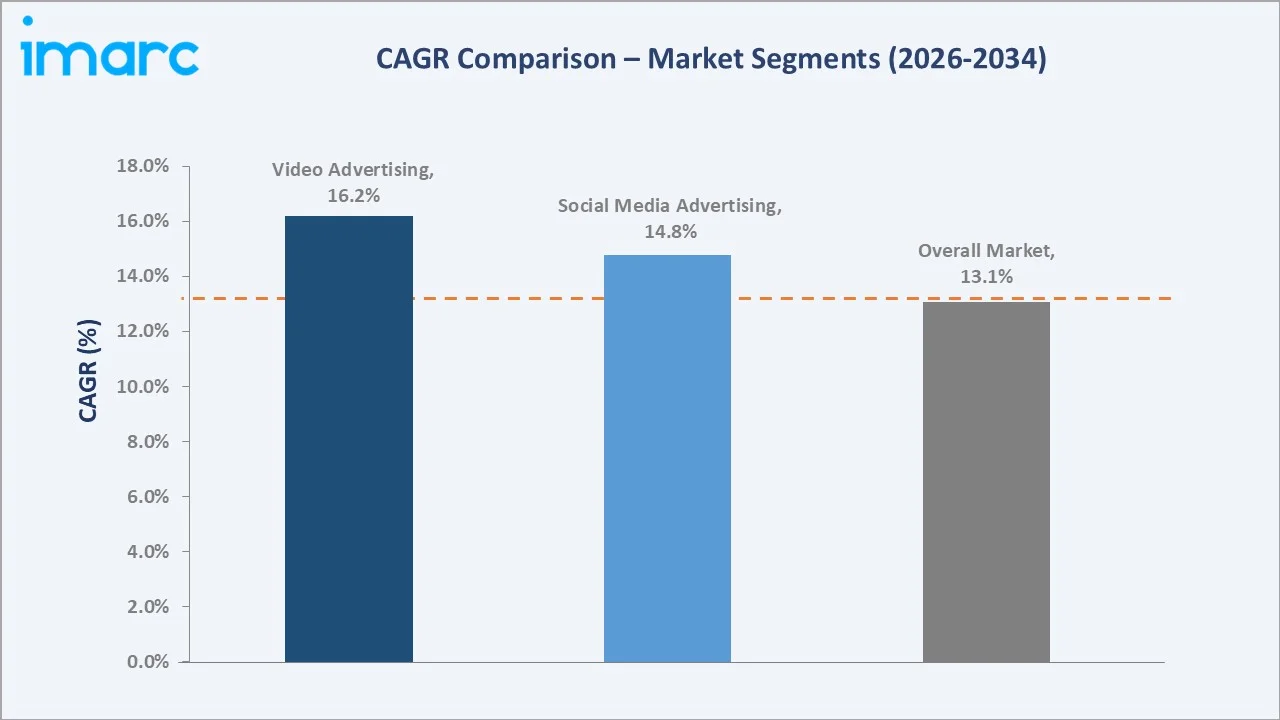

Social Media advertising grows at approximately 14.8% CAGR as Meta, TikTok, and Snapchat ecosystems expand advertising monetization and social commerce formats proliferate. Video advertising at approximately 16.2% CAGR is the fastest-growing format as short-form video content on TikTok, Instagram Reels, and YouTube Shorts attracts incremental advertiser budgets migrating from linear television.

Executive Summary

The United States mobile advertising market expanded from USD 78.5 Billion in 2025, to an estimated USD 88.72 Billion in 2026 representing one of the fastest-growing segments within the broader digital advertising ecosystem. Mobile advertising encompasses all promotional messages delivered to users via smartphones, tablets, and mobile-connected devices through formats including social media ads, search ads, video ads, display ads, and in-app placements. The market is projected to reach USD 245.0 Billion by 2034.

Social Media at 31.8% and Search at 24.6% collectively command over 56% of the 2025 market, reflecting the dominance of platform-based mobile advertising driven by Google and Meta. Retail and E-commerce at 27.5% leads industry verticals through performance marketing demands and mobile commerce growth. The South region at 34.8% leads nationally through concentration of major corporate headquarters and high-growth metropolitan areas.

Key Market Insights

|

Insight |

Data |

|

Dominant Format Type |

Social Media - 31.8% share (2025) |

|

Leading Industry Vertical |

Retail and E-commerce - 27.5% market share (2025) |

|

Leading Region |

South - 34.8% market share (2025) |

|

Market Opportunity |

AI-driven personalization, retail media networks, AR/VR ad formats, CTV convergence |

Key Analytical Observations Supporting The Above Data:

- Social Media at 31.8%: Social media advertising dominates due to high daily active user engagement rates on Facebook, Instagram, TikTok, and Snapchat. These platforms offer unmatched first-party audience data, native ad integration, and social commerce capabilities delivering premium advertiser returns on mobile, with Meta alone generating approximately USD 30 Billion in annual US mobile advertising revenues.

- Retail and E-commerce at 27.5%: Retail and e-commerce advertisers lead industry vertical spend driven by performance marketing requirements, the rise of social commerce and shoppable ad formats, and mobile-first shopping behaviors requiring persistent advertising presence throughout the consumer purchase journey to drive measurable conversion outcomes.

- South at 34.8%: The South region leads due to its concentration of major corporate headquarters in Texas, Florida, Georgia, and the Carolinas, combined with robust population growth attracting increased advertising investment and high digital adoption in rapidly growing metropolitan centers including Dallas, Atlanta, and Miami.

United States Mobile Advertising Market Overview

The United States mobile advertising market encompasses all digital advertising delivered through mobile devices, including smartphones and tablets, covering in-app advertising, mobile web advertising, social media advertising, mobile search, video advertising, and emerging formats such as augmented reality ads and interactive rich media. Mobile advertising leverages the unique features of mobile devices, including location data, touchscreens, and device-specific functionalities, to deliver personalized promotional messages driving consumer actions including app installations, website visits, and product purchases.

The ecosystem integrates advertisers and brands, advertising agencies, demand-side platforms, data management platforms, programmatic exchanges, supply-side platforms, mobile publishers and app developers, mobile measurement partners, and regulatory bodies including the FTC and state-level privacy agencies. Macroeconomic factors influencing the market include smartphone penetration rates, mobile internet usage growth, consumer spending patterns, privacy regulation evolution, and advancements in AI and machine learning for advertising optimization.

Market Dynamics

To evaluate market opportunities, Request Sample

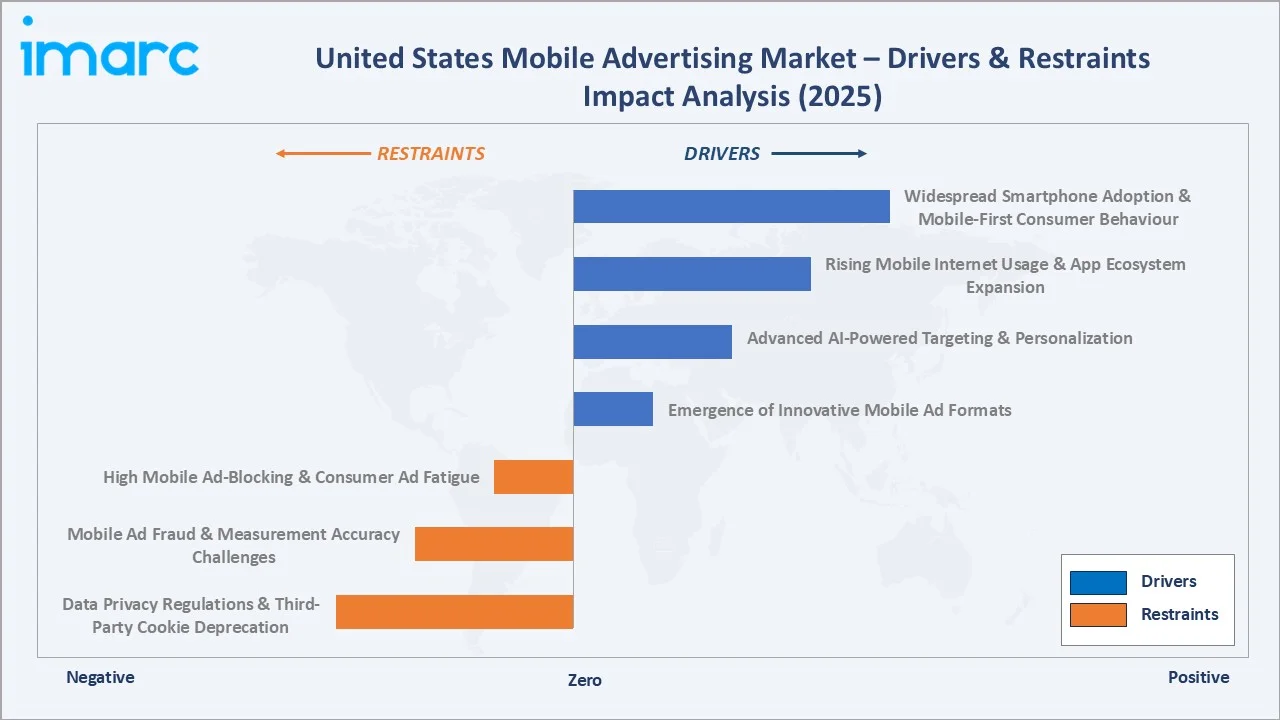

Market Drivers

- Widespread Smartphone Adoption and Mobile-First Consumer Behavior: The United States has one of the world's highest smartphone penetration rates, with over 300 million active smartphone users as of 2025. Mobile devices have become the primary screen for content consumption, social interaction, and commerce, with consumers spending an average of 4.5 hours per day on mobile applications. This ubiquitous smartphone presence creates unparalleled advertising reach for brands seeking to engage consumers across the entire purchase funnel, directly fueling sustained growth in mobile advertising expenditure across all format categories.

- Rising Mobile Internet Usage and App Ecosystem Expansion: Mobile internet consumption accounts for over 60% of total US digital media time, driven by the proliferation of mobile applications across social networking, gaming, entertainment, retail, and finance categories. The expanding mobile app ecosystem generates vast advertising inventory accessible through programmatic buying platforms, enabling precise audience targeting at population scale. In-app advertising captures consumers within high-engagement environments where ad format integration is seamless and conversion attribution is measurable through mobile measurement partners.

- Advanced AI-Powered Targeting and Personalization Capabilities: Artificial intelligence and machine learning technologies enable advertisers to analyze behavioral signals, location data, purchase intent patterns, and demographic attributes in real time to deliver hyper-personalized mobile advertising campaigns. AI-driven campaign optimization platforms automate bid adjustments, audience segmentation, and creative personalization, improving return on ad spend and democratizing access to performance-grade mobile advertising for mid-market advertisers who previously lacked the expertise to compete effectively against large brand advertisers.

- Emergence of Innovative Mobile Ad Formats and Rich Media Experiences: The continuous evolution of mobile ad formats, including short-form video ads, interactive rich media, augmented reality try-on experiences, and shoppable ad units, is expanding advertiser options and increasing consumer engagement rates. These innovative formats command premium CPMs and attract incremental advertising budgets from brands seeking differentiated mobile brand experiences. Interactive AR advertising deployed through Snapchat and Meta delivers engagement rates multiple times higher than standard banner ad formats, justifying premium pricing.

Market Restraints

- Data Privacy Regulations and Third-Party Cookie Deprecation: The proliferation of state-level privacy legislation including the California Consumer Privacy Act and equivalent regulations across 17 US states is constraining advertisers' ability to use third-party data for mobile audience targeting. Apple's App Tracking Transparency framework has significantly reduced mobile identifier availability, and evolving privacy standards are reshaping programmatic mobile advertising infrastructure, creating targeting inefficiencies and increased compliance costs for advertisers reliant on cross-app behavioral data for campaign optimization.

- Mobile Ad Fraud and Measurement Accuracy Challenges: Ad fraud including click injection, SDK spoofing, and bot traffic continues to erode mobile advertising returns, with industry estimates suggesting 10-15% of mobile ad spend is affected by fraudulent activity. Attribution fragmentation across walled garden platforms operated by Meta, Google, and Apple, combined with open programmatic environments, creates measurement gaps reducing advertiser confidence and complicating cross-channel return on investment assessment, particularly for mid-market advertisers lacking sophisticated fraud detection infrastructure.

- High Mobile Ad-Blocking Adoption and Consumer Ad Fatigue: Increasing consumer adoption of ad-blocking tools on mobile browsers, combined with growing ad fatigue from overexposure to intrusive mobile formats including interstitials and pop-ups, reduces effective reach for advertisers. Poor mobile ad experiences driven by slow-loading creatives, disruptive placements, and irrelevant targeting drive user avoidance behaviors limiting advertiser access to engaged audiences and reducing campaign conversion rates, particularly among younger demographics most proficient at avoiding unwanted advertising exposure.

Market Opportunities

- AI and Generative AI Integration for Creative Automation: The integration of generative AI tools into mobile advertising workflows enables brands to produce thousands of personalized creative variants at scale, enabling hyper-personalized campaigns that improve engagement rates without proportional increases in production costs. Automated creative optimization continuously tests and rotates ad variants to identify highest-performing combinations, driving sustained campaign performance improvements throughout campaign flight periods across all mobile advertising formats.

- Connected TV and Cross-Screen Mobile Advertising Convergence: The convergence of mobile and connected TV advertising enables brands to execute sequential storytelling campaigns reaching consumers across mobile apps and streaming platforms, creating new multi-screen engagement opportunities. Retail media networks operated by major US retailers are expanding mobile advertising inventory, providing brands access to high-intent purchase audiences through first-party data-powered targeting delivering measurable conversion outcomes independent of third-party tracking infrastructure.

Market Challenges

- Walled Garden Fragmentation Limiting Cross-Platform Measurement: The concentration of mobile advertising inventory within closed ecosystems operated by Google, Meta, and Apple creates data silos preventing advertisers from measuring true cross-platform campaign performance. Each walled garden reports performance through proprietary attribution models that may inflate contribution metrics, making unified mobile advertising measurement and budget optimization across platforms inherently complex and contested among major technology platforms competing for advertising budget allocation.

- Rising Mobile Advertising CPMs and Competitive Inventory Pressures: Sustained demand growth for premium mobile advertising inventory is driving CPM inflation, particularly for video and social media formats, increasing the barrier for smaller advertisers to achieve cost-efficient reach. Competition from retail media networks redirecting brand budgets away from traditional programmatic channels is further fragmenting the mobile advertising landscape, requiring advertisers to maintain expertise across an increasing number of specialized platforms and inventory sources throughout the forecast period.

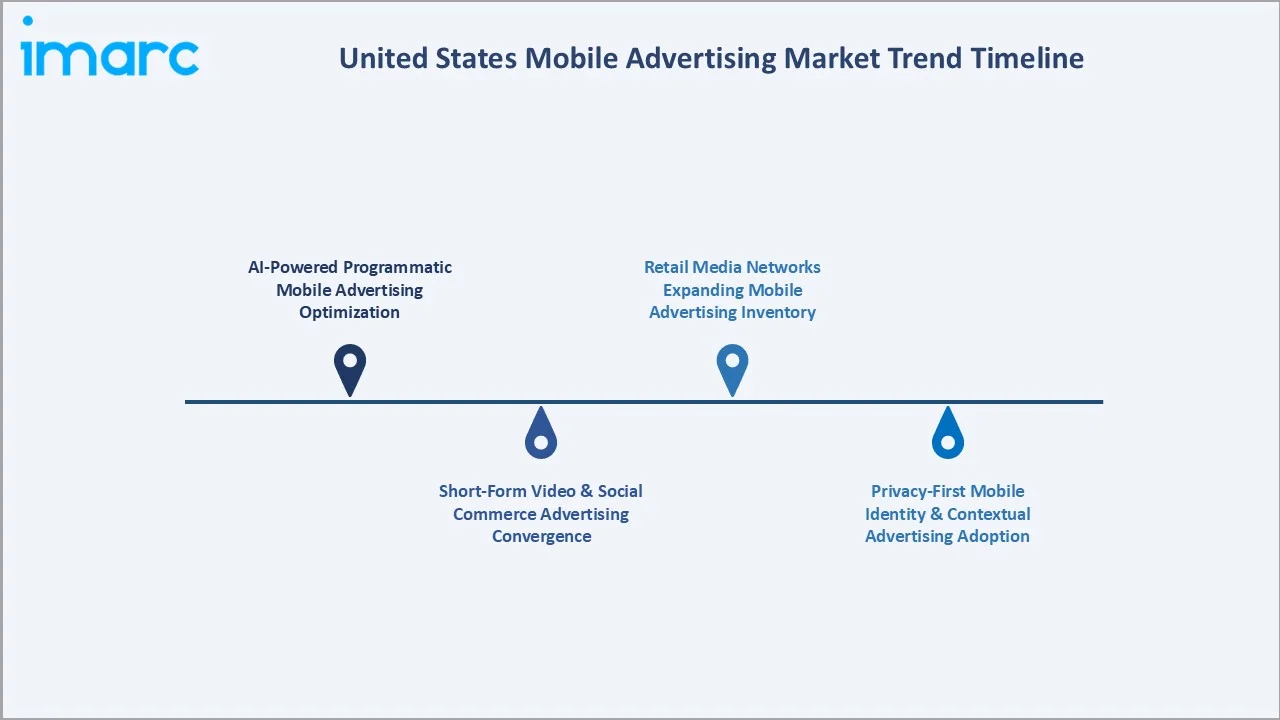

Emerging Market Trends

1. AI-Powered Programmatic Mobile Advertising Optimization

AI and machine learning are transforming programmatic mobile advertising by enabling real-time bid optimization, predictive audience targeting, and dynamic creative personalization. Advanced algorithms analyze billions of data signals per second to determine optimal ad placements, pricing, and creative combinations. Google launched AI-powered Performance Max campaigns with enhanced mobile optimization features, integrating Gemini AI for automated creative generation across all Google advertising surfaces including YouTube Shorts, demonstrating the accelerating integration of generative AI into mobile advertising workflows across the US market.

2. Short-Form Video and Social Commerce Advertising Convergence

The explosive growth of short-form video content on TikTok, Instagram Reels, and YouTube Shorts is creating high-engagement advertising environments on mobile platforms commanding premium CPMs and attracting substantial brand budget reallocation from linear television. Brands are integrating shoppable ad units directly within short-form video content, enabling seamless purchase experiences without leaving the platform environment. This social commerce convergence is driving measurable improvements in mobile advertising conversion rates and accelerating the shift of retail advertising budgets toward social media mobile formats throughout the forecast period.

3. Privacy-First Mobile Identity and Contextual Advertising Adoption

The decline of mobile device identifiers following Apple's App Tracking Transparency framework is accelerating adoption of privacy-preserving identity solutions, including contextual targeting, cohort-based audience models, and first-party data strategies. Advertisers are investing in customer data platforms and clean room technologies to activate their own customer data for mobile targeting without relying on third-party identifiers. This privacy-driven transformation is reshaping the mobile targeting infrastructure across the US advertising ecosystem, creating competitive advantages for platforms controlling first-party data at scale.

4. Retail Media Networks Expanding Mobile Advertising Inventory

Major US retailers including Amazon, Walmart, Target, and Kroger are scaling retail media networks offering advertisers access to first-party purchase intent data through mobile advertising channels. These networks enable brands to reach consumers on retailer mobile apps and websites at critical purchase decision moments, combining advertising reach with closed-loop conversion measurement demonstrating direct return on advertising investment without relying on cross-app tracking infrastructure. Retail media is attracting significant budget reallocation from traditional mobile advertising channels toward performance-measurable formats.

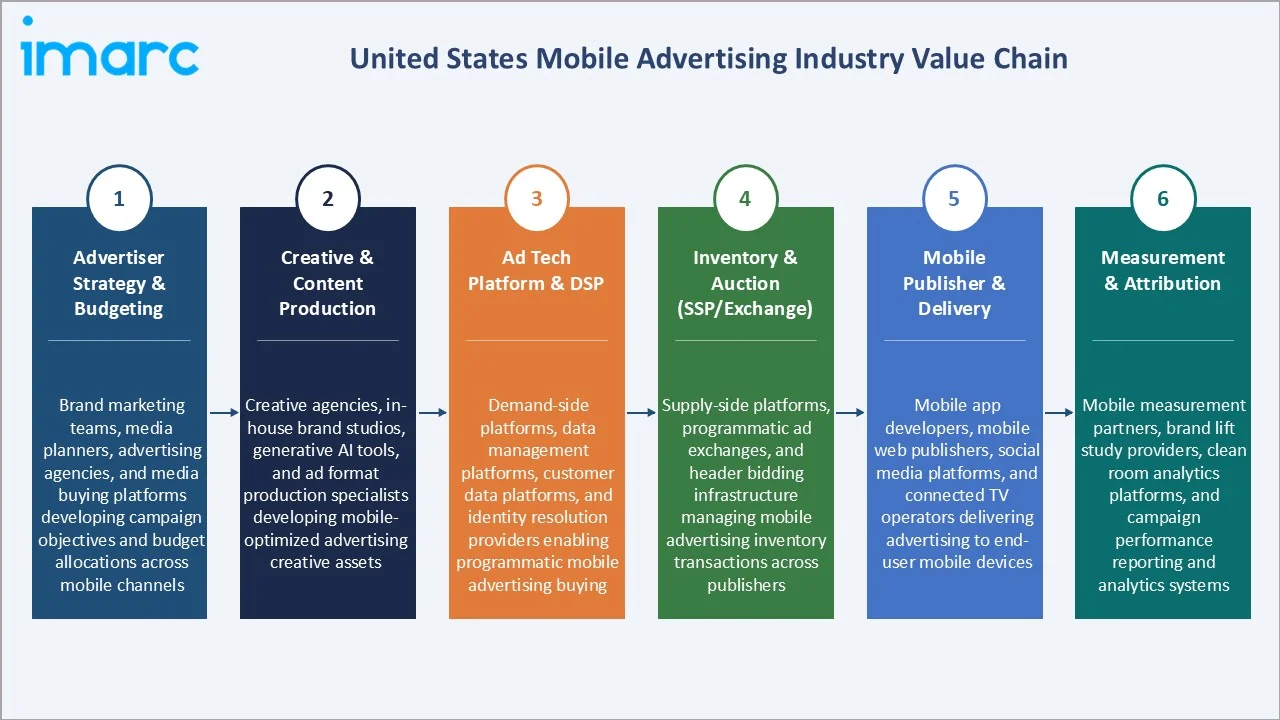

Industry Value Chain Analysis

The mobile advertising value chain integrates advertiser strategy and budget planning, creative and content production, ad technology platform and demand-side platform management, inventory procurement through supply-side platforms and exchanges, mobile publisher ad delivery, and performance measurement through mobile measurement partners. Platform intermediaries including demand-side platforms and supply-side platforms collectively earn 20-40% technology fees on programmatic transaction value, capturing the highest margins within the value chain architecture.

|

Stage |

Key Participants |

|

Advertiser Strategy & Budgeting |

Brand marketing teams, media planners, advertising agencies, and media buying platforms developing campaign objectives and budget allocations across mobile channels |

|

Creative & Content Production |

Creative agencies, in-house brand studios, generative AI tools, and ad format production specialists developing mobile-optimized advertising creative assets |

|

Ad Tech Platform & DSP |

Demand-side platforms, data management platforms, customer data platforms, and identity resolution providers enabling programmatic mobile advertising buying |

|

Inventory & Auction (SSP/Exchange) |

Supply-side platforms, programmatic ad exchanges, and header bidding infrastructure managing mobile advertising inventory transactions across publishers |

|

Mobile Publisher & Delivery |

Mobile app developers, mobile web publishers, social media platforms, and connected TV operators delivering advertising to end-user mobile devices |

|

Measurement & Attribution |

Mobile measurement partners, brand lift study providers, clean room analytics platforms, and campaign performance reporting and analytics systems |

The measurement and attribution tier is experiencing the most rapid restructuring as privacy regulations fragment mobile identity infrastructure. Mobile measurement partners that successfully develop privacy-preserving attribution methodologies command premium positioning as the measurability infrastructure justifying continued advertiser investment in mobile advertising despite tracking restrictions. The creative production tier is undergoing transformation driven by generative AI tools reducing the time and cost required to produce mobile-optimized ad creative at scale.

Technology Landscape in the United States Mobile Advertising Industry

Programmatic Advertising Technology

Programmatic advertising technology automates the buying and selling of mobile advertising inventory through real-time bidding auctions and private marketplace deals. Programmatic platforms leverage AI algorithms to evaluate audience signals and bid prices within milliseconds, enabling advertisers to reach target audiences across millions of mobile placements with precision and efficiency at scale. Programmatic now accounts for over 80% of total US digital advertising expenditure, with mobile programmatic representing the fastest-growing channel within the broader programmatic ecosystem.

AI and Machine Learning for Campaign Optimization

Artificial intelligence and machine learning capabilities embedded within demand-side platforms and campaign management platforms enable automated bid optimization, predictive audience modeling, and dynamic creative optimization. These technologies continuously analyze campaign performance signals to reallocate budgets toward the highest-performing placements and creative combinations, improving return on ad spend without manual intervention.

Mobile Attribution and Measurement Technology

Mobile attribution technology tracks consumer interactions across mobile touchpoints, mapping ad exposures and clicks to app installs, purchases, and other conversion events to demonstrate advertising return on investment. Privacy-preserving measurement solutions, including Apple's SKAdNetwork and evolving privacy sandbox frameworks are reshaping attribution infrastructure as mobile identifier availability declines.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Format Type |

Social Media |

31.8% |

2025 |

|

Industry Vertical |

Retail and E-commerce |

27.5% |

2025 |

|

Region |

South |

34.8% |

2025 |

By Format Type

Social Media advertising leads at 31.8% in 2025, anchored by Meta's family of apps encompassing Facebook, Instagram, and WhatsApp, TikTok's explosive advertising growth, and Snapchat's engaged young adult audience. Social media platforms offer unmatched first-party audience data, native ad integration, and social commerce capabilities, delivering premium advertiser returns on mobile investment across performance and brand advertising objectives.

To access detailed market analysis, Request Sample

Search advertising at 24.6% captures users at peak purchase intent moments, driven by Google's mobile search dominance and superior conversion rates of keyword-targeted campaigns. Video advertising at 19.7% is the fastest-growing format at approximately 16.2% CAGR, fueled by TikTok growth, YouTube mobile consumption, and migration of brand budgets from linear television to digital video. Display advertising at 12.8% serves brand awareness objectives across mobile websites and apps, while Websites at 7.4% and Others at 3.7% capture the remaining market share.

By Industry Vertical

Retail and E-commerce lead at 27.5% through performance marketing demands, mobile commerce growth, and the rise of social shopping experiences requiring persistent mobile advertising presence throughout the consumer purchase journey. The vertical's high mobile advertising intensity reflects the direct sales conversion attribution available through mobile channels, enabling retailers to measure advertising return on investment with sufficient precision to justify substantial ongoing mobile advertising investments across multiple format types.

Media and Entertainment at 18.9% is driven by streaming platform subscriber acquisition campaigns, gaming app advertising, and entertainment brand engagement on social media platforms. BFSI at 13.8% reflects the high CPM financial services category, with banks, insurance companies, and fintech platforms investing heavily in mobile acquisition campaigns. Healthcare at 10.9%, Automotive at 9.2%, Travel and Tourism at 7.6%, Education at 6.5%, and Others at 5.6% represent the remaining market vertical distribution.

Regional Market Insights

|

Region |

Share (2025) |

Key Mobile Advertising Market Drivers & Characteristics |

|

South |

34.8% |

Driven by high concentration of corporate headquarters, robust population growth, and strong retail and e-commerce advertiser investment across Texas, Florida, Georgia, and the Carolinas |

|

West |

29.7% |

Led by technology industry headquarters in California, strong media and entertainment sector advertising investment, and high per-capita mobile advertising spend across Pacific Coast markets |

|

Northeast |

21.5% |

Anchored by advertising agency headquarters in New York City, financial and healthcare mobile advertising investment in Boston, and dense urban smartphone user concentration |

|

Midwest |

14.0% |

Growing through Chicago's diverse corporate advertiser base, automotive industry digital investment in Michigan, and rising mobile internet adoption in secondary metropolitan markets |

The South region, at 34.8%, leads the United States mobile advertising market through its expanding corporate presence, population concentration in high-growth metropolitan areas, and strong retail and e-commerce advertiser base. The West region, at 29.7%, reflects technology industry headquarters concentration in California and the region's disproportionate mobile advertising innovation activity driven by Silicon Valley platforms and the strong media and entertainment economy.

The Northeast, at 21.5%, hosts the largest concentration of advertising agency holding company headquarters in New York City, making it a critical strategy and planning hub even where campaign spend is geographically distributed. The Midwest, at 14.0%, represents the smallest regional share but offers growth opportunities as automotive, financial services, and retail advertisers in Chicago and Detroit expand mobile advertising investments in response to evolving consumer media consumption patterns.

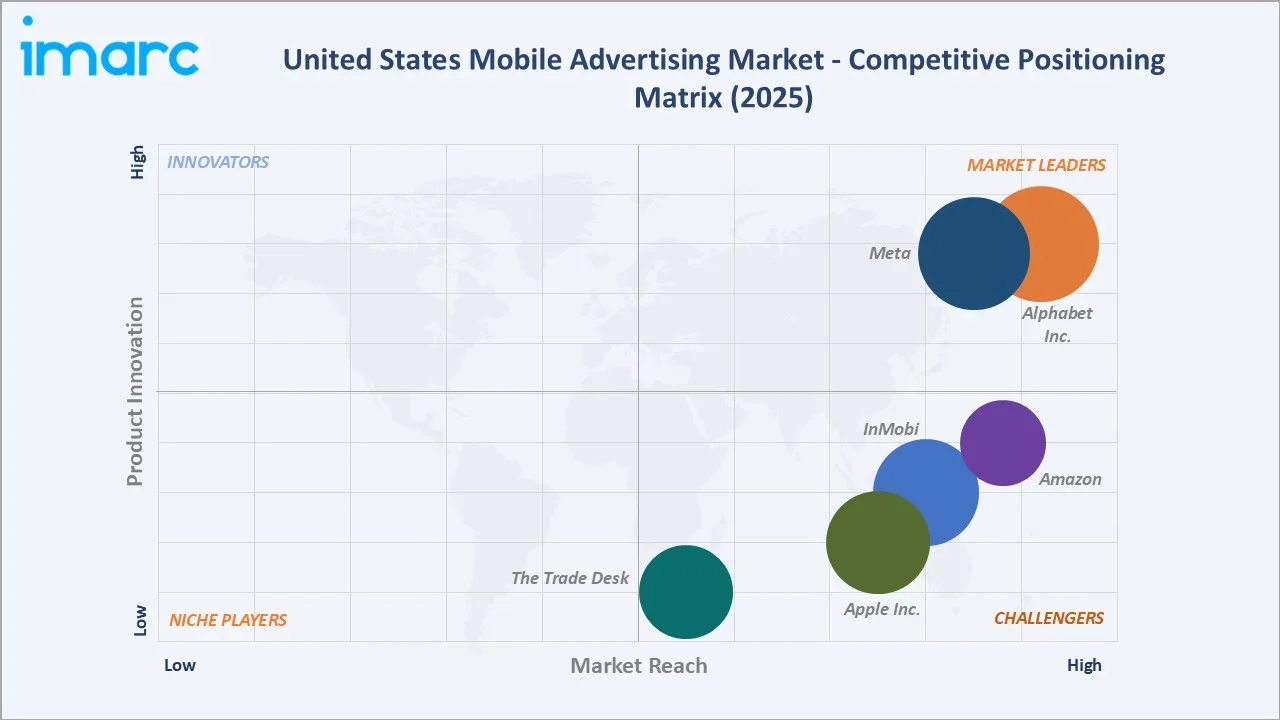

Competitive Landscape

The United States mobile advertising market competitive landscape is highly concentrated at the platform level, with top players collectively commanding approximately 50-60% of total US mobile advertising revenues. The market has three distinct competitive tiers: dominant walled garden platforms controlling first-party data, scaled independent ad technology companies offering programmatic solutions, and specialized mobile advertising solution providers addressing niche formats and audiences.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Alphabet Inc. |

Google Ads, AdMob, DV360, YouTube Mobile Ads |

Market Leader |

Alphabet Inc. (Google) commands the largest US mobile advertising share through dominance in mobile search, YouTube video, and AdMob in-app advertising network. |

|

Meta |

Facebook Ads, Instagram Ads, Advantage+ AI, Meta Audience Network |

Market Leader |

Meta leverages its family of social apps and unmatched first-party social graph data to deliver highly targeted mobile advertising at scale. |

|

Amazon |

Sponsored Products, Amazon DSP, Streaming TV Ads |

Strong Challenger |

Amazon uses unique purchase intent first-party data to enable closed-loop mobile advertising measurement tied directly to e-commerce conversion outcomes. |

|

Apple Inc. |

Apple Ads, Apple Advertising Platform |

Strong Challenger |

Apple Inc. offers premium App Store advertising inventory with high conversion rates, leveraging first-party behavioral data within its privacy-preserving framework. |

|

The Trade Desk |

Trade Desk DSP, Unified ID 2.0, Koa AI |

Market Challenger |

The Trade Desk provides the leading independent programmatic buying platform, enabling open mobile advertising access with advanced AI-powered optimization. |

|

InMobi |

InMobi DSP, Glance, InMobi Exchange |

Market Challenger |

InMobi operates one of the largest independent mobile advertising platforms, offering mobile-specific programmatic solutions and extensive in-app inventory. |

Key players include Alphabet Inc., Meta, Amazon, Apple Inc., The Trade Desk, InMobi, and others.

Key Company Profiles

Alphabet Inc.

Alphabet Inc. is a United States-based technology conglomerate with dominant mobile advertising operations through its Google advertising business, encompassing Google Ads, AdMob, DV360, YouTube, and others, generating the largest mobile advertising revenues in the US market.

- Key Products: Google Ads, AdMob, DV360, YouTube Mobile Ads

- Strategic Focus: Advancing AI-first advertising solutions through Performance Max automation, developing Privacy Sandbox for Android as a privacy-compliant mobile targeting alternative, and expanding YouTube Shorts advertising monetization to capture short-form video budgets migrating from TikTok.

Meta

Meta is a United States-based social technology company operating Facebook, Instagram, WhatsApp, and others, with mobile advertising constituting over 95% of total advertising revenues, making it one of the largest US mobile advertising platform.

- Key Products: Facebook Ads, Instagram Ads, Advantage+ AI, Meta Audience Network

- Strategic Focus: Scaling AI-powered advertising automation through Advantage+ to improve advertiser return on ad spend, expanding Instagram Reels and Threads advertising monetization, and developing Conversions API infrastructure as a privacy-preserving alternative to pixel-based mobile attribution for performance measurement across the US market.

Amazon

Amazon is the advertising division of Amazon.com Inc., a United States-based e-commerce and cloud computing company, offering sponsored advertising, display advertising, and programmatic solutions leveraging Amazon's unique first-party purchase intent data at scale across its retail and media ecosystem.

- Key Products: Sponsored Products, Amazon DSP, Streaming TV Ads

- Strategic Focus: Expanding retail media network capabilities for third-party retailers to grow the addressable advertising ecosystem beyond Amazon's own inventory, scaling Amazon Marketing Cloud clean room technology for privacy-preserving audience measurement and growing Streaming TV advertising inventory on Prime Video to capture television budgets transitioning to digital.

Market Concentration Analysis

The US mobile advertising market is highly concentrated at the platform level, with the top two players collectively accounting for approximately 50-60% of total mobile advertising revenues. Amazon Advertising has emerged as the third-largest platform, capturing an estimated 10-12% share through retail media network expansion and sponsored advertising growth.

Independent ad technology companies collectively address the remaining open programmatic and niche advertising market segments. Market concentration is evolving as retail media networks and connected TV advertising create new competitive dynamics, redistributing advertising budgets away from traditional search and social formats toward performance-measurable commerce media channels.

Investment & Growth Opportunities

Highest Growth Segments

Video advertising (~16.2% CAGR), Social Media advertising (~14.8% CAGR), Retail and E-commerce vertical (~14.1% CAGR), AR/VR mobile ad formats (~30%+ CAGR from nascent base), AI-powered campaign automation tools (~20% CAGR), and privacy-tech mobile identity solutions represent the highest-growth investment vectors through 2034 in the US mobile advertising market.

Emerging Investment Opportunities

Retail media network technology platforms enabling brands to access first-party purchase intent data through mobile advertising represent the US mobile advertising market's highest-value emerging investment opportunity. Connected TV and streaming advertising technology enabling mobile-CTV cross-screen campaigns represents a significant additional investment opportunity as linear television advertising budgets migrate to addressable digital formats over the forecast period.

Investment Themes

- Privacy-Preserving Mobile Identity Infrastructure: Companies developing cookieless mobile targeting solutions, universal identity graphs, and clean room technologies for mobile advertising represent structural long-term investment opportunities as third-party mobile identifier deprecation reshapes the US mobile targeting ecosystem through 2034, creating durable competitive advantages for platforms establishing privacy-compliant audience solutions before regulatory constraints intensify further.

- AI Generative Creative Automation for Mobile Advertising: Investment in AI-powered mobile creative production platforms automating personalized ad generation at scale represents a significant market opportunity, reducing creative production costs while improving campaign performance through continuous optimization, with particular value for mid-market advertisers lacking resources to produce creative volumes needed to compete effectively in algorithmic auction environments throughout the forecast period.

Future Market Outlook (2026-2034)

The United States mobile advertising market is projected to grow from USD 78.5 Billion in 2025 and is estimated to reach USD 88.72 Billion in 2026. It is further projected to attain USD 245.0 Billion by 2034, delivering a 13.09% CAGR over the forecast period. Three structural forces define this growth trajectory with high confidence across macroeconomic scenarios.

Mobile devices will consolidate their position as the primary advertising channel as US consumers spend increasing proportions of media time on mobile screens across social media, streaming video, gaming, and mobile commerce applications. AI-powered advertising automation will expand the addressable advertiser base by reducing expertise and budget barriers to effective mobile advertising, growing total market participation from smaller advertisers who previously lacked resources to run sophisticated mobile campaigns.

The market anchor value of USD 145.1 Billion in 2030 represents the midpoint trajectory where AI automation has become mainstream across all major platforms, privacy-preserving identity solutions have stabilized targeting capabilities following the post-cookie transition, and short-form video advertising has established its position as the premium mobile advertising format commanding the highest CPMs in the US digital advertising market.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50 or more industry stakeholders conducted in 2025, including Chief Marketing Officers, programmatic advertising platform leads, mobile marketing specialists, retail media network managers, mobile measurement and attribution specialists, ad agency media buyers, and brand-side mobile advertising decision-makers across key industry verticals including retail, financial services, and healthcare.

Secondary Research

Secondary research encompassed company annual reports and investor presentations, IAB Internet Advertising Revenue Reports, eMarketer US digital advertising forecasts, Mobile Marketing Association industry benchmarks, FTC privacy regulation guidance, Apple ATT impact analyses, Sensor Tower app market data, and mobile advertising market forecast studies from leading research firms. Over 60 secondary sources were reviewed and cross-referenced to triangulate market size estimates and segment share assumptions.

Forecasting Models

Market revenue forecasts were developed using a top-down digital advertising share model calibrated against IAB US digital advertising baseline data, with mobile's share projected forward using mobile consumption time share growth rates and mobile CPM inflation trends derived from platform-reported revenue disclosures and agency media buying allocation surveys collected through primary research activities.

United States Mobile Advertising Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Format Types Covered | Search, Display, Video, Social Media, Websites, Others |

| Industry Verticals Covered | Retail and E-commerce, Media and Entertainment, Healthcare, BFSI, Education, Travel and Tourism, Automotive, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Alphabet Inc., Meta, Amazon, Apple Inc., The Trade Desk, InMobi, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States mobile advertising market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States mobile advertising market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States mobile advertising industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Mobile Advertising Market Report

The United States mobile advertising market size is estimated at USD 88.72 Billion in 2026, driven by Social Media advertising at 31.8%, Search advertising at 24.6%, and Video advertising at 19.7% of format type share. Retail and E-commerce leads industry verticals at 27.5%, and the South region commands 34.8% of the national market.

The market grows at 13.09% CAGR during 2026-2034, reaching USD 245.0 Billion by 2034. This growth reflects continued smartphone adoption, AI-powered advertising automation, social commerce growth, retail media network expansion, and 5G-enabled rich media advertising format innovation.

Social Media leads at 31.8% in 2025, driven by Meta's Facebook and Instagram platforms, TikTok's advertising revenue growth, and Snapchat's engaged young demographic. Social media advertising's superior first-party audience targeting capabilities maintain its dominant position through the forecast period.

Retail and E-commerce lead at 27.5% through performance marketing requirements, mobile commerce growth, social shopping integration, and the availability of closed-loop mobile attribution enabling retailers to measure direct advertising return on investment with sufficient precision to justify ongoing substantial investment.

The South leads at 34.8% through major corporate headquarters concentration, robust population growth, and high digital advertising investment in key metropolitan areas, including Dallas, Atlanta, Miami, and Charlotte. The South's economic growth trajectory supports continued advertising investment expansion through the forecast period.

Leading companies include Alphabet Inc., Meta, Amazon, Apple Inc., The Trade Desk, InMobi, and others.

The United States mobile advertising market is projected to reach USD 145.1 Billion by 2030, with AI advertising automation achieving mainstream adoption, privacy-preserving identity solutions stabilizing mobile targeting capabilities following the post-cookie transition, and short-form video establishing dominance as the premium mobile advertising format.

Three priority investment opportunities include privacy-preserving mobile identity infrastructure development, AI-powered generative creative automation platforms for mobile advertising workflows, and retail media network technology enabling brands to access first-party purchase data through mobile advertising channels at major US retailers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade