Key Challenges and Opportunities Shaping the Japan Power Electronics Industry

Introduction to the Japan Power Electronics Market:

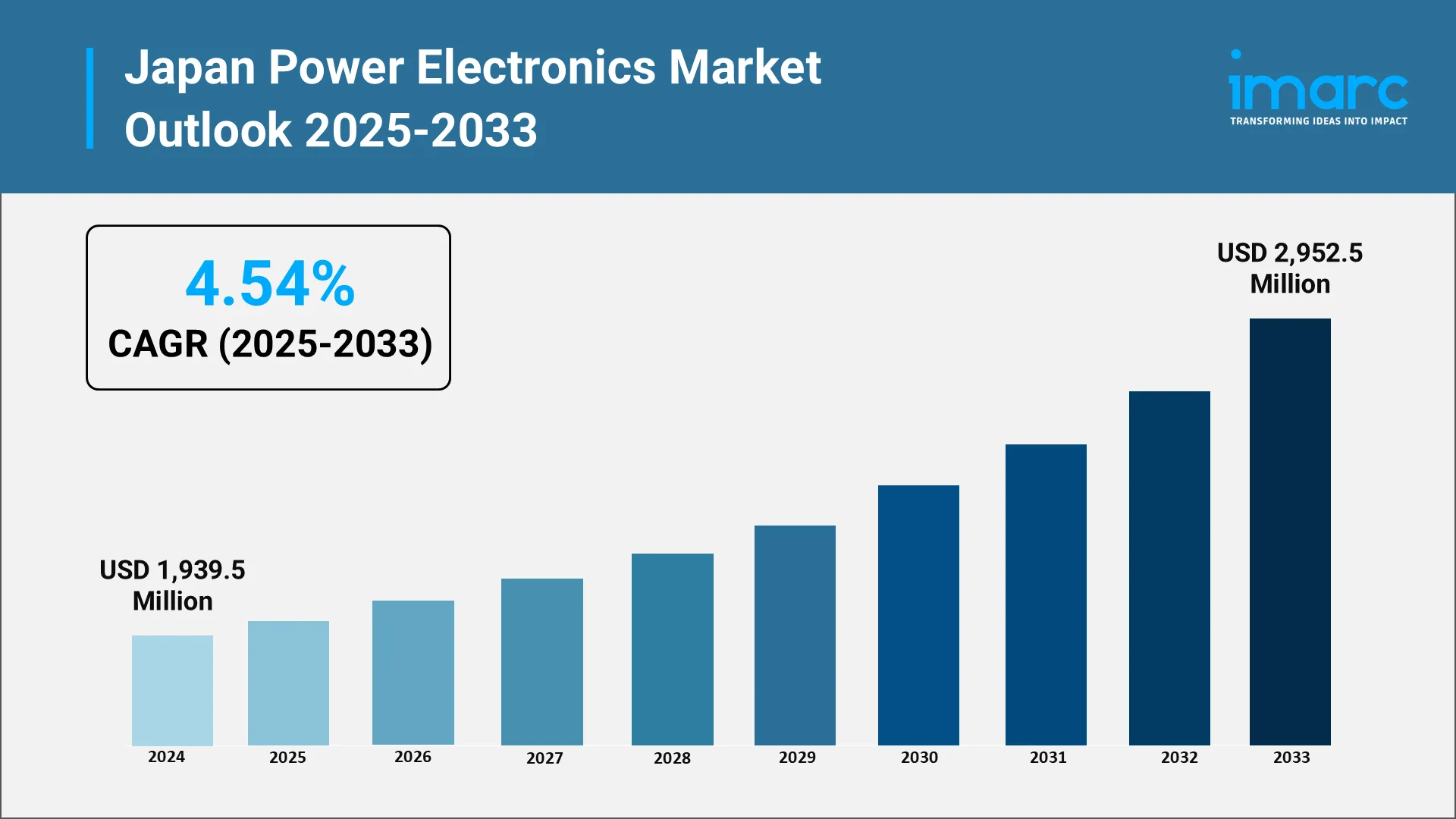

The Japan power electronics market is poised to grow substantially, driven by rising demand in automotive, energy, industrial automation, and infrastructure sectors. According to IMARC Group, the Japan power electronics market is studied from 2019 to 2024 with projections extending to 2033.

Power electronics — covering devices such as inverters, converters, power modules, discrete switches, and integrated power ICs — serve as essential building blocks for energy conversion, regulation, and control. Japan’s unique mix of domestic demand (highly automated factories, advanced transport) and national commitments to decarbonization create both challenge and opportunity for players in this domain.

Explore in-depth findings for this market, Request Sample

Rising Demand Across Automotive and Industrial Applications

- Automotive Electrification Driving Growth

The shift toward electric vehicles (EVs) is reshaping the power electronics landscape worldwide. Japan’s automotive industry—home to major OEMs and tier-1 suppliers—is pushing aggressively into electrification. Power inverters, DC–DC converters, onboard chargers (OBCs), and battery management systems (BMS) all depend heavily on advanced power electronics.

Globally, the power electronics market is forecast to grow from a revenue of about USD 32.96 Billion in 2024 to USD 52.38 Billion by 2033. Japanese firms are well positioned to capture parts of that growth, given their existing expertise in automotive electronics and reliability demands. Domestic automakers and suppliers increasingly demand components with higher efficiency, lower losses, smaller footprints, and greater thermal robustness.

- Industrial Automation, Robotics, and Process Electrification

Japan is a leader in robotics, factory automation, semiconductor manufacturing, precision equipment, and high-end industrial machinery. All of these systems increasingly depend on power conversion, motor drives, variable frequency drives (VFDs), and real-time power control. The global power electronics trends highlight that industrial motor drives remain a major volume driver.

In semiconductor fabs or data centers, power electronics must manage high current densities, maintain low electromagnetic interference, and handle fast switching. Japan’s strengths in precision manufacturing, thermal design, and reliability give it an edge—but only if innovation keeps pace.

- Infrastructure & Grid Edge Demand

Japan has also begun integrating power electronics deeply into grid infrastructure, such as static VAR compensators, grid-tied inverters for renewable plants, and energy storage interface systems. As Japan liberalizes its electricity market and opens new grid services, demand for advanced converters, grid controllers, and power conditioning systems will follow.

Technological Advancements and Innovation in Power Devices:

- Wide Bandgap Semiconductors (SiC, GaN) as Enablers

One of the strongest trends is a shift from silicon-based devices (IGBTs, MOSFETs) to wide bandgap (WBG) materials such as silicon carbide (SiC) and gallium nitride (GaN). WBG devices offer lower conduction and switching losses, higher temperature operation, and greater switching speeds. Japan’s research institutions, semiconductor firms, and device fabs are investing in these areas.

- Advanced Packaging, Thermal and Reliability Engineering

As switching speeds rise, thermal management and packaging become bottlenecks. Japan’s semiconductor and materials firms are exploring advanced packaging techniques (e.g. chip-scale packaging, substrate materials, 3D interconnect) and cooling methods (liquid cooling, heat pipes, novel substrates) to keep performance stable over long life cycles. The challenge is to design packaging that maintains reliability under harsh temperature cycling, vibration, and long-term drift.

- Integration and System-Level Intelligence

Pure device innovation is no longer enough: system integration, smart sensing, and control loops are becoming differentiators. Embedding real-time diagnostics, adaptive switching control, and predictive maintenance (e.g. self-healing, fault detection) into power modules is gaining traction. Japanese firms can leverage strength in sensor integration, AI, and control.

- Materials, Nanotechnology, and Alternative Substrates

Beyond SiC/GaN, Japan’s materials science base is exploring novel materials, substrates, and dielectric compounds to reduce parasitic inductance, improve breakdown voltage, and reduce device footprint. Research in wide bandgap alloys, ultra-low loss dielectrics, and next-gen packaging materials matters more as demands scale.

Government Policies and Energy Efficiency Regulations:

- National Targets: GX, Decarbonization, Strategic Energy Plans

In February 2025, Japan approved the Seventh Strategic Energy Plan. It aligns with a national goal to reduce greenhouse gas emissions by about 73 % by FY2040 (versus FY2013). The plan supports stable energy supply, economic growth, and decarbonization via policies dubbed “GX” (Green Transformation).

Under GX, Japan is pushing investments in renewables, hydrogen, energy storage, and energy efficiency. Power electronics is at the heart of many of these solutions.

- Energy Efficiency Legislation & Benchmarking

The cornerstone policy is the Act on the Rational Use of Energy, known informally as Japan’s energy conservation law, first passed in 1979. This is supplemented by programs like the Top Runner program (which enforces efficiency standards on appliances and devices) and industrial benchmarking measures.

METI (Ministry of Economy, Trade and Industry) continually revises energy efficiency standards for transformers, inverters, and other power equipment. Utilities and manufacturing facilities (especially large energy users) must file periodic reports and adhere to benchmarking targets.

- Incentives, Subsidies, and Regulation

To spur green transformation, incentives, grants, and subsidies are provided for renewable deployment, storage, smart grid trials, and energy-efficient equipment. JETRO notes that FIT (feed-in tariffs), FIP (feed-in premiums), and local government programs help support renewable and storage rollouts. On the regulation front, utilities are being deregulated, retail markets liberalized, and grid access rules reformed.

The stricter efficiency standards and regulation push OEMs and power electronics firms to meet tighter loss targets, higher reliability, and lower parasitic values. These requirements escalate R&D and capital burden, especially for smaller players.

.webp)

Key Challenges: High Costs and Supply Chain Constraints

- High Manufacturing and Material Costs

Wide bandgap devices, advanced substrates, and premium packaging technologies come with high initial costs, and yields are often low in early fabrication. Many Japanese firms must contend with capital-intensive fabs, expensive materials, and small margins in the early phases of adoption.

Cost competition from foreign players—especially from China, South Korea, and Taiwan—is intense. Maintaining performance leadership while managing cost pressure is a delicate balance.

- Supply Chain Disruptions and Rare Materials

Input dependencies are a serious threat. For instance, SiC wafers, GaN epitaxy, specialized substrates, hermetic packaging materials, rare metals, and precision ceramics may depend on limited global supply or critical material imports. Global supply chain shocks (pandemic, geopolitical friction, shipping delays) can upend procurement. The power electronics industry globally is reinforcing resilience across supply chains.

- Thermal, Packaging, and Reliability Bottlenecks

As switching speeds and power densities rise, thermal and packaging constraints become harder to overcome. Aging, reliability under harsh environments, and field failures can damage reputation and market trust. The margin for error narrows.

- Fragmentation and Regulatory Complexity

Domestic regulation, energy efficiency norms, import/export controls, safety certifications (e.g. for automotive), and grid interconnection standards vary by region or utility. Navigating this regulatory patchwork increases cost and time. In addition, companies often must localize designs to meet Japanese quality and safety standards, which can slow time-to-market.

- Market Saturation and Intense Competition

The Japan electronics ecosystem is crowded. Established firms like Toshiba, Mitsubishi Electric, Hitachi Power Semiconductor Device already compete heavily. New entrants must differentiate technologically or via cost-efficiency. Rapid innovation cycles and short product life spans demand continuous investment.

Additionally, some domestic demand is met by imports due to lower production costs abroad. Competing with low-cost foreign components while maintaining Japanese reliability standards is a constant struggle.

Emerging Opportunities in Renewable Energy and Smart Grids:

- Grid-Tied Inverters, Energy Storage, Microgrids

Japan plans to dramatically expand renewable capacity. To integrate intermittent wind and solar generation, advanced power electronics will be needed: grid-tied inverters, power conditioning units, control systems, battery interface, bidirectional converters, and microgrid controllers.

Energy storage systems (ESS) combined with renewables demand efficient converters and charge/discharge controllers. As costs decline, the pairing of solar-plus-storage becomes economically viable and presents scale opportunities.

- Smart Grid, Demand Response, and Power Electronics as Grid Asset

Japan’s power market liberalization (with full retail liberalization since 2016 and T&D unbundling as of 2020) opens doors for grid services, demand response, and distributed energy integration. In this regime, power electronics can act as active grid assets — supporting voltage regulation, frequency stability, reactive power control, and grid resilience.

Japan also plans to increase electricity output by 35–50 % by 2050 to meet demands from AI, chip fabs, and data centers. That means large-scale infrastructure, more renewables, and higher stress on grid edge electronics.

- Electrification Beyond EVs: Marine, Rail, Aviation

Power electronics opportunities extend beyond cars. Rail systems, electric ferries, aircraft auxiliary systems, and electric buses all call for high-efficiency converters and power modules. Japan’s transport ambitions and decarbonization goals position these segments for growth.

- Export Potential and Global Partnerships

Japan’s leadership in quality, miniaturization, reliability, and materials research gives it export advantage. Collaboration with foreign OEMs, joint ventures, and cross-border acquisitions can help Japanese firms tap into global EV and renewable markets. A partner strategy combining Japanese quality and global scale could be compelling.

- Innovation in Grid-Edge Electrification, Solid-State Transformers

Research interest in solid-state transformers, bidirectional power flow, and real-time reconfigurable grids opens a pathway for cutting-edge device makers in Japan to lead. Integration with AI for grid optimization, vehicle-to-grid (V2G) support, and predictive energy load management is a potential differentiator.

Choose IMARC Group as your trusted partner in the power electronics sector:

- Data-Driven Market Research: Deepen your understanding of device trends, adoption rates in automotive, industrial electrification, and renewable power systems through rigorous, custom research reports.

- Strategic Growth Forecasting: Predict emerging shifts — from SiC/GaN device uptake to grid-scale inverter deployment and smart grid architectures — across geographies.

- Competitive Benchmarking: Compare product pipelines, techno-roadmaps, and reliability performance of leading power electronics players in Japan and globally.

- Policy and Infrastructure Advisory: Stay ahead of evolving Japanese energy regulations, efficiency mandates, grid liberalization, and subsidy regimes in the power and energy sectors.

- Custom Reports and Consulting: Get bespoke insights aligned with your goals — whether entering Japan’s power electronics space, investing in device manufacturing, or scaling system integration.

At IMARC Group, we aim to empower decision-makers in the electronics and energy industries with clarity, foresight, and actionable intelligence. Partner with us to navigate the evolving power electronics landscape by clicking on the link: https://www.imarcgroup.com/japan-power-electronics-market

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

Japan's printed circuit board (PCB) industry is the world leader in technology innovation, enabling consumer electronics, automotive, and next-generation communication system development. As a key enabler of modern electronic products, PCBs provide the essential building blocks for embedding semiconductors, sensors, and microchips into miniaturized, high-performance devices. Japan, through its world-class manufacturing base and engineering expertise, remains the hub of the global PCB supply chain.

Aluminum-Air (Al-Air) battery is a new energy storage technology that has attracted interest as a future alternative to conventional lithium-ion batteries, specifically for electric vehicle (EV) use. As opposed to normal rechargeable batteries, the Al-Air battery is a metal-air electrochemical cell with aluminum as the anode, oxygen from the ambient air as the cathode reactant, and a liquid electrolyte (commonly sodium hydroxide or potassium hydroxide) as the medium through which the reaction occurs.

Aluminium wire is an essential industrial commodity commonly employed in power transmission, electrical distribution, building construction, and manufacturing processes owing to its high conductivity-to-weight ratio, resistance to corrosion, and cost advantage over copper. Produced by methods including continuous casting, rolling, and drawing, aluminum wire is available in various grades and alloys to serve the wide demands, from overhead transmission conductors and building wiring to automotive harnesses and electronic applications.

Air conditioners are electromechanical devices used to control indoor climate by extracting heat and humidity and ensuring optimum air circulation. Generally consisting of a compressor, condenser, evaporator, refrigerant fluid, filters, fans, and electronic controls, air conditioners work based on the principle of heat exchange, moving heat from indoor areas to the external environment. Contemporary units come in diverse configurations, such as split systems, window units, central air systems, and portable models, supporting respective residential, commercial, and industrial applications. Some of the major characteristics are efficiency in cooling, energy use, noise rating, and environmental footprint in relation to refrigerant type.

E-waste, or electronic waste, is electrical and electronic equipment that has been discarded, such as computers, cell phones, television sets, servers, and household appliances. It is among the world's fastest-growing streams of waste, consisting of a heterogeneous combination of metals, plastics, glass, and toxic substances. E-waste contains valuable metals like copper, aluminum, gold, silver, palladium, and rare earth elements, in addition to toxic materials like lead, mercury, cadmium, and brominated flame retardants.

Polished silicon wafers are very pure, ultra-flat semiconductor substrates that are produced from high-quality single-crystal silicon. The wafers act as the material base for making integrated circuits, power devices, and MEMS (Microelectromechanical Systems). The wafers are made of monocrystalline silicon ingots using the Czochralski or Float-Zone process, from which the wafers are cut, lapped, etched, and polished to atomic-scale flatness and defect-free surfaces.

AI is revolutionizing Japan’s semiconductor industry by boosting innovation and efficiency across the entire value chain. Advanced artificial intelligence (AI)-powered Electronic Design Automation (EDA) tools significantly shorten chip design cycles, improving performance and energy efficiency.

Recent projections indicate that Australia semiconductor market, including services, is growing at a steady compound annual growth rate as the nation deepens its tech infrastructure. The importance of semiconductors spans electronics, defense systems, telecommunications, and emerging AI applications, which position the local ecosystem as strategically vital for growth.

Fiber optic cables are high-tech communications cables that carry information like bursts of light along extremely thin glass or plastic strands, providing high-speed, high-bandwidth connectivity with little loss of signal. Fiber optic cables make up the foundation of contemporary telecommunications, carrying internet, cloud computing, 5G networks, and smart infrastructure.

CAT (Category) cables are twisted-pair Ethernet cables utilized for copper-based wired network communications, varying from CAT5e to CAT8 standards. The cables carry data through copper conductors, but with different speeds (up to 40 Gbps for CAT8) and bandwidths, supporting networks such as LANs, data centers, and smart buildings.

India's semiconductor industry is undergoing a revolutionary phase driven by rising demand from industries like consumer electronics, automotive technologies, industrial automation, and telecom infrastructure.

USB data cables are critical elements of contemporary digital connectivity, enabling high-speed and consistent data transfer and power supply for a broad scope of electronic products. They provide the foundation for charging and synchronizing smartphones, tablets, laptops, and other peripherals, with significant applications in consumer electronics, industrial automation, and new technologies. With technologies like USB-C, the cables today carry faster data speeds, more power output, and universal compatibility, making them essential in a world that is connected.

Thin-film-transistor (TFT) liquid-crystal display (LCD) is a type of display technology used in many electronic devices, such as smartphones, tablets, laptops, and televisions (TVs). A backlight, colour filters, a thin-film transistor array, and a liquid crystal layer are among the layers that make up this flat-panel display. TFT LCDs are made to produce sharp images with superb viewing angles, strong contrast, and accurate colour reproduction. They are made up of thousands of tiny transistors that regulate how much light enters each pixel. This makes it possible for the display to generate crisp, detailed images at rapid refresh rates. TFT LCD technology's low power consumption is one of its main benefits, which makes it perfect for battery-operated gadgets.

Polycrystalline solar photovoltaic (PV) modules are a key component of solar energy systems, harnessing sunlight and converting it into electricity through the photovoltaic effect. These modules are composed of multiple interconnected solar cells, each made from polycrystalline silicon. Polycrystalline solar panels are renowned for their efficiency, affordability, and versatility, making them a popular choice for various applications such as solar installations, commercial and industrial projects, off-grid systems and solar farms.

The LED chip is the core component of an LED bulb, comprising semiconductor layers that enable the free flow of protons and electrons. Employed in all LED lighting fixtures—from bulbs to tubes—the LED chip fundamentally determines light quality, with variations in brightness, voltage, and wavelength. These chips are manufactured through a process called MOCVD (metal-organic chemical vapor deposition), which creates the semiconductor layers that facilitate electric flow. Major applications of these chips include backlighting, illumination, automotive lighting, signs, and signals.

Semiconductors are crucial components in the modern electronics industry, used in electronic equipment and devices to manage and control the flow of electricity. They are found in consumer items like smartphones, wearables, smart TVs, and advanced equipment used in industrial applications, defense, and aerospace. Semiconductors are further divided into four broad categories: optoelectronics, discrete components, integrated circuits, and sensors. Memory devices, logic devices, analog ICs, MPUs, discrete power devices, MCUs, and sensors are some of the major components of semiconductors.