Top Petrochemical Segments Driving Global Market Growth

Market Overview: The State of Petrochemicals in 2025

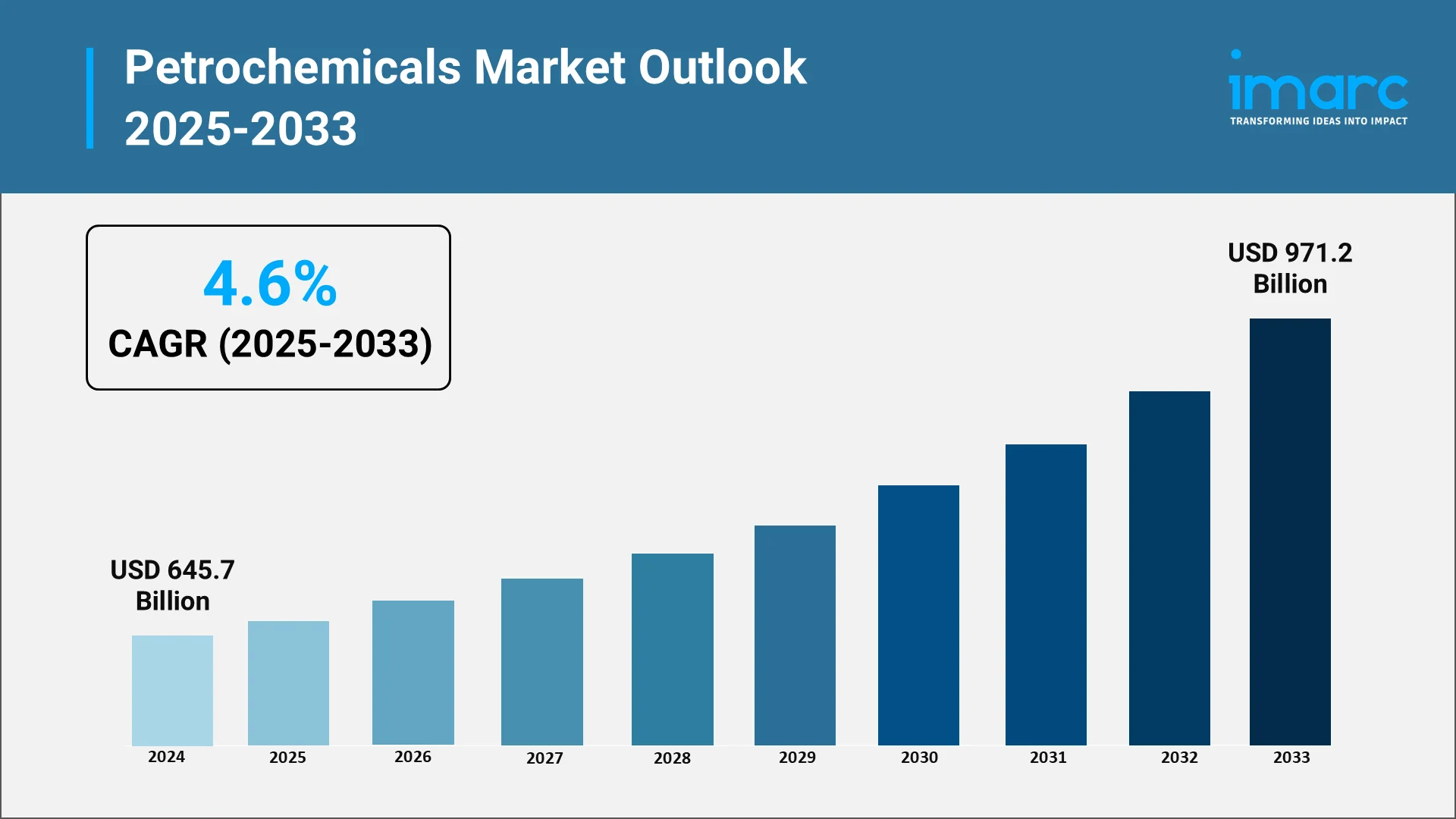

The global petrochemicals market is witnessing steady growth, supported by rising end-user consumption, industrial diversification, and infrastructure development across both developed and emerging economies. As industries increasingly adopt lighter and high-performance materials, demand for synthetic polymers, specialty chemicals, and plastics derived from petrochemicals continues to expand. As per IMARC projections, the global petrochemicals market reached USD 645.7 Billion in 2024 and is expected to reach USD 971.2 Billion by 2033, reflecting a CAGR of 4.6% during 2025-2033.

In parallel, governments and manufacturers are investing in domestic production to reduce import dependency and enhance export capabilities. Regulatory mandates on emissions and plastic waste are accelerating the transition toward cleaner technologies and bio-based feedstocks. This article provides a detailed examination of the top segments driving growth in the petrochemical industry.

Explore in-depth findings for this market, Request Sample

Top Growth-Driving Segments:

The petrochemical market in 2025 is shaped by rising demand across several key product categories, each playing a central role in industrial supply chains. Among these, ethylene, propylene, aromatics, methanol, and bio-based derivatives continue to demonstrate significant growth due to their diverse applications and alignment with global industrial and sustainability goals.

1. Ethylene and Its Derivatives

Ethylene remains a fundamental building block in the petrochemical industry. Its primary derivative, polyethylene (PE), is the most widely used plastic globally, applied in sectors such as food packaging, medical disposables, industrial films, and household products. In 2025, high-density polyethylene (HDPE) and linear low-density polyethylene (LLDPE) are witnessing strong demand.

Ethylene oxide is widely used in producing surfactants, detergents, and antifreeze solutions. In November 2024, Argus launched a global weekly Ethylene Oxide and Derivatives service, providing price assessments, capacity analysis, and trade insights to support strategic decisions across the ethylene value chain. Capacity expansions in China, India, the United States, and the Middle East are underway to meet global demand. These new facilities are increasingly integrating energy-efficient technologies and carbon capture systems to align with environmental compliance expectations.

2. Propylene and Polypropylene

Propylene is the second-most significant olefin in the global petrochemical market. Its major derivative, polypropylene (PP), is essential in automotive components, medical tools, consumer goods, and textile fibers. In March 2025, LyondellBasell approved a propylene expansion project at its Channelview Complex in Houston, adding 400,000 Metric Tons of annual capacity, with operations expected to begin by late 2028. Polypropylene’s lightweight, durability, and thermal resistance make it a preferred alternative to traditional materials such as metals in structural and packaging applications.

Beyond polypropylene, propylene is used in the production of acrylonitrile (for ABS plastics), propylene oxide (used in foams and coatings), and cumene (a precursor for phenol and acetone). Ongoing innovation and material substitution trends continue to drive the expansion of propylene-based products.

3. Aromatics: Benzene, Toluene, and Xylene (BTX)

Aromatic compounds, including benzene, toluene, and xylene (collectively referred to as BTX), are essential for producing a range of downstream products such as resins, nylon, and synthetic fibers. Benzene remains highly utilized for producing styrene and phenol, key ingredients in engineering plastics and adhesives. In March 2025, Lotte Chemical announced the startup of its USD 3.9 Billion Cilegon facility in Indonesia, which will manufacture key BTX products to support regional and global petrochemical demand.

Toluene is processed into toluene diisocyanate (TDI), used in flexible foams for furniture and automotive seating. Xylene, particularly para-xylene, is in demand for manufacturing purified terephthalic acid (PTA), a precursor to polyester and PET bottles. As transport fuels undergo decarbonization, producers are investing in integrated refining-petrochemical complexes to optimize BTX production.

4. Methanol and Its Derivatives

Methanol is gaining importance due to its role in producing formaldehyde, acetic acid, and MTBE, as well as in methanol-to-olefins (MTO) technologies. Additionally, methanol is being adopted as an alternative fuel source in marine, industrial, and transportation applications. Latin America and Southeast Asia are seeing significant investments in green methanol projects using biomass and carbon capture-based hydrogen. For example, in October 2024, HIF Global launched its first Brazilian project to produce 800,000 tons of e-methanol annually from green hydrogen, utilizing 1.6 GW of electrolyzers and captured CO2.

5. Bio-Based and Sustainable Petrochemicals

Sustainability trends are accelerating the development of bio-based petrochemicals such as bio-ethylene, bio-PET, and green methanol. In July 2025, Chevron Lummus Global and INA successfully produced sustainable aviation fuel and renewable diesel from biogenic feedstocks at Croatia’s Rijeka Refinery, demonstrating scalable bio-based fuel integration in existing infrastructure.

Derived from renewable feedstocks like sugarcane and agricultural waste, these products support compliance with environmental regulations and consumer demand for lower-emission materials. Further, bio-based derivatives are projected to expand within specialty chemicals, driven by advancing technologies and public-private collaboration supporting commercial-scale adoption.

Regional Trends and Demand Centers:

North America

North America holds a strategic position in the petrochemical industry, underpinned by abundant natural gas liquids and advanced infrastructure. The region’s cost-effective feedstock and policy-driven sustainability measures enable stable expansion across ethylene, methanol, and polymer production, supporting both domestic growth and export competitiveness.

Key Trends:

- Significant investments in ethane-based ethylene production in the US Gulf Coast states

- Widespread adoption of chemical recycling and carbon capture technologies

- Increasing use of digital monitoring systems in process optimization

In February 2025, TCL USA announced a USD 200 Million investment in a West Virginia plant to produce maleic anhydride and specialty chemicals, with operations expected to begin in Q4 2025. Moreover, petrochemical demand in North America is driven by the packaging, construction, and automotive sectors. Continued growth is also supported by downstream chemical exports, proximity to end-markets, and the development of integrated refining and petrochemical hubs across the US.

Europe

Europe is transitioning toward climate-aligned petrochemical production, driven by regulatory frameworks under the EU Green Deal. Investments in low-emission feedstocks, specialty chemicals, and closed-loop systems are accelerating as producers adapt operations to remain compliant, competitive, and aligned with circular economy mandates and carbon reduction targets.

Key Trends:

- Expansion of hydrogen-based and electrified production systems

- Strong emphasis on ESG-compliant operations and traceability

- Shift toward high-margin, specialty petrochemical derivatives

- Adoption of chemical recycling and advanced recovery technologies

In May 2025, the Kassø e-methanol facility in Denmark was officially inaugurated, becoming the world’s first commercial-scale plant producing e-methanol using renewable power and carbon capture technologies. Moreover, demand stems from high-performance applications in automotive, pharmaceuticals, electronics, and food packaging. End-users prioritize traceability and low environmental impact, prompting the industry to develop value-added, sustainable solutions.

Asia-Pacific

Asia-Pacific is a key center for petrochemical manufacturing and end-use growth, with countries expanding local production to enhance industrial resilience. In May 2023, BPCL announced a USD 5.95 Billion ethylene cracker project at its Bina refinery in India, targeting expanded production of ethylene, propylene, polyethylene, and polypropylene by FY 2027–28. Governments across the region support backward integration in polymers and chemicals, prioritizing feedstock diversification and infrastructure development.

Key Trends:

- Ongoing expansion of domestic ethylene, polypropylene, and aromatics capacity

- Development of automation-enabled petrochemical complexes

- Rising implementation of plastic waste regulations and circular policies

Demand across Asia-Pacific is broad-based, spanning construction, textiles, packaging, automotive, and electronics. Population growth, rising incomes, and urbanization continue to increase per capita consumption, while regulatory reforms and foreign investments are reshaping the structure of downstream petrochemical markets regionally.

Middle East and Africa

The Middle East is strengthening its position in value-added petrochemical manufacturing through integrated complexes and feedstock optimization. Africa is advancing selectively, focusing on refinery-linked chemical zones to support local industrialization and enhance access to fertilizers, plastics, and construction inputs for regional development.

Key Trends:

- Deployment of crude-to-chemicals and derivative park projects

- Expansion into methanol, ammonia, and urea production

- Exploration of green hydrogen and blue ammonia technologies

- Public-private partnerships in African countries for infrastructure upgrades

In June 2025, Algeria announced petrochemical and refining projects worth USD 7 Billion, aiming to raise hydrocarbon conversion rates to 50% by 2029, including new refineries and cracking units.

Also, regional demand centers include fertilizer chemicals in agriculture, building materials for infrastructure, and consumer goods packaging. Middle Eastern producers target export markets, while African countries are focused on meeting domestic demand growth.

Latin America

Latin America is strengthening its petrochemical production base through targeted investments in bio-based chemicals, ethylene, and gas-fed methanol. Key economies are aligning with sustainability goals by leveraging biomass, shale gas, and regional integration to reduce dependency on imports and increase value-added production capacity.

Key Trends:

- Expansion of bio-polymer production in Brazil using renewable feedstock

- Capacity upgrades in Mexico supported by USMCA trade incentives

- Infrastructure development near Vaca Muerta shale in Argentina

Demand is led by agriculture (fertilizers and films), consumer packaging, and construction materials. Increasing regional consumption and trade integration are encouraging localized production, enabling Latin America to serve domestic needs and selected export markets efficiently.

-(1)_11zon.webp)

Sector Innovations and Technology Drivers:

- Process Automation and Digital Twins

Digital twins, virtual replicas of plants, are being used to simulate, predict, and optimize production performance in real-time. Operators gain insights into equipment wear and energy consumption, leading to significant cost savings.

- AI and Predictive Maintenance

AI-powered analytics support yield optimization, maintenance scheduling, and logistics planning. Advanced algorithms detect early signs of asset fatigue and recommend interventions before costly failures occur.

- Advanced Catalysis

Catalyst innovation is enhancing reaction selectivity, reducing by-products, and enabling lower-temperature operations. Companies are also using nanotechnology to develop next-generation catalytic converters for cleaner emissions.

- Carbon Capture and Utilization

CCU solutions are being deployed at scale in integrated petrochemical plants, particularly in the US and Europe. Captured CO2 is converted into polymers, synthetic fuels, or building materials, turning waste into value.

- Recycling and Circular Economy

Technologies such as pyrolysis, depolymerization, and solvent-based extraction allow for chemical recycling of mixed plastic waste. These processes deliver virgin-quality polymers, meeting growing demand for recycled content in consumer products.

Market Challenges and Risks:

- Feedstock and Price Volatility: Crude oil and natural gas prices continue to fluctuate due to geopolitical tensions, OPEC+ decisions, and speculative trading. This affects raw material costs, profit margins, and investment predictability for petrochemical plants.

- Capital Intensity and Long Payback Periods: The development of large-scale petrochemical plants involves significant capital expenditure and extended project timelines.

- Environmental and Regulatory Pressures: The industry is subject to stringent environmental regulations, requiring continuous upgrades and investments to ensure compliance with emissions, resource usage, and sustainability reporting standards.

- Workforce and Talent Constraints: There is a noticeable shortage of skilled professionals in process engineering, automation, and compliance, necessitating strategic efforts in workforce development, retention, and specialized skill enhancement.

- Global Supply Chain Disruptions: Port congestion, shipping container shortages, and geopolitical instability (e.g., Middle East tensions, trade restrictions) are impacting raw material flow and delivery schedules.

Strategic Insights for Stakeholders:

- Integrate Production Facilities: Combine refining and petrochemical operations to maximize feedstock flexibility and margin control.

- Invest in Net-Zero Tech: Adopt renewable energy sources, CCS systems, and green hydrogen inputs to future-proof operations.

- Localize Sourcing: Develop regional supply chains to reduce risk exposure and improve resilience.

- Leverage Data: Use AI, IoT, and cloud platforms to streamline supply chains, sales forecasting, and quality control.

- Differentiate Through ESG: Build brand equity and attract investors by aligning with ESG benchmarks and transparent reporting.

Conclusion:

- The petrochemical industry in 2025 is shaped by rising demand, innovation in key segments, and pressure to align with sustainability and digitalization goals. Key segments such as ethylene, polypropylene, aromatics, and methanol continue to expand, supported by infrastructure growth and regional diversification. Regional shifts and operational challenges require precise, forward-looking strategies.

- IMARC delivers actionable intelligence and tailored advisory to help companies navigate complexity, optimize performance, and achieve long-term growth in a competitive global landscape.

How IMARC Can Help:

IMARC Group offers data-driven insights and strategic support to businesses navigating the evolving petrochemical market. Our services help companies gain clarity on emerging trends, competitor activity, and investment feasibility.

Our capabilities include:

- Segment-specific market size forecasts

- Investment feasibility studies and ROI modeling

- Industry benchmarking and SWOT analysis

- Location-based opportunity mapping

- Go-to-market and regulatory strategy support

- Support for technology assessment and partner selection

Whether you are entering a new market, expanding capacity, or digitizing operations, IMARC helps you minimize risk and maximize growth potential.

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

Ethyl acetate is a volatile, colorless, flammable liquid having a characteristic sweet smell. It is primarily used as a solvent in various industrial and commercial applications. It finds primary production through esterification from ethanol and acetic acid.

Ammonium nitrate (NH4NO3) is a white solid that is widely used as a high-nitrogen fertilizer and as a component of industrial explosives. It is made by neutralization of ammonia with nitric acid and is very soluble in water, making it useful for its efficiency in providing nitrogen to plants.

Ceramic tiles are durable, versatile, and cost-effective building materials made from natural clay, sand, and water, which are shaped, glazed, and kiln-fired at high temperatures. Known for their aesthetic appeal, resistance to moisture, and ease of maintenance, ceramic tiles are widely used in flooring, walls, kitchen backsplashes, and bathrooms across residential, commercial, and industrial spaces.

Diethylenetriamine (DETA) is a colorless, hygroscopic organic chemical compound of the ethyleneamine group having the chemical formula HN(CH2CH2NH2)2. It is a triamine that contains two primary amine groups and one secondary amine group, thus imparting to it a highly reactive molecular structure to be used in a number of industrial processes.

Calcium Chloride Anhydrous (CaCl2) is an off-white, hygroscopic inorganic substance commonly utilized due to its high desiccating and exothermic properties. The anhydrous form, as opposed to its hydrated counterparts, has no water molecules within it, thus making it very effective to use in moisture control processes.

Explore a step-by-step guide to setting up a unsaturated polyester resin production plant including planning, machinery, raw materials, costs & demand drivers.

Explore the growth, trends, and innovations driving the global bio-lubricant market toward a sustainable future.

Medium Density Fibreboard (MDF) is an engineered wood product created by dissolving hardwood or softwood residues into wood fibers, blending them with wax and resin binders, and molding them into panels under the pressure of high temperature. MDF is renowned for its even density, smooth surface, and easy machinability and is used extensively in cabinetry, flooring, furniture, and interior decoration because of its relative cheapness and adaptability as compared to plywood and solid wood.

Lanthanum oxide (La2O3) is a white, odorless, and extremely stable rare earth compound obtained mainly from monazite and bastnäsite ores. It is essential for a vast array of industrial uses such as the manufacture of optical lenses, ceramics, phosphors, and battery electrodes. Lanthanum oxide is also used extensively as a catalyst in petroleum refining processes, particularly in fluid catalytic cracking (FCC) operations. Due to its exceptional electrical, optical, and catalytic properties, La2O3 is an important material for advanced technologies like electric vehicles (EVs), smart electronics, and renewable energy devices.

Silica sand is a pure quartz-based material used extensively by many industries. It is known for its durability, chemical inertness, and resistance to heat, and it is an important raw material in glass production, construction, foundries, electronics, and hydraulic fracturing (fracking). Increasing demand for high-purity silica in semiconductors, solar panels, and filters is fueling market growth. With more infrastructure development and development in silica processing, the applications keep expanding, and it is becoming an essential industrial commodity worldwide.

Stone paper is an innovative, eco-friendly material gaining traction across various industries due to its durability, sustainability, and water resistance. Made primarily from calcium carbonate and resin, it offers a tree-free alternative to traditional paper, reducing deforestation and water consumption. Its tear-resistant and smooth texture makes it ideal for printing, packaging, and stationery applications. Additionally, stone paper is recyclable, photodegradable, and highly resistant to moisture, making it suitable for outdoor and high-humidity environments. With growing environmental concerns and demand for sustainable packaging and printing solutions, stone paper is emerging as a key player in the global paper industry, attracting interest from publishers, packaging manufacturers, and eco-conscious brands.

Nitrile gloves are synthetic rubber gloves that are extensively used in the medical, industrial, and food industries because of their strength, resistance to chemicals, and hypoallergenic nature. They are ideal for people with allergies since they are latex-free, as opposed to latex gloves. They are more flexible, puncture-resistant, and resistant to infection and chemicals. The demand for nitrile gloves in manufacturing, healthcare, and laboratory environments is increasing because of stringent safety regulations and increasing hygiene consciousness, which is driving the worldwide market growth.

Acetic acid (CH3COOH) is a clear, colorless liquid organic compound with a sour taste and a pungent odor. It is produced by the carbonylation of methanol and is also manufactured via bacterial fermentation. Acetic acid is extensively employed in the manufacturing of vinyl acetate monomer (VAM), purified terephthalic acid (PTA), acetic anhydride, and ester solvents, among others. It provides solvent effectiveness, chemically useful to use in syntheses, as well as utilization in the fabrication of polymers and resins.

Calcium bromide (CaBr2) is an inorganic compound commonly used in drilling fluids for oil and gas exploration, as well as in pharmaceutical and photographic applications. It is a white, crystalline solid or solution that dissolves very easily and is used as a clear, dense brine in well drilling operations. Calcium bromide is prized for its capacity to manage pressure and avoid well blowouts due to its exceptional thermal and chemical stability. The growing energy industry and improvements in drilling technology are the main drivers of its demand.

Laminated veneer lumber (LVL) is one of the most popular engineered wood products, which is manufactured from sliced and peeled thin wood veneers. LVL is a light material used for construction, which is utilized in public structures, industrial warehouses, product parts, large, prefabricated buildings, as well as designed wooden homes. This can be attributed to its strength, uniformity, high strength, and dimensional accuracy. Apart from this, it is utilized for structural framing in residential and commercial building work, including lintels, joists, beams, purlins, scaffold boards, concrete formwork, and truss chords.

Cross-laminated timber (CLT), an engineered wood product, is renowned for its durability, strength, and adaptability in contemporary building. CLT provides a lightweight yet strong substitute for steel and concrete in structures with sustainable engineering. Its layered structure adds to its integrity and makes it suitable for building anything from residential to commercial to high-rise buildings. Besides being aesthetically pleasing for eco-friendly building projects, CLT has very good fire resistance, thermal performance, and ease of installation. CLT changes the architectural sphere and instigates the development of new concepts for urban environments and shaping the future of sustainable construction.

Copper wire is a versatile, flexible, and highly conductive electrical wire used extensively in power transmission, telecommunications, and electronics. Fabricated from pure copper, copper wire has good thermal and electrical conductivity, resistance to corrosion, and ease of processing. Copper wire plays a critical role in construction, automotive, and consumer electronics industries. With the increased demand for effective power distribution and advancing technology, the copper wire market keeps growing because of urbanization, electrification, and growth in infrastructure development globally.

Aluminum wire rods are critical industrial products renowned for their high conductivity, strength, and versatility. They are cylindrical metal rods that are the backbone of electrical transmission and distribution systems and play a fundamental role in power infrastructure, building construction, and manufacturing. Due to their good conductivity and low weight, they are a top choice for cable production, overhead power lines, and electrical wires. Outside of electrical uses, aluminum wire rods find extensive application in the automotive, aerospace, and industrial industries, where their corrosion resistance and recyclability play important roles in sustainability initiatives.

N-Methyl Aniline (NMA) is an organic chemical compound widely used as an intermediate in various industrial applications. It plays a crucial role in the production of dyes, agrochemicals, pharmaceuticals and fuel additives. As a key component in high-octane fuel formulations NMA enhances combustion efficiency and reduces engine knocking making it valuable in the automotive and petroleum industries. Its use in the synthesis of specialty chemicals and pigments further expands its industrial significance.

Ammonium perchlorate is a crystalline, white inorganic substance that finds principal application as an energetic oxidizer in solid rocket propellants, explosives, and pyrotechnics. Its release of oxygen when subjected to heat gives it a fundamental role in different industrial and technological processes. Aside from its primary application in propulsion systems, it is also used in pyrotechnic devices to generate controlled, vibrant flames and brilliant effects, especially in aerospace displays and enormous entertainment productions.

Potassium sulfate (K2SO4) is an inorganic compound widely used as a specialty fertilizer, providing essential potassium and sulfur nutrients to crops. Its low salt index makes it the preferred crop for crops that are sensitive to chloride, like fruits, vegetables, and tobacco. Potassium sulphate is also used in pharmaceutical and glass manufacturing processes, among other industrial processes. It is the perfect choice for contemporary agricultural methods because of its high solubility and compatibility with irrigation systems, which promote plant development, yield enhancement, and soil health maintenance.

Battery electrolyte is a key element of energy storage, facilitating the flow of ions between electrodes to drive devices effectively. It is an important factor in lithium-ion, solid-state, and future batteries, influencing performance, safety, and durability. In electric vehicles, renewable energy storage systems, and consumer devices, development in electrolyte technology targets sustainability, improved conductivity, and heat resistance for unlocking the future of clean energy technologies.

Cobalt acetate is an inorganic substance that is frequently utilised in chemical synthesis as a precursor, dye mordant, and catalyst. This crystalline solid has a reddish-purple appearance and is very soluble in organic solvents and water. In addition to being widely used in the manufacture of paints, inks, and adhesives, it is also an essential component of polyester and a catalyst in oxidation processes. It is a crucial component in many industries, with industrial uses driving its demand, especially in petrochemicals, textiles, and battery technology.

Transformer oil, sometimes referred to as insulating oil, is essential to electrical transformer operation. Its main functions are to cool and insulate the internal parts. By acting as a dielectric medium, the oil prolongs the transformer's lifespan and improves overall performance by preventing electrical discharges between various components. It moves around inside the transformer, assisting in the dissipation of heat produced during the conversion of energy. Although there are synthetic and bio-based substitutes, refined mineral oil is usually the source of it. Moisture, impurities, or the disintegration of the oil's chemical structure can all cause its quality to decline over time. It must be tested and maintained on a regular basis to stay effective.

Silica gel is obtained from silica dioxide a naturally occurring compound in sand and comprises fine particles that can soak quantity of water. It is a drying agent that is frequently packaged in tiny paper or cloth packets as tiny, transparent beads or crystals of clear rock. These packets are frequently included with business goods to guard against moisture-related damage. Food, clothing, and electronics are just a few of the many things that include silica gel packets. Although silica gel is typically non-toxic, it poses a choking hazard, particularly to young children.

Amorphous silicon dioxide (silica) particles dispersed in water are known as colloidal silica. In order to produce these amorphous silica particles, silica nuclei from silicate solutions are polymerised in an alkaline environment to create silica sols with a high surface area and a nanometre size. The surface of the silica nanoparticles is then charged, which causes the particles to reject one another and create a stable colloid, or dispersion. Although colloidal silica comes in a variety of grades, all of them are made up of silica particles that range in size from roughly 2 nm to 150 nm. The particles might exist as discrete particles or as slightly organised aggregates, and they can have a spherical or slightly irregular shape.

In a time characterized by environmental awareness and limited resources, sustainable manufacturing has become an essential priority for companies all over the world. Sustainable manufacturing is a model beyond conventional manufacturing practices, focusing on the production of goods in a manner that reduces harm to the environment, uses less energy and natural resources, and prioritizes the health and safety of workers, communities, and consumers.

Intravenous (IV) solutions represent a critical and ubiquitous component of modern healthcare, playing a fundamental role in patient care and treatment. These sterile, liquid formulations consist of a carefully balanced blend of fluids and electrolytes, administered directly into a patient's bloodstream. They are tailored to address a wide range of medical needs, from rehydration and medication delivery to nutritional support and blood transfusions.

Titanium dioxide (TiO 2) is a white, naturally being mineral extensively used as a pigment, UV blocker, and opacifier. A vital element of paints, coatings, plastics, cosmetics, and sunscreens, it's well- known for its exceptional opacity, high illumination, and superior light- scattering capabilities. Also, TiO 2 is essential for advanced operations like photocatalysis, food, and pharmaceuticals. Because of its non-toxic and chemical- resistant rates, it's a necessary element of numerous different sectors, performing in steady demand worldwide.

Yellow phosphorus, a chemical element with the symbol P and atomic number 15, is a fascinating and essential element in the periodic table. This highly reactive nonmetal is widely known for its distinctive yellow appearance and its crucial role in various industrial applications. Found in nature primarily as phosphates, yellow phosphorus is isolated through a complex process to ensure its purity and effectiveness. Its versatility allows it to be employed in the production of fertilizers, detergents, and even in the synthesis of organophosphorus compounds used in medicine and pesticides.

Xanthan gum is a food additive that is produced by fermenting simple sugar using bacteria. It quickly disperses and creates a viscous and stable solution when added to a liquid for providing a thickness or stabilizing effect to a product. It assists in improving the texture, flavour, consistency, appearance, and shelf life of a product. It aids in preventing food products from separating and allowing them to flow smoothly and can lower blood sugar levels among individuals. It also reduces cholesterol levels, slows digestion, supports weight loss management, and treats dry mouth problems.

Titanium sponge is a highly porous, lightweight form of titanium metal produced through the Kroll process. It is the major raw material in the production of titanium alloys in industrial, automotive, medical implant, and aerospace applications. For high-performance industries, titanium sponge is an indispensable component as it has a very high strength-to-weight ratio, is resistant to corrosion, and is biocompatible. It is prepared by reducing titanium tetrachloride (TiCl4) with magnesium, followed by purification and processing to produce titanium compounds that can be used.

Urea is a nitrogenous compound produced in living organisms as a byproduct of the metabolism of protein degradation. In industrial and agricultural use, urea is a synthetic compound produced on a large scale for use as a fertilizer. Urea is a critical source of nitrogen that helps to enhance plant growth and development. Its high content of nitrogen makes it popular in the agricultural sector and serves as a concentrated, readily available source of nitrogen for crops. Besides being a fertilizer, urea also has several industrial uses, such as the manufacture of adhesives and some resins, as well as plastics.

Active dry yeast is a dehydrated form of yeast commonly used in baking and fermentation. Its dormant yeast cells spring to life when they are rehydrated with warm water. In bread-making, brewing, and other fermentation operations, active dry yeast is frequently employed due to its extended shelf life and convenience of storing. It aids in flavour development and raises dough by generating carbon dioxide. It is a necessary component of both commercial and home baking due to its dependability and convenience.

Ethylene-vinyl alcohol, commonly referred to as EVOH, is an extraordinary polymer with outstanding properties that have revolutionized applications in packaging, industrial, and medical fields. The copolymer consists of alternating ethylene and vinyl alcohol monomer units, which result in the unique gas barrier property that makes EVOH a strong contender for food packaging applications.

Ethylene propylene diene monomer (EPDM) is an adaptable synthetic rubber with unique performance properties. It is a copolymer of ethylene, propylene, and diene monomers and is manufactured through suspension, solution polymerization, or gas-phase polymerization processes. It is commonly used in belts, window and door seals, tubing, roofing membrane, non-slip coatings, radiator, drain tubes, and trunk seals.

Ferrosilicon, an iron alloy made of silicon and iron, is a very versatile alloy that is used in many different industries, especially the steel and casting industries. Its composition can vary, with silicon content ranging from 15% to 90%, depending on the application and desired properties.

Polytetrafluoroethylene (PTFE) refers to a tough, waxy and non-flammable synthetic resin that consists of carbon and fluorine atoms. It is manufactured through the free-radical polymerization process of chloroform, fluorspar and hydrochloric acid. PTFE is usually used to give a non-stick coating to surfaces, especially cookware, such as pans and baking trays and industrial products.

Collagen in the connective tissues, bone, and skin of cows and pigs contains gelatin. A common method for creating this colourless, odourless animal protein is to boil ligaments, tendons, and skin in water. Its outstanding physical characteristics include low viscosity, dispersion stability, high affinity, and dispersibility.

Electrolytic manganese dioxide (EMD) is made by dissolving manganese dioxide in sulfuric acid and placing between two electrodes. Manganese dioxide, also referred to as Manganese (IV) oxide, is an inorganic compound that is commonly found in blackish or brown solid and is insoluble in water. EMD is a highly refined form of MnO2 designed to meet the specific electrical requirements of battery manufacturers.

Electrolytic manganese metal is a pure form of the metallic element manganese, Mn concentration ranges from 99.7% to 99.9%. It is termed "electrolytic" because the refining process involves electrolysis. In other words, a chemical reaction powered by an electric current. Heating the ore and applying chemical processes to remove most impurities is the first steps in the processing of manganese.

Ethanol is a renewable biofuel produced primarily from crops such as corn, sugarcane, and biomass. It is often added to fuel to lower carbon emissions and improve energy security. Additionally, ethanol is used in the beverage, chemical, and pharmaceutical sectors. Ethanol is becoming more popular as a cleaner substitute for fossil fuels due to the rising need for sustainable energy solutions, which is propelling improvements in biofuel technology and production efficiency.

Widely recognized for its superior mechanical, chemical, and thermal properties, unsaturated polyester resin (UPR) is a highly versatile thermosetting polymer utilized across multiple industries. UPR is created when unsaturated acids and glycols react mostly used in composites, coatings, and adhesives.

Sodium cyanide (NaCN) is a highly toxic, colorless crystalline compound with a faint almond-like odor. It is a water-soluble salt composed of sodium (Na+) and cyanide (CN-) ions, known for its versatile applications across various industrial sectors. Despite its hazardous nature, sodium cyanide is extensively used due to its unique properties and efficacy in specific processes.

Caustic soda is the common term for sodium hydroxide (NaOH), a versatile alkali widely used in industries such as chemicals, textiles, pulp and paper, detergents, and water treatment. Sodium hydroxide is known to have strong alkaline properties. It is employed in manufacturing processes such as saponification, pH regulation, and chemical synthesis, making it essential for diversified industrial applications.

Citric acid is a naturally occurring weak organic acid found in citrus fruits, widely used for its sour taste, preservative properties, and acidity regulation. Industrially, it is produced through the fermentation of sugars and is a key ingredient in the food and beverage industry, where it enhances flavor and preserves freshness. Additionally, it has applications in pharmaceuticals, cosmetics, and cleaning products due to its ability to stabilize ingredients and chelate metals.

Calcium stearate, a key chemical compound, holds significant importance across various industries due to its multifunctional properties. Comprising calcium and stearic acid, it serves as a versatile additive and processing aid. As a widely utilized stabilizer and lubricant in the manufacturing of plastics, rubber, and pharmaceuticals, calcium stearate plays a pivotal role in enhancing material properties and processing efficiency.

Calcium hypochlorite is a powerful chemical compound, widely used in many different applications and industries. This white solid, made up of calcium, oxygen, and chlorine, contains excellent chlorine content with a strong oxidation capability. Being an oxidizing agent that gives out chlorine when dissolved in water, it is in huge demand for the treatment, sanitation, and disinfection of water.

Nitrocellulose, also known as cellulose nitrate or guncotton, is a chemically modified form of cellulose known for its exceptional film-forming capabilities, strong adhesion, and biodegradability. It is widely used in applications such as wood coatings, printing inks, leather finishes, automotive paints, nail varnishes, and more.

The growth of the copper wire market is primarily driven by increased electricity demand, heightened investments in construction, expansion of electrical infrastructure, the rise of renewable energy, a shift toward electric vehicles in the automotive industry, and the growing adoption of electric appliances. The development of smart grids and investments in upgrading power transmission systems further boost global copper wire demand. Additionally, the telecom industry's use of copper in optic fiber cables and infrastructure development in emerging markets, especially in Asia Pacific and Latin America, are expected to sustain high demand for copper wire in the coming years.

Urea, also known as carbamide, is an organic compound with the formula CO(NH2)2. It is a highly versatile and widely used chemical, primarily known for its role in agriculture as a nitrogen fertilizer. Urea is available in various grades, including fertilizer grade, feed grade, and technical grade, and is used in a wide range of applications, such as nitrogenous fertilizers, stabilizing agents, keratolytic, and resins, among others. Key industries that utilize urea include agriculture, chemicals, automotive, and medical sectors.

Lithium-ion batteries are rechargeable power sources widely used in devices such as cell phones, laptops, and electric vehicles. These batteries store energy by transferring lithium ions between the anode and cathode electrodes, with the electrolyte facilitating this movement and generating free electrons at the anode. Key types of lithium-ion batteries include those with lithium cobalt oxide, lithium iron phosphate, lithium nickel manganese cobalt, and lithium manganese oxide. Lithium-ion batteries come in a range of capacities from 0 mAh to 6000 mAh. They offer several advantages, including a high energy-to-weight ratio, excellent charge retention, and generally longer lifespans with more charge/discharge cycles compared to other rechargeable batteries.

Brazil is renowned across the world for its enormous rainforests and agricultural resources. Over the recent years, the country has emerged as a major player in the global cellulose industry. As per IMARC estimates, the cellulose fiber market in Brazil was valued at US$ 740.4 Million in 2023. By 2032, the market is projected to reach US$ 1,379.9 Million, growing at a CAGR of 7.0% from 2024 till 2032. Strategic investments in the industry, along with favorable environmental conditions, are guiding a cellulose revolution in Brazil, which is likely to have profound implications for both regional and international markets.

Green chemistry refers to the practice of creating new chemicals, materials, and processes that are less toxic to human health and the environment. It comprises the utilization of renewable resources and reducing waste and energy consumption. Green chemicals are used in various applications such as industrial and chemical, food and beverages, automotive, packaging, construction, agriculture, personal care, and many others. Nowadays, different types of green chemicals are available in the market, including bio-alcohol (bioethanol, bio-butanol, bio-methanol, and many others), bio-organic acids (bio-lactic acid, bio-acetic acid, bio-citric acid, bio-adipic acid, bio-acrylic acid, bio-succinic acid, and others), biopolymers (poly-lactic acid, bio-polyethylene, and others), bio-ketones, bio-solvents, and many other organic acids.

Vanadium has been discovered in sediment samples collected from the Gulf of Khambhat, which opens into the Arabian Sea off Alang in Gujarat. This discovery is expected to enhance the production of steel and titanium in India and boost redox battery manufacturing. Vanadium is one of the most abundant transition metals and is typically found in various minerals, including vanadinite, patronite, and carnotite. It is a hard, ductile, and rare grey metal, often extracted as a byproduct while processing other metals such as iron and uranium.

Steel is a versatile and widely used alloy composed primarily of iron and carbon, with small amounts of other elements such as manganese, chromium, nickel, and others. It is a widely utilized material in construction, manufacturing, and various industries. Steel exhibits a range of desirable properties, including high tensile strength, durability, hardness, corrosion resistance, heat resistance, and the ability to be formed into different shapes. Carbon steel, alloy steel, stainless steel, and tool steel are the main types of steel. Steel is utilized in the manufacturing of various products, including ingots, semi-finished materials, hot-rolled sheets and coils, galvanized sheets, steel tubes and fittings, plates, wire rods, and many others. Its applications span various industries such as building and construction, electrical appliances, metal products, automotive, transportation, and mechanical equipment. The top five exporters of steel are China, Japan, South Korea, and Germany. Similarly, the major importers of steel include the United States, Germany, Italy, and Turkey.

Copper is an essential material in electrical wiring, electronics, and heating systems. It is also highly ductile and malleable, allowing it to be easily shaped and drawn into thin wires. Additionally, copper possesses antimicrobial properties, making it useful in medical and architectural applications. Its resistance to corrosion and its ability to form alloys with other metals further enhance its versatility across various industries.