Top Factors Driving Growth in the GCC Construction Market

Introduction to the GCC Construction Industry:

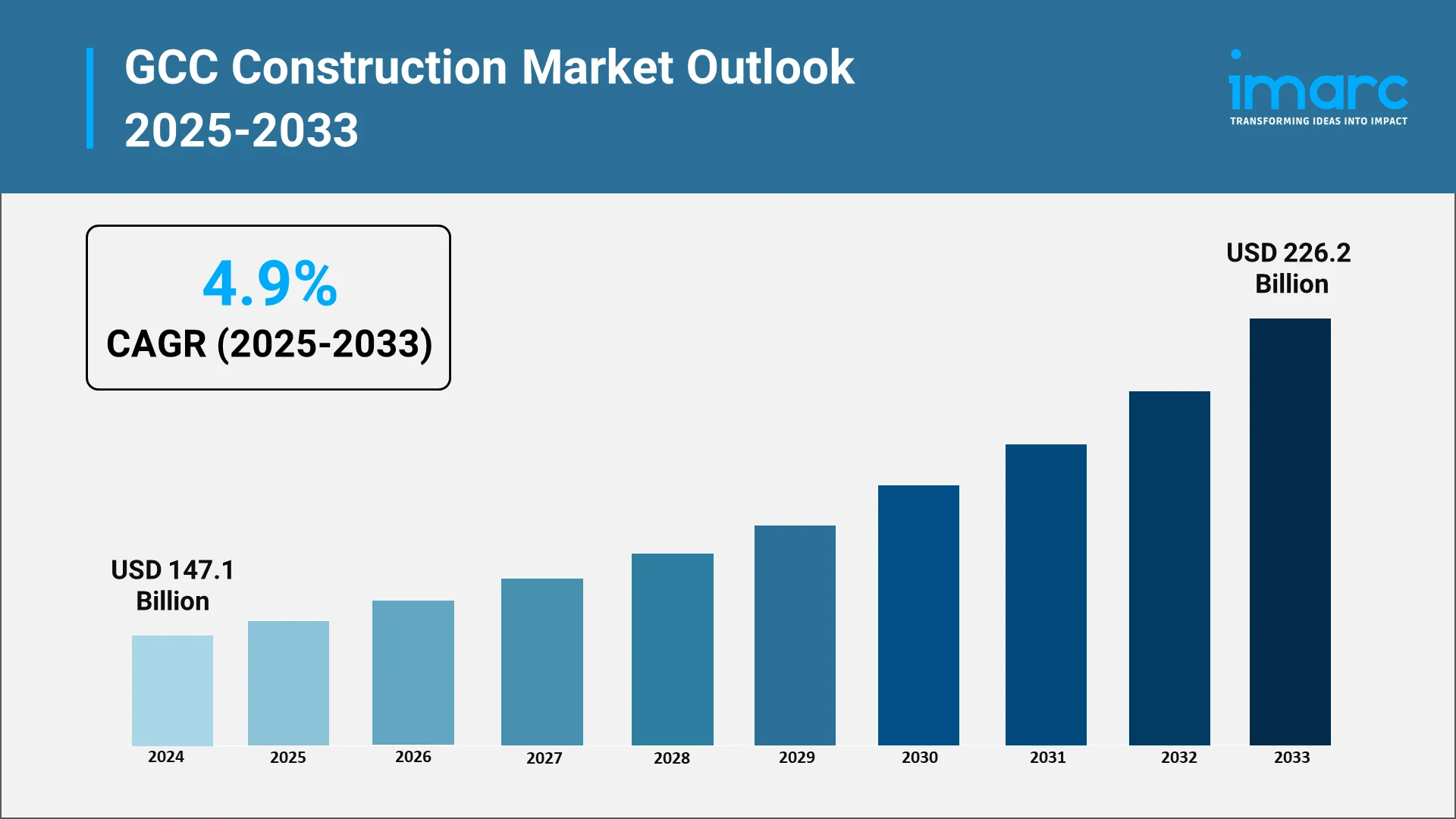

The construction industry across the Gulf Cooperation Council (GCC) member states is at the core of a monumental economic transformation. Far exceeding traditional building activities, the sector now serves as the principal vehicle for national economic diversification strategies, moving these nations beyond reliance on oil revenues. In 2024, the GCC construction market size reached USD 147.1 Billion. The ambitious visions set forth by regional governments—aiming to build futuristic, sustainable, and globally competitive societies—have infused the market with unprecedented momentum. This drive is characterized by large-scale, complex development programs that require massive investment in infrastructure, urban amenities, and high-tech solutions. The resulting expansion affects every part of the regional economy, creating a vibrant landscape of opportunities for domestic and international firms. The sustained and strategic nature of this development trajectory provides a crucial indicator of the fundamental GCC construction market size, which continues to expand rapidly to support the region’s long-term aspirations.

Explore in-depth findings for this market, Request Sample

Rising Investments in Mega Infrastructure and Urban Development Projects:

The single most influential factor propelling the GCC market is the aggressive investment in giga-projects and comprehensive urban masterplans. These developments are designed not merely as construction projects, but as foundational economic pillars intended to attract tourism, global trade, and foreign direct investment. From the creation of entirely new, purpose-built cities to the establishment of vast, high-capacity transport networks—including advanced rail systems, expanded ports, and modernized airports—the focus is on dramatically improving global connectivity and quality of life. This massive pipeline of strategic work demonstrates governmental commitment to reshaping the physical and economic identity of the Gulf region. The execution of these schemes necessitates collaboration between local and global heavyweights, directly impacting the distribution of work across the region and thereby defining the GCC construction market share among the leading industry players. The sustained governmental support ensures that the project momentum remains strong, insulating the sector from many external pressures and guaranteeing a steady flow of contracts for years to come.

Increasing Adoption of Sustainable and Green Building Materials:

Sustainability has emerged as a non-negotiable standard within the GCC construction sphere, evolving rapidly from a desirable feature to a core regulatory requirement. Driven by national climate pledges and the need for more resource-efficient urban environments, there is a widespread pivot toward green building practices. Governments are implementing mandatory green building codes that enforce higher performance standards for energy and water conservation, air quality, and material selection. This focus stimulates demand for innovative, eco-friendly construction materials, such as low-emission concrete, advanced insulation systems, and recycled content. This dedication to responsible development is reshaping supply chains and project specifications across all sectors. The increasing integration of environmental, social, and governance factors into procurement and design criteria is one of the most significant GCC construction industry trends 2024, showcasing a long-term commitment to ecological stewardship. Developers who prioritize sustainable design and lifecycle cost efficiency are gaining a distinct competitive advantage, pushing the entire industry toward a greener and more mature operational model.

Growth in Public-Private Partnership (PPP) Construction Initiatives:

The growing reliance on Public-Private Partnership (PPP) models is a strategic financial and operational shift designed to manage the scale and complexity of the region's development goals. PPPs enable governments to leverage the specialized expertise, efficiency, and private capital of the corporate sector, accelerating the delivery of critical public infrastructure and social amenities. By sharing project risks and responsibilities, this funding model allows large-scale, long-duration projects—such as transportation, utilities, and social facilities—to move forward more reliably and quickly. The framework encourages private entities to focus not just on the initial build, but also on the long-term maintenance and operational excellence of the asset. This structured approach to financing and project delivery is a critical component for any thorough GCC construction market analysis, as it indicates where new opportunities for private participation and investment will arise. The growing acceptance and successful execution of PPP projects across the Gulf signal a sophisticated evolution in project governance and procurement, fostering deeper collaboration between the public and private realms.

Expanding Construction Technology Integration (BIM, Drones, and 3D Printing):

The GCC construction sector is actively undergoing a digital transformation, adopting advanced technologies to boost productivity and manage complexity inherent in giga-projects. Building Information Modeling (BIM) is now widely mandated, serving as a unified digital platform that optimizes design coordination, clash detection, and asset management throughout the project lifecycle. On-site efficiency is being revolutionized by tools like drones, which provide real-time aerial surveying, site progress monitoring, and enhanced safety surveillance. As per Middle East Property and Construction Handbook- MENA economic review 2025, Artificial intelligence (AI)-supported construction approaches, such as generative designs, supply chain management predictive analytics, and improved safety monitoring, are becoming increasingly important in the construction industry. This shows an effort to overcome the industry's historical digitization lag. Furthermore, the region is emerging as a global leader in piloting and scaling up advanced fabrication methods. The adoption of modular construction and large-scale 3D printing accelerates delivery timelines, reduces waste, and addresses labor demands by shifting production off-site. These technological investments are often highlighted in specialized GCC construction market reports to illustrate the market’s commitment to innovation and its move towards industrialized construction. Embracing digital tools and automation is essential for meeting aggressive national development timelines and ensuring that the quality and precision of the final built environment are world-class.

Surge in Residential and Commercial Real Estate Developments across GCC:

Underpinning the large-scale infrastructure work is a continuous and substantial demand for residential and commercial real estate. Rapid urbanization, significant population expansion—including a growing influx of skilled expatriates—and a rising quality of life expectation are fueling this sector. Developers are actively catering to varied consumer segments, launching everything from master-planned, mid-market residential communities to highly luxurious and iconic urban towers. The commercial segment is thriving due to the growth of new business hubs, economic free zones, and a burgeoning tourism and hospitality industry, which requires massive new retail, office, and leisure facilities. This private and consumer-driven demand provides essential diversification and resilience to the overall market. The strong pipeline of housing and commercial projects remains a key indicator for any optimistic GCC construction market forecast, ensuring sustained activity for contractors focused on building and property development. The continuous creation of vibrant mixed-use developments further solidifies the region’s status as a dynamic global center for living and commerce.

Opportunities and Challenges in the GCC Construction Industry:

The GCC construction landscape presents a compelling balance of high-reward opportunities and structural challenges. Navigating these factors is critical for successful market entry and sustained performance. The latest GCC construction industry trends last 6 months emphasize that resilience and adaptability are crucial for firms operating in this fast-paced environment.

Opportunities:

- Decade-Long Project Pipeline: Guaranteed workload across multiple sectors (transport, tourism, utilities) due to strategic national visions.

- Green Building Specialization: High demand for expertise in sustainable materials, energy efficiency retrofits, and smart building technologies.

- Digital Adoption Services: Strong opportunities for firms specializing in BIM implementation, construction software, and automation solutions.

- Localized Manufacturing: Incentives for establishing regional supply chains to reduce reliance on imports and improve cost predictability.

Challenges:

- Skilled Labor Shortages: Persistent difficulty in sourcing and retaining a specialized, highly skilled workforce.

- Supply Chain Volatility: Vulnerability to global material price fluctuations and delays, impacting project budgets and timelines.

- Cash Flow Management: Complex payment structures and delays, requiring robust financial planning and risk mitigation strategies.

- Regulatory Adaptation: Need to continuously adjust to evolving national building codes, sustainability mandates, and localization policies.

.webp)

Future Outlook for the GCC Construction Industry:

The outlook for the GCC construction industry is defined by ambitious scale, strategic intent, and technological advancement. The market is transitioning into a mature, high-tech sector where sustainability and digitalization are standard operating procedure, not optional extras. Continued, targeted government investment, coupled with the proven effectiveness of PPP frameworks, will ensure a stable foundation for growth. The sustained demand from urbanization and the tourism boom guarantees that both infrastructure and building construction will remain buoyant. The commitment to futuristic projects ensures that the GCC construction market size 2024 will continue to reflect robust expansion, driven by visionary leadership and the necessary capital to realize these monumental national aspirations. Looking forward, IMARC Group expects the market to reach USD 226.2 Billion by 2033, exhibiting a growth rate (CAGR) of 4.9% during 2025-2033.

Choose IMARC Group for Unmatched Expertise in the GCC Construction Market:

To successfully capitalize on the expansive opportunities and navigate the unique complexities of the Gulf construction sector, access to deep, authoritative market intelligence is non-negotiable.

- Data-Driven Market Research: Deepen your knowledge of infrastructural investment plans, project pipelines, and the specialized demand for advanced construction materials and services through in-depth market research reports tailored to the region.

- Strategic Growth Forecasting: Predict emerging trends in project financing, procurement models (like PPP), and technological adoption (BIM, modular construction) by region and sector, enabling you to strategically position your firm for future growth.

- Competitive Benchmarking: Analyze competitive forces within the Gulf, review contractor project histories, and monitor breakthroughs in sustainable building practices and large-scale project execution methodologies.

- Policy and Infrastructure Advisory: Stay one step ahead of regulatory paradigms, localization programs, and foreign investment policies affecting project bidding, labor quotas, and operational standards across the GCC.

- Custom Reports and Consulting: Get tailored insights geared to your organizational objectives—be it entering a new GCC country, investing in specialized construction technology, or building strategic local partnerships for giga-projects.

At IMARC Group, our goal is to empower industry leaders with the clarity and intelligence required to secure and execute successful projects in the world’s most exciting construction market. Join us in shaping the future skyline of the Gulf—because every structure matters. Please visit: https://www.imarcgroup.com/gcc-construction-market, for more details.

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

Paver blocks are precast construction material made basically from cement, aggregates, sand, and pigments for constructing surfacing. They are produced in standardized shape and thickness, allowing each unit to interlock to form a strong, load-bearing surface with no need for continuous concrete pouring. Paver blocks possess high compressive strength, abrasion resistance, and are easy to lay and maintain.

The Brazil ceramic tiles market has witnessed stable growth, reflecting broader trends in the construction and building materials industries of the country. The Brazil ceramic tiles market size was valued at USD 1.6 Billion in 2025. The market is expected to reach USD 2.2 Billion by 2034, exhibiting a CAGR of 3.91% during 2026-2034.

MDF is an engineered wood product produced by breaking down hardwood or softwood residuals into wood fibers, which are then combined with resin binders under heat and pressure. MDF exhibits a homogeneous density, a smooth surface, and fine texture, ensuring a much more workable material compared to natural wood.

Float glass is a type of flat glass that is manufactured by floating molten glass on a bed of molten tin. This produces a smooth, uniform surface and consistent thickness. The float process was developed by Pilkington in the 1950s and revolutionized glassmaking because it enabled the production of large, flawless sheets of glass without needing polishing or grinding. The basic raw materials used-silica sand, soda ash, limestone, and dolomite-are heated in the furnace to a very high temperature, then continuously poured onto the tin bath, where the molten glass spreads out into an even layer. It cools and solidifies into a perfectly flat and perfectly transparent sheet. As it provides optical clarity and strength and is easily processed into coated, laminated, or toughened forms, float glass is used as a basic product for various applications, ranging from architectural and automotive to industrial applications.

ERW steel pipes can be identified as one of the most important categories of welded pipes and find wide applications in infrastructure, construction, and other industries because of their precision, cost-effectiveness, and reliability. The raw material to produce these pipes is either hot-rolled or cold-rolled steel coils that are longitudinally formed and welded by the application of high-frequency electric resistance welding.

Drill bits are specifically designed cutting instruments intended to produce cylindrical holes in various materials, ranging from soft woods and plastics to hardened steels, stone, and rock. Although they seem straightforward, drill bits consist of various specialized shapes, coatings, and materials that are designed to suit the cutting characteristics of the intended material and the requirements of the drilling task.

Concrete is among the most widely used construction materials in the world due to its strength, versatility, and durability. It is a composite material largely made of cement, water, aggregates-sand, gravel, or crushed stone-and in some cases, admixtures which give special properties to the concrete.

Clay bricks are one of the oldest and most extensively used construction materials in the globe, appreciated for their strength, durability, insulation against heat, and beauty. They are produced mainly from natural clay and shale, which are fashioned, dried, and subjected to high-temperature firing to produce a hard, dense material that can resist multiple environmental and structural stresses. The mix generally consists of alumina, silica, lime, iron oxide, and magnesia that collectively decide the color, texture, and performance properties of the brick.

Metal beam crash barriers and high mast light poles are essential infrastructural features providing security and visibility on highways, city roads, and industrial sites. Metal beam crash barriers or guardrails are made of galvanized steel beams, typically W-beam or Thrie-beam, that are designed to dissipate the impact energy on impact with a vehicle and minimize death and damage to vehicles.

Laminated plywood is an engineered wood material that is produced by laminating several layers of thin veneers of wood together with powerful adhesives and covering them with a protective or decorative laminate sheet. This amalgamation not only increases the strength of the plywood but also its beauty, which is why it is extremely versatile for use in furniture, cabinetry, floors, paneling, and interior design.

Ductile iron pipes (DIP) are a key part of new water and wastewater infrastructure, providing enhanced performance capabilities over older piping materials. Cast from ductile cast iron, a material that has the strength of steel combined with the resistance to corrosion of cast iron, these pipes are designed to endure high-pressure use while still being flexible enough to absorb stress without cracking.

The real estate sector plays a critical role in driving economic growth and shaping communities. It significantly contributes to national economies by generating jobs, influencing investment flows, and boosting government revenues through taxes. Beyond these economic benefits, real estate development directly affects the quality of life by creating homes, enhancing infrastructure, and revitalizing urban areas.

Gypsum boards, also referred to as drywall or plasterboard, are lightweight, strong and fireproof building materials that are frequently used for partitions, walls and ceilings. Constructed from a gypsum core encased in paper liners, they provide improved acoustics, cost effectiveness, and speedy installation. Gypsum boards are favoured in industrial, commercial, and residential construction because of its environmentally beneficial qualities, ability to withstand moisture, and ability to insulate against heat. They are an essential part of efficient and sustainable construction methods because of their adaptability to contemporary building processes.

A frameless shower door is a modern and aesthetically appealing bathroom fixture that has gained popularity for its sleek and minimalist design. They are constructed without the bulky metal framing that surrounds the glass panels and are typically made from thick, tempered glass that is securely attached to the wall and floor using hinges or brackets.