Australia Private Equity Industry: Tech Investments Surge, Major Sectors, Leading Firms, and Insights

Introduction:

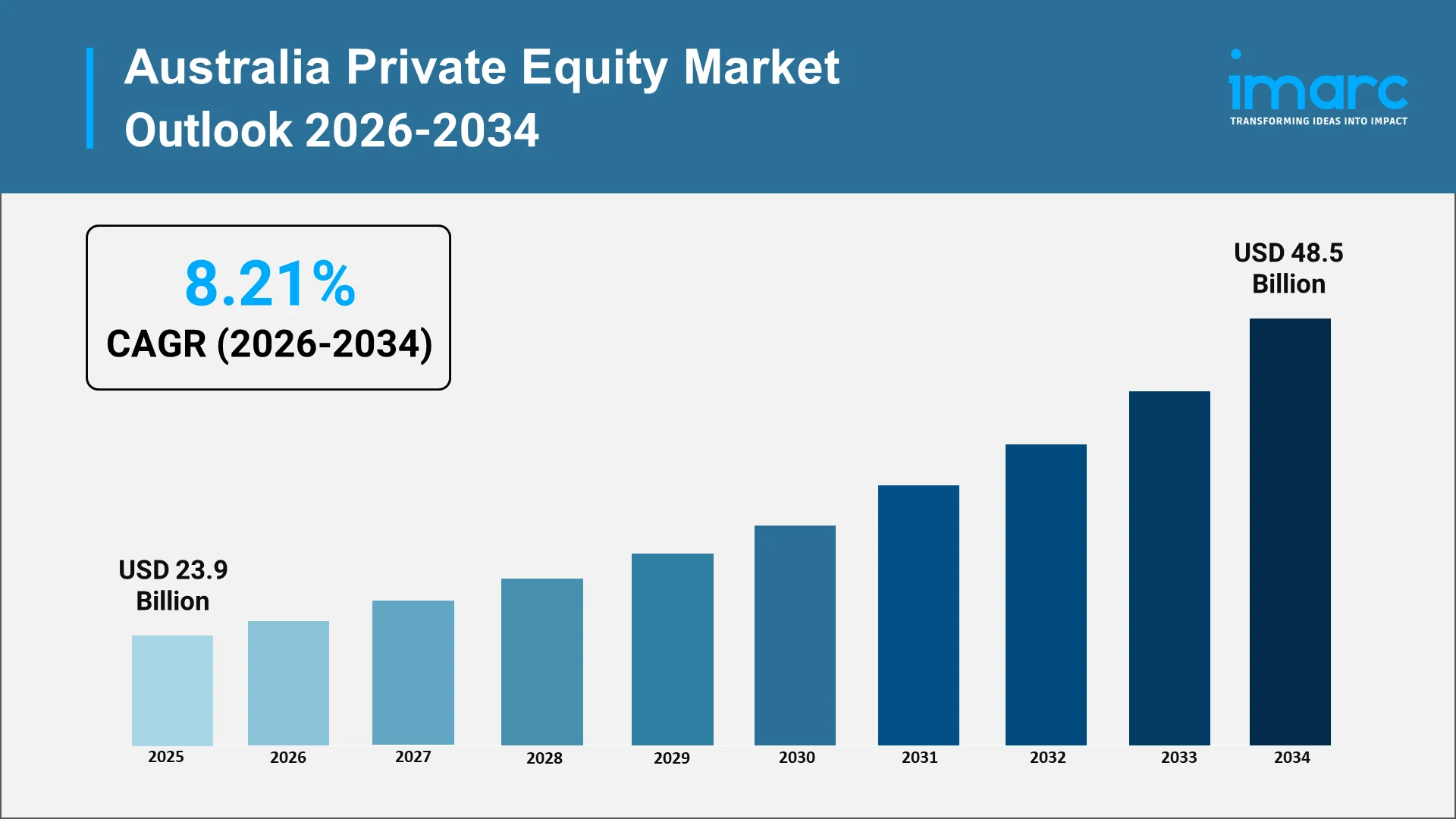

The Australia private equity industry is experiencing transformative growth as institutional investors increasingly allocate capital to high-potential sectors, including technology, healthcare, and renewable energy. The Australia private equity market size reached USD 23.9 Billion in 2025 and is projected to surge to USD 48.5 Billion by 2034, exhibiting a robust compound annual growth rate (CAGR) of 8.21% during 2026-2034. This remarkable expansion reflects the market's evolution from traditional leveraged buyouts to sophisticated investment strategies powered by artificial intelligence, advanced analytics, and digital transformation initiatives.

As global private equity firms expand their presence in Australia, the competitive landscape has intensified across multiple dimensions. International players are attracted by Australia's stable regulatory environment, strong superannuation system managing approximately AUD 3.9 Trillion, and strategic positioning within the Asia-Pacific region. With assets under management reaching AUD 66 billion as of June 2023, representing 2.6% of GDP, the Australian private equity ecosystem has matured into a dynamic marketplace where innovation, operational excellence, and value creation drive investment decisions. The integration of artificial intelligence across deal sourcing, due diligence, and portfolio management represents a fundamental shift in how private equity firms identify opportunities and generate returns for investors.

Explore in-depth findings for this market, Request Sample

The Role of AI in Deal Sourcing, Valuation & Portfolio Management:

Artificial intelligence is revolutionizing the Australia private equity landscape by fundamentally transforming traditional investment methodologies. Recent surveys indicate that most private equity and venture capital firms have now integrated artificial intelligence into their operations, reflecting its evolution from an emerging innovation to a core component of decision-making and investment management processes.

In deal sourcing, AI-powered platforms analyze over 45,000 potential investment targets across Australian markets, processing financial statements, market data, and competitive intelligence 60% faster than traditional methods. According to the industry reports, 65% of private equity executives are either piloting or fully implementing AI in investment decision-making, citing improved deal sourcing efficiency as the top benefit. Industry estimates suggest that AI has the potential to boost deal origination productivity by as much as 30%, allowing partners and analysts to dedicate more time to strategic negotiations instead of routine data-gathering tasks.

Natural language processing (NLP) algorithms have emerged as powerful tools for identifying hidden opportunities. These systems sift through unstructured data—including news articles, press releases, regulatory filings, and social media posts—to identify companies or sectors gaining momentum before competitors discover them. AI-driven platforms aggregate data from multiple sources, including government databases, patent filings, hiring trends, and even satellite imagery, presenting a holistic view of investment opportunities that would be impossible to compile manually.

For valuation and due diligence, AI transforms what has historically been a time-consuming bottleneck in deal timelines. Advanced AI tools can ingest thousands of documents—financial reports, customer contracts, compliance records—and automatically highlight irregularities such as sudden revenue spikes, inconsistent margin reporting, or unusually favorable contract clauses. Research indicates that private equity firms integrating AI into their deal sourcing processes are achieving notable improvements in lead quality and reductions in acquisition costs. Many firms also expect significant declines in the cost of pursuing or terminating deals over the coming years, driven by enhanced efficiency and automation within the due diligence process.

Portfolio management has been similarly transformed by AI capabilities. Real-time AI-powered dashboards offer continuous visibility into the performance metrics of portfolio companies, enabling private equity teams to identify issues early and act quickly to resolve them. Machine learning models analyze historical financial statements, cash flows, and industry data to identify early signs of financial distress or credit risk, allowing proactive intervention before problems escalate. Advanced analytics platforms enhance investment evaluation, enabling private equity firms to assess portfolio companies more accurately and identify value creation opportunities through data-driven insights.

AI’s transformative potential in deal sourcing is evident in its ability to analyze vast volumes of market data and identify promising opportunities far faster than traditional methods. This unprecedented efficiency enables both mid-market and large private equity firms to sustain stronger deal pipelines while channeling greater focus toward strategic decision-making and relationship management.

Impact & Benefits: Faster Due Diligence and Smarter Exits

The integration of artificial intelligence and advanced analytics into private equity operations delivers measurable impacts across the entire investment lifecycle, from initial screening through successful exits. Faster due diligence represents one of the most immediate and quantifiable benefits. Traditional due diligence processes often required weeks or months to thoroughly evaluate potential acquisitions, creating competitive disadvantages in fast-moving markets. AI-driven document processing solutions now analyze thousands of pages in minutes, extracting key data points and identifying patterns that would take analysts days to uncover manually.

Optical Character Recognition (OCR) technology converts scanned documents, contracts, and financial statements into searchable and editable formats, enabling rapid information retrieval. Retrieval-Augmented Generation (RAG) combines the power of large language models with custom data from internal business documents, delivering accurate and contextually relevant responses grounded in high-quality sources. This approach supports dynamic analysis, making AI tools more reliable for tasks like due diligence and market research while ensuring outputs can be easily verified against source materials.

The Australia private equity market is experiencing fundamental shifts through technology-driven deal sourcing, with AI and software proliferation continuing to garner attention from private equity funds, particularly in professional services and financial sectors. Healthcare AI investments are creating significant opportunities, with global healthcare technology attracting substantial private equity interest as aging demographics and digital transformation converge.

Smarter exits represent the culmination of AI-enhanced portfolio management strategies. By continuously monitoring market conditions, competitor activities, and macroeconomic indicators, AI systems can identify optimal exit windows that maximize returns for investors. Predictive analytics models forecast asset performance with increasing precision, helping private equity firms time exits to capture peak valuations. According to the Reserve Bank of Australia's April 2024 bulletin, the share of capital committed to Australian private equity funds from foreign investors rose steadily to 45% in 2019, compared with less than 10% in 2010, demonstrating growing international confidence in the market's sophistication and potential returns.

Exit strategies in Australia’s private equity market are becoming more diverse, extending beyond traditional IPOs to include secondary transactions, strategic sales, and partial divestments. With public markets remaining relatively subdued, firms are increasingly favoring alternative exit routes that offer greater flexibility and certainty. Secondary transactions and strategic sales have emerged as the preferred options, reflecting the industry’s adaptability and focus on achieving optimal outcomes in a challenging market environment.

The technology sector remains a leading source of private equity deal activity in Australia, largely driven by venture capital interest. However, despite its prominence in deal volume, larger investment values are increasingly concentrated in sectors such as infrastructure, real estate, and industry, where AI-enabled operational efficiencies offer stronger potential for long-term returns. This trend highlights a shift in focus from high-growth tech startups to asset-heavy sectors capable of leveraging technology for performance optimization and value creation.

Opportunities & Challenges: Regulation, Risk, and Competitive Edge

The Australia private equity market presents compelling opportunities alongside evolving regulatory complexities that firms must navigate strategically. Government infrastructure initiatives are creating substantial investment prospects through public-private partnerships, with the Australian Government committing AUD 22.7 billion as part of its 'Future Made in Australia' policy announced in the 2024-2025 budget. This federal initiative seeks to protect Australia's long-term national interest by investing in domestic capability to provide economic resilience, security, and independence.

Infrastructure and renewable energy sectors offer particularly attractive growth trajectories. In March 2025, I Squared Capital announced that Rest superannuation fund—one of Australia's largest profit-to-member superannuation funds managing approximately USD 59.52 billion for 2 million members—committed USD 300 million to global infrastructure investments, focusing specifically on digital infrastructure, transportation, and renewable energy sectors. This demonstrates strong institutional backing for infrastructure-focused private equity strategies.

The healthcare technology sector represents another significant opportunity driven by Australia's aging population demographics and increasing digitalization of medical services. Private equity firms are capitalizing on the convergence of healthcare delivery and technology platforms, investing in telemedicine solutions, digital health records, and AI-powered diagnostic tools that improve patient outcomes while reducing system costs.

However, regulatory challenges have intensified in 2024-2025, fundamentally altering the competitive landscape for private equity transactions. The Australian Parliament passed the Treasury Laws Amendment (Mergers and Acquisitions Reform) Act 2024 on November 28, 2024, introducing mandatory merger control notification requirements effective January 1, 2026, with transitional voluntary notification available from July 1, 2025. This represents the most significant change to Australia's merger regime since the Trade Practices Act was enacted 50 years ago, according to ACCC Chair Gina Cass-Gottlieb.

Under the revised regulatory framework, transactions involving a change of control—whether through the acquisition of shares, assets, or interests in partnerships and investment schemes—must now be notified to the Australian Competition and Consumer Commission (ACCC) for approval before completion if they meet specific monetary thresholds. The ACCC has signaled increased scrutiny of private equity activity, particularly in the case of serial acquisitions and roll-up strategies. Sectors such as liquor, pathology, and private healthcare services are receiving heightened regulatory attention as part of this more proactive oversight approach.

The updated regulatory framework introduces a structured two-phase review process for merger assessments. Initial reviews are designed for quicker determinations, while more complex cases undergo extended evaluation if potential competition concerns are identified. The framework also introduces standardized filing fees, with certain exemptions available for smaller businesses, ensuring a more transparent and proportionate approach to regulatory oversight.

Foreign investment regulations have also tightened, with the Foreign Investment Review Board (FIRB) announcing on May 1, 2024, a revised risk-based approach that applies special scrutiny to investments in critical infrastructure, critical minerals, critical technology, investments in proximity to sensitive government facilities, and investments involving holding or accessing sensitive data sets. Rising geopolitical tensions have contributed to greater scrutiny of foreign investment into Australia, potentially extending approval timelines for international private equity firms.

Competitive pressures in the Australian private equity market are escalating as increasing amounts of capital pursue a limited pool of quality assets. Firms are responding by adopting more selective and disciplined investment strategies, focusing on opportunities that offer clear value creation potential. Despite a shift toward smaller deal sizes, large-scale transactions continue to take place globally, particularly in take-private and carve-out deals, reflecting sustained investor confidence in strategic, high-value opportunities.

Cost of capital challenges persisted through 2024, with headline inflation in Australia remaining among the highest in major advanced economies due to tight labor markets, higher energy prices, sustained migration, and cost-of-living increases. Markets expected the first rate cut to occur in 2025, contrasting with other advanced economies like Singapore and the UK that had already initiated rate cuts. The elevated cost of debt in Australia presented challenges for private equity buyers accustomed to historically low interest rates.

.webp)

Recent News: Mega Funds, Tech Buyouts & New PE Regulations

The Australia private equity landscape witnessed several landmark transactions and regulatory developments during 2024-2025 that signal the market's continued maturation and global significance.

Mega Fund Deals:

Blackstone completed the largest data center deal globally and Australia's biggest transaction of 2024 with its AUD 24 billion acquisition of AirTrunk in December 2024. The transaction, which received regulatory approval from the Australian Foreign Investment Review Board, involved a consortium led by Blackstone, including Blackstone Real Estate Partners, Blackstone Infrastructure Partners, Blackstone Tactical Opportunities, and Blackstone's private equity strategy for individual investors, alongside the Canada Pension Plan Investment Board (CPP Investments). AirTrunk, founded in 2016, operates hyperscale data centers across Australia, Hong Kong, Japan, Malaysia, and Singapore, with over 800MW of capacity committed to customers. This acquisition represents Blackstone's largest-ever investment in the Asia-Pacific region, surpassing its AUD 8.9 billion takeover of Crown Resorts in 2022.

According to Blackstone President and Chief Operating Officer Jon Gray, "This is Blackstone at its best, leveraging our global platform to capitalize on our highest conviction theme. AirTrunk is another vital step as Blackstone seeks to be the leading digital infrastructure investor in the world across the ecosystem, including data centers, power and related services." The deal underscores the unprecedented demand for digital infrastructure driven by artificial intelligence adoption and broader economic digitization.

International Fund Launches:

Ares Management Corporation, a leading global alternative investment manager, launched the Ares Private Markets Fund (AUT) on December 11, 2024, an Australian-domiciled unit trust designed to provide wholesale clients in Australia access to the Ares Private Markets Fund (APMF), a U.S.-registered management investment vehicle. APMF, managed by Ares' Wealth Management Solutions platform, is a private equity investment solution that primarily invests in North American and European private equity fund stakes, offering Australian investors diversified exposure to international private markets.

Regulatory Developments:

Beyond the mandatory merger control regime previously discussed, the Australian Government released draft notification forms in March 2025 requiring merger parties to specify whether Sale and Purchase Agreements contain goodwill protection provisions, including non-competes and restraints of trade. The ACCC issued transition guidance indicating that businesses considering acquisitions in 2025 should engage as early as possible to ensure sufficient time for review completion before the mandatory regime takes effect. The ACCC also announced it will renew and expand its Performance Consultative Committee to advise on merger review functions, consisting of stakeholders, including consumer, business, and legal representatives.

Technology Investment Trends:

According to the Australian Private Capital 2025 Yearbook, technology continues to account for the highest proportion of private equity-backed deals by number, with the sector attracting significant venture capital interest. However, average deal sizes in technology decreased compared to mega-deals in infrastructure and real estate, suggesting a bifurcation between early-stage technology investments and large-scale infrastructure acquisitions. The IT sector's share of total private equity deployment by value remains at approximately 8%, with larger capital commitments flowing to infrastructure, real estate, and industrial opportunities.

The private equity market in Australia is also witnessing increased mid-market focus, with firms pursuing operational transformation strategies and Environmental, Social, and Governance (ESG) integration becoming standard practice rather than optional considerations. Superannuation funds are boosting allocations to private equity, with foreign capital contributing approximately 45% of capital committed to Australian-focused funds, demonstrating continued international investor confidence despite regulatory complexities.

Conclusion:

The Australia private equity market stands at a pivotal transformation point, driven by unprecedented superannuation fund backing, record-high assets under management, and strategic technology adoption across investment lifecycles. The integration of artificial intelligence represents a fundamental competitive advantage, with 82% of private equity firms actively deploying AI tools to accelerate deal sourcing, enhance due diligence accuracy, and optimize portfolio management decisions.

The regulatory landscape is evolving rapidly, with mandatory merger control requirements effective from January 2026, introducing new compliance obligations but also providing greater certainty for long-term strategic planning. While these changes present short-term adjustment challenges, they ultimately strengthen market integrity and investor confidence. Foreign investment scrutiny has intensified around critical infrastructure and technology sectors, reflecting Australia's strategic positioning within broader Asia-Pacific geopolitical dynamics.

Technology investments continue to surge across the Australia private equity market size expansion, particularly in digital infrastructure, fintech platforms, healthcare technology, and renewable energy solutions. The landmark AUD 24 Billion Blackstone-AirTrunk transaction exemplifies the scale of capital available for high-conviction digital infrastructure opportunities. Leading firms, including Blackstone, KKR, Carlyle Group, Bain Capital, Pacific Equity Partners, BGH Capital, and Quadrant Private Equity, are leveraging sophisticated analytics, operational expertise, and global networks to capture emerging opportunities across diverse sectors.

Looking forward, the Australian private equity ecosystem will continue to evolve through innovation, regulatory adaptation, and strategic capital deployment. Firms that successfully integrate artificial intelligence capabilities, navigate complex regulatory requirements, and maintain disciplined investment approaches will be best positioned to generate superior risk-adjusted returns for investors. The convergence of strong institutional backing, technological transformation, and strategic government infrastructure initiatives creates a robust foundation for sustained growth throughout the remainder of the decade.

Choose IMARC Group As We Offer Unmatched Expertise and Core Services:

- Data-Driven Market Research: Deepen your knowledge of private equity deal flows, investment scenarios, and technological advancements such as AI-driven analytics, digital infrastructure platforms, and ESG integration frameworks through comprehensive market research reports tailored to Australia's dynamic investment environment.

- Strategic Growth Forecasting: Predict emerging trends in private equity deployment—from intelligent data centers and AI-powered portfolio management tools to regulatory changes, merger control requirements, and institutional allocation shifts—analyzed by sector, deal size, and geographic region across Australia.

- Competitive Benchmarking: Analyze competitive forces shaping Australia's private equity market, review fund strategies and performance metrics, and monitor breakthroughs in operational value creation, technology adoption, and alternative exit strategies employed by leading domestic and international firms.

- Policy and Infrastructure Advisory: Stay ahead of evolving regulatory paradigms including ACCC merger control requirements, FIRB foreign investment protocols, and government-sponsored infrastructure programs affecting deal structuring, approval timelines, and investment opportunity assessment.

- Custom Reports and Consulting: Access tailored insights aligned with your organizational objectives—whether evaluating sector-specific investment opportunities, assessing competitive positioning, analyzing regulatory compliance requirements, or developing comprehensive market entry strategies for Australia's private equity ecosystem.

At IMARC Group, our goal is to empower private equity professionals, institutional investors, and strategic advisors with the clarity and intelligence required to navigate Australia's complex investment landscape. Partner with us to unlock transformational opportunities—because every investment decision matters.

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

The global maritime sector operates as the backbone of international trade, facilitating the movement of the world’s goods by volume. Within this vast and complex ecosystem, the marine insurance market plays an indispensable role by providing financial protection against risks inherent to maritime operations. From hull and machinery coverage to cargo, liability, and protection and indemnity (P&I) insurance, marine insurance safeguards the assets, revenues, and reputation of shipowners, cargo operators, and logistics companies.

The Australian travel insurance market has grown from a value-added travel product to a necessary protection for travelers. As confidence in domestic and foreign travel increases, Australian travelers increasing value full coverage against unexpected events like medical issues, flight cancellations, and trip interruptions.

Australia’s wealth management industry is undergoing a profound transformation, driven by rapid technological advancements, evolving investor behavior, and the increasing integration of artificial intelligence (AI) in financial services. The nation’s strong economic fundamentals, coupled with its expanding base of high-net-worth individuals (HNWIs) and robust superannuation system, have established a solid foundation for sustained market growth.

The Australia investment banking industry is experiencing transformative growth driven by technological innovation, sustainable finance initiatives, and robust mergers and acquisitions activity. With market valuations reaching USD 7.9 Billion in 2024, the sector demonstrates remarkable resilience despite global economic uncertainties.

The Australian fintech industry stands as one of the most dynamic and rapidly expanding financial technology ecosystems in the Asia-Pacific region. The market reached USD 4.10 Billion in 2024 and is projected to surge to USD 9.50 Billion by 2033, representing a compound annual growth rate (CAGR) of 8.90%. This remarkable trajectory positions Australia as a global fintech powerhouse, with around 767 companies operating across major capital cities including Sydney, Melbourne, and Brisbane.

Australia’s equity market is leaning into artificial intelligence as a practical lever for returns, liquidity, and product innovation. By size, the Australia stock market reached USD 72.9 Million in 2024 and is projected to hit USD 114.4 Million by 2033 at a 5.13% CAGR (2025–2033). Those headline figures sit on top of an economy where listed companies already deploy AI in operations, compliance, and customer-facing tools, while market plumbing: data centers, cloud, and connectivity, ramps for GPU-heavy workloads.

The Australian cryptocurrency market is experiencing significant growth, with the rise of digital assets capturing both public and institutional interest. Driven by technological innovation, evolving regulations, and increasing institutional adoption, the Australia cryptocurrency exchange market was valued at USD 975.76 Million in 2024, stated by the IMARC Group.

India’s real estate market is entering a new phase of structured growth, driven by a powerful confluence of factors. The real estate market size in India was valued at approximately USD 482 Billion in 2024, is being reshaped by robust residential demand, the expansion of commercial spaces, and increasing institutional investment.

In a progressively interconnected world, where digital operations form the backbone of commerce and daily life, the specter of cyber threats is no longer rare – it is becoming a daily headline. From phishing scams to full-blown ransomware assaults, cyber threats are evolving faster than most businesses can react.

India’s foreign exchange market has emerged as a crucial component of the nation's financial system. Over the past decade, its scale, depth, and liquidity have expanded significantly, fueled by increasing international trade volume, attracting foreign investments (FDI and FII), and facilitating outbound remittances.

India's real estate market is rapidly transforming, driven by urbanization, economic growth, and evolving consumer preferences. Real estate is no longer limited to residential and commercial properties; it is shaping infrastructure, technology-driven housing, and sustainable developments. With increasing investments, policy reforms, and rising demand for smart and affordable housing, the sector is witnessing significant expansion.

Real estate represents tangible property encompassing land and any enhancements, whether natural or artificial, affixed to it. It can serve various purposes, including residential, commercial, agricultural, and industrial. Ownership of real estate can belong to a government, a corporate entity, or a private party. The value of real estate is often influenced by factors such as location, demand, economic conditions, and market trends. Real estate markets can vary significantly from one region to another, with factors like population growth, urbanization, and infrastructure development playing crucial roles in shaping these markets.

The combustion of fossil fuels results in the release of a substantial amount of greenhouse gases, mainly carbon dioxide. Carbon dioxide emissions occur directly or indirectly from individuals, organizations, events, or products. A carbon footprint measures the environmental impact in terms of carbon emissions. Governments and organizations worldwide are engaged in various initiatives to reduce carbon emissions. In 1992, the United Nations Framework Convention on Climate Change (UNFCCC) introduced the "Kyoto Protocol," an international agreement aimed at significantly reducing greenhouse gas emissions. Adopted in Kyoto, Japan, on December 11, 1997, it became international law on February 16, 2005. Under the Kyoto Protocol, countries were allocated a maximum number of carbon credits. If a country exceeded its assigned limit, penalties in the form of a reduced emissions cap for the subsequent period were imposed.