Future of the Japan Robo Taxi Industry: Trends and Outlook to 2033

Introduction to Japan’s Robo Taxi Industry:

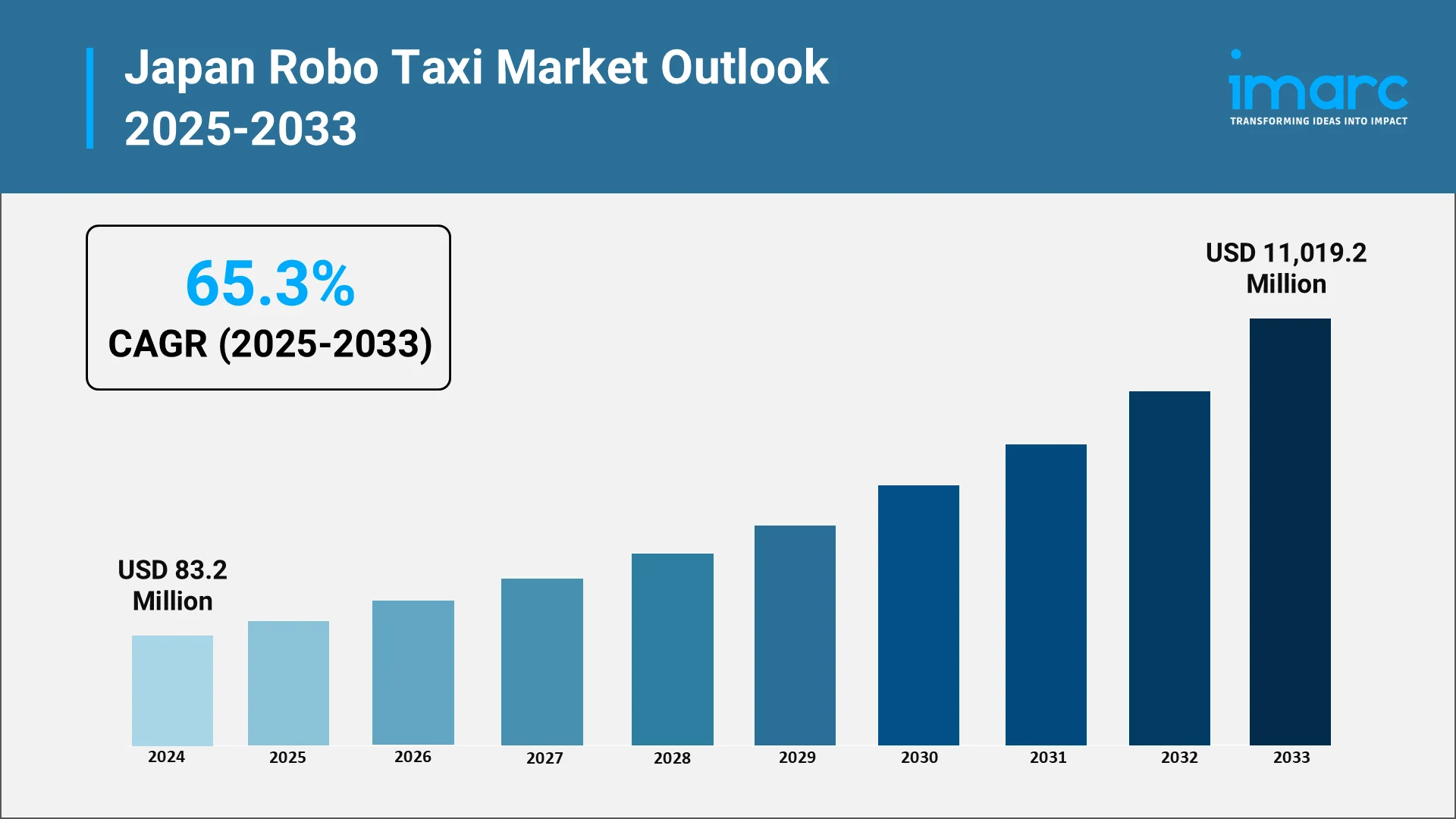

Japan’s transportation landscape is on the brink of a major shift, with robo taxis, autonomous, driverless vehicles designed for passenger and goods transport, emerging as a practical mobility solution. The Japan robo taxi market reached USD 83.2 Million in 2024. This remarkable expansion reflects Japan’s broader move toward smart mobility, sustainability, and automation.

The convergence of artificial intelligence, sensor technology, and electric propulsion is reshaping how people and goods move across urban centers like Tokyo, Osaka, and Nagoya. Rapid urbanization, traffic congestion, and demographic challenges, such as an aging population, are amplifying the demand for autonomous transport. As a result, robo taxis are poised to play a pivotal role in Japan’s future mobility ecosystem, reducing human-error-related accidents, improving accessibility, and supporting carbon-neutral transportation goals.

Market Size and Growth Potential by 2033:

The market is projected to soar to USD 11,019.2 Million by 2033, registering a CAGR of 65.3% during 2025–2033. The market’s projected jump from USD 83.2 Million more than USD 11.0 Billion in less than a decade underscores the depth of investment and regulatory alignment Japan has achieved in autonomous transport. This growth trajectory is supported by pilot programs launched across major regions, notably in the Kanto and Kansai/Kinki areas, where population density and infrastructure readiness are highest.

Passenger applications dominate current deployments, but the goods-transport segment is gaining momentum as logistics companies explore last-mile delivery automation. In 2024, Japan’s Ministry of Land, Infrastructure, Transport and Tourism (MLIT) approved several commercial pilot projects allowing Level 4 autonomous vehicles to operate on designated public routes. The Japanese Ministry of Economy, Trade and Industry selected TIER IV in 2024 to lead mobility digital transformation projects. The government aims to promote Level 4 autonomous transport services across more than 100 municipalities by 2027. These approvals signaled the transition from controlled testing to scalable deployment, establishing Japan as one of the first Asian markets ready for regulated robo taxi services.

Explore in-depth findings for this market, Request Sample

Technological Innovations Driving the Market:

Robo taxis rely on a blend of technologies, LiDAR, radar, high-resolution cameras, and AI-driven navigation systems, that collectively enable precise real-time decision-making. Recent advancements in Japan’s automotive and robotics industries have accelerated their adoption.

Japanese automakers such as Toyota, Nissan, and Honda are leading initiatives to integrate Level 4 and Level 5 autonomy into electric-vehicle platforms. Toyota’s Woven City project in Shizuoka Prefecture serves as a living laboratory for connected autonomous mobility, including electric robo shuttles and station-based fleets. Meanwhile, advances in solid-state battery technology are improving vehicle range and reducing energy costs—key prerequisites for fleet viability.

The integration of AI-based traffic management and edge computing also stands out. These systems allow robo taxis to process high volumes of sensor data locally, improving reaction time and reducing dependence on centralized networks. The result is a more resilient and responsive autonomous-mobility ecosystem that aligns with Japan’s precision-engineering ethos.

Some of the most recent developments in the market include:

- In December 2024, Waymo announced plans to begin testing its autonomous vehicle technology in Tokyo in early 2025, marking the first time its robotaxis will operate on public roads outside the United States. The initiative, launched under Waymo’s “road trips” development program, will introduce a small fleet of self-driving Jaguar I-Pace vehicles operated in partnership with GO and Nihon Kotsu, initially focusing on key Tokyo districts such as Minato, Shinjuku, and Shibuya. This expansion highlights Japan’s growing role in the global robotaxi market, aligning with the country’s ambition to integrate advanced autonomous mobility solutions into dense urban environments.

- In May 2024, Japan-based autonomous driving pioneer TIER IV announced plans to launch its robotaxi service in Tokyo by November 2024, beginning with proof-of-concept operations in the Tokyo Bay Odaiba area. The initiative will initially focus on underserved routes and aims to expand coverage to major Tokyo districts by 2025 and the entire metropolitan area by 2027. TIER IV’s robotaxi, based on its Autoware open-source autonomous driving platform, has already demonstrated safety and reliability in heavy-traffic testing, marking a significant step toward Japan’s large-scale commercial deployment of self-driving taxis.

- In April 2024, Honda, in partnership with General Motors (GM) and Cruise, confirmed plans to launch a fully autonomous taxi service in central Tokyo by early 2026 using the Cruise Origin, a Level 4 self-driving vehicle with no steering wheel or pedals. The project builds on years of technology verification in Tochigi Prefecture, adapting the system for Japan’s traffic environment and regulatory standards. This milestone positions Honda among key players advancing Japan’s robo taxi market, aligning with national efforts to commercialize autonomous mobility and enhance urban transport efficiency.

- In February 2024, Nissan Motor Co. announced that it will commercialize autonomous-drive mobility services in Japan by fiscal year 2027, building on progress made through its long-running Easy Ride autonomous vehicle trials. The initiative uses a Nissan Leaf–based test fleet and aims to integrate Level 4 self-driving technology into public transport systems, focusing on dense urban routes. This plan reinforces Japan’s position as a frontrunner in the robo taxi market, with Nissan expanding its role in deploying safe, scalable, and sustainable autonomous mobility solutions nationwide.

.webp)

Government Policies and Regulatory Support:

Japan's regulatory framework for autonomous vehicles has evolved through deliberate legislative amendments designed to balance innovation encouragement with public safety mandates. Regulatory support remains one of Japan’s strongest enablers for autonomous mobility. The government’s Strategic Innovation Promotion Program (SIP) and Society 5.0 framework explicitly prioritize self-driving technologies as part of national digital transformation. In 2023, the Road Traffic Act was amended to permit Level 4 autonomous vehicles on public roads under defined operational conditions, providing legal clarity for robo-taxi operators. The Ministry of Economy, Trade and Industry (METI) has championed several programs including a ¥700 million (approx. USD 4.5 Million) grant initiative in 2024 to foster digital transformation in mobility by supporting robotaxi and autonomous truck projects.

Additionally, the MLIT and National Police Agency introduced detailed safety-assessment standards covering remote monitoring, cybersecurity protocols, and liability assignment for autonomous-driving incidents. The government’s National Comprehensive Digital Lifeline Development Plan (June 2024) aims to accelerate autonomous driving implementation, including establishing “autonomous driving service support roads” equipped with local 5G communications to enhance safety and data sharing. These initiatives aim to balance innovation with public safety and trust.

Beyond regulation, Japan’s commitment to decarbonization under the Green Growth Strategy 2050 supports the proliferation of electric and fuel-cell robo taxis. With the government offering incentives for EV adoption and hydrogen infrastructure, the regulatory environment strongly complements the sector’s technological ambitions.

Key Challenges and Barriers to Adoption:

Despite favorable regulatory conditions and technological maturation, Japan's robo taxi industry confronts multifaceted challenges that moderate deployment velocity and constrain near-term scaling potential.

- Infrastructure readiness remains uneven across regions. While metropolitan areas have robust 5G and smart-traffic infrastructure, rural prefectures lack the connectivity required for autonomous-vehicle operations. Building uniform digital infrastructure will be crucial for nationwide rollout.

- Public acceptance and safety perception also present challenges. Surveys conducted in 2024 showed that only about 38% of Japanese consumers expressed comfort with fully autonomous vehicles. Establishing consumer trust will depend on consistent safety records from pilot operations and transparent regulatory oversight.

- High deployment costs—stemming from lidar sensors, AI hardware, and cloud-computing systems—add another layer of complexity. The capital intensity limits small and mid-sized fleet operators from scaling quickly. Moreover, cybersecurity threats and data-privacy concerns around vehicle-to-infrastructure communication highlight the need for rigorous standards and resilient digital architecture.

- Lastly, workforce displacement in traditional taxi sectors remains a sensitive issue, necessitating retraining and transition programs as automation reshapes employment dynamics.

Future Opportunities and Outlook:

Japan’s robo taxi industry sits at the intersection of automation, electrification, and shared mobility—three defining themes of the next decade. The convergence of these forces presents diverse opportunities:

- Fleet Electrification and Sustainability: With Japan targeting carbon neutrality by 2050, the adoption of electric and hydrogen fuel-cell robo taxis will accelerate. Toyota is actively promoting hydrogen fuel-cell taxis in Tokyo, targeting approximately 600 fuel cell taxis by fiscal 2030, with 200 units scheduled for introduction by 2025. This is part of the "TOKYO H2" project led by the Tokyo Metropolitan Government, aiming to establish Tokyo as a global hydrogen leader and boost commercial hydrogen vehicle adoption.

- Urban Mobility-as-a-Service (MaaS): Integration with public-transport networks will enable seamless multi-modal journeys, positioning robo-taxis as connective tissue within Japan's extensive transit infrastructure. Station-based robo-taxi services in the Chubu and Kyushu-Okinawa regions are being designed to complement rail and bus systems rather than compete with them, addressing first-mile and last-mile gaps that conventional transit struggles to serve economically.

- Autonomous Goods Transport: The logistics sector is expected to become a major adopter, using autonomous vans and shuttles to address driver shortages and delivery-cost pressures that threaten service reliability across Japan's e-commerce ecosystem. Warehouse-to-port drayage, urban parcel delivery, and intercity freight corridors represent immediate deployment opportunities where predictable routes and controlled environments simplify autonomous system requirements.

- AI-Enhanced Passenger Experience: Personalized route optimization, dynamic pricing, and in-vehicle infotainment powered by machine learning will distinguish next-generation robo-taxi services from conventional ride-hailing offerings. These systems analyze historical traffic patterns, real-time congestion data, and individual passenger preferences to deliver customized journeys that balance speed, comfort, and cost according to user priorities.

- Cross-Industry Partnerships: Collaborations among automakers, telecom providers, and software firms, will define Japan’s leadership in autonomous-mobility ecosystems. For example, in March 2025, SoftBank Corp. announced the development of a “remote autonomous driving support system” powered by its AITRAS edge AI server, designed to enable safe operation of Level 4 autonomous vehicles during sensor malfunctions or unexpected conditions. The system was tested in collaboration with Keio University’s Shonan Fujisawa Campus, where trials demonstrated successful real-time obstacle recognition and safe stopping performance through 5G-enabled AI processing.

Looking ahead, the market’s 65.3% CAGR through 2033 positions Japan as a global front-runner in regulated, high-density autonomous transport. The transition from pilot to commercial scale will depend on how effectively stakeholders align technological readiness with public trust and sustainable operations. If successful, Japan’s robo-taxi model could become an exportable template for other nations seeking to combine safety, efficiency, and environmental stewardship in urban transport.

Why Choose IMARC for Market Analysis:

IMARC Group’s analysis of the Japan robo taxi industry is grounded in data-driven methodology and sector expertise that help businesses navigate emerging technologies with clarity and precision.

- Data Accuracy and Timely Forecasts: Reliable projections—such as the USD 11.0 billion market forecast and 65.3 % CAGR—reflect IMARC’s consistent validation against industry developments and regulatory updates.

- Holistic Coverage Across Segments: Reports include detailed insights by application, autonomy level, propulsion type, and region, enabling informed decisions for both investors and policymakers.

- Cross-Industry Context: Analyses integrate robotics, AI, electric-vehicle, and transport-infrastructure trends, offering a comprehensive view of how each domain shapes the robo-taxi ecosystem.

- Rigorous Analytical Framework: The firm’s research methodology emphasizes quantitative rigor, transparent assumptions, and validation through primary sources and industry interviews.

- Local Insight with Global Perspective: IMARC’s understanding of Japan’s industrial ecosystem, combined with global benchmarking, ensures that analysis remains both regionally specific and internationally relevant.

Through these strengths, IMARC provides dependable intelligence for organizations evaluating Japan’s autonomous-mobility transformation—supporting evidence-based strategies in one of the world’s fastest-growing transport frontiers.

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

The Japan electric truck market is experiencing transformative growth as the nation accelerates toward sustainable transportation and carbon neutrality. As a leading automotive manufacturing hub, Japan is witnessing unprecedented momentum in commercial vehicle electrification, driven by stringent environmental regulations, technological innovation, and strategic government support. The electric truck industry represents a critical component of Japan's commitment to achieving 100% electrified vehicle sales by 2035 and carbon neutrality by 2050.

An EV charging station represents the necessary main infrastructure that allows electrical energy to be transferred from the power grid into electric vehicles to enable their use for transportation. Unlike conventional fueling stations that offer liquid fuels, EV charging stations provide electric power through the use of standardized connectors and smart control systems. The core components include a power conversion unit, which transforms alternating current from the grid into direct current for the vehicle battery; a charging controller controlling communication between the charger and the EV; and a connector or plug matched to the vehicle's charging interface.

An electric scooter is a two-wheeled vehicle powered by an electric motor and rechargeable battery, aimed at offering the means for efficient, eco-friendly, and cost-effective urban mobility. Apart from the traditional scooters that are powered by internal combustion engines, the electric scooters make use of lithium-ion or lead-acid batteries that feed an electric supply to a BLDC motor, which drives the wheels either directly or via a belt or chain mechanism.

Electric bikes, commonly referred to as e-bikes, are one of the most transformational innovations in modern personal mobility, combining conventional bicycle mechanics with advanced electric propulsion technology. At the heart of e-bikes are an electric motor, a rechargeable battery, and a control system that add assistance to the rider while pedaling, making cycling easier, faster, and more accessible across varied terrains. Based on their design, they can be further categorized into pedal-assist, throttle-controlled, or hybrid models, each providing different levels of rider control and engagement of the motor.

The micro-mobility industry has emerged as a transformative force in urban transportation, revolutionizing how people navigate cities worldwide. According to IMARC, the global micro-mobility market size was valued at USD 63.10 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 204.83 Billion by 2033, exhibiting a CAGR of 12.86% from 2025-2033.

India's electric vehicle (EV) revolution is accelerating at a breakneck speed, powered by a strategic combination of government incentives, infrastructure investments, and manufacturing policies that are transforming the automotive landscape. The IMARC Group forecasts that the Indian electric car market reached USD 963 Million in 2024.

The diesel engine industry is standing at a transformative crossroads. As global markets are pushing for sustainability, stricter emissions compliance, and cutting-edge innovations, diesel powertrains are facing both immense pressure and promising potential.

The global tire market is a multi-billion-dollar industry, driven by the growing demand for vehicles across emerging economies and the replacement tire segment in developed countries. The global tire market is expected to grow at a compound annual growth rate (CAGR) of 4.70% between 2025 and 2033. The industry is heavily influenced by factors such as technological advancements, raw material prices, environmental regulations, and consumer preferences.

Australia's electric vehicle (EV) sector is experiencing swift expansion, fueled by increasing interest in eco-friendly transportation alternatives. In 2024, sales of battery electric and plug-in hybrid vehicles hit an all-time high, totaling around 114,000 units.

The electric bus industry is the part of the transportation sector that deals with the production and installation of buses that run completely or partially on electricity, employing battery packs or fuel cells in place of conventional diesel or gasoline engines. The buses deliver lower greenhouse gas emissions, lesser noise levels, and enhanced energy efficiency, and thus they are a prime solution for environmentally friendly public transport.

India's electric vehicle market is undergoing a profound transformation, impelled by green priorities, economic imperatives, and changing consumer trends. With rising concerns about air pollution and fossil fuel dependence, electric mobility has become a strategic option for India's transport industry. Policy clarity, technology development, and an emerging ecosystem of makers and suppliers are driving this market shift.

The global electric vehicle market size was valued at USD 755 Billion in 2024. The global EV market is rapidly expanding, driven by technological advancements, government incentives, stricter emission regulations, rising fuel costs, extended battery range, growing environmental consciousness, and significant investments in charging and production infrastructure.

Electric Vehicles, or EVs, are vehicles operated partially or wholly by electrical power, generally with rechargeable battery packs as their fuel. In contrast to conventional internal combustion engine cars, EVs emit no tailpipe emissions, making them a cleaner, environmentally friendly transportation choice. EVs comprise Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Hybrid Electric Vehicles (HEVs), and are gaining ground in passenger, commercial, and two-wheeler segments owing to developments in battery technology, charging infrastructure, and policy support.

Aluminum alloy wheels are high-performance, lightweight, and durable components widely used in the automotive industry. Their superior strength-to-weight ratio enhances vehicle efficiency, fuel economy, and handling, making them a preferred choice for both passenger and commercial vehicles. Beyond their functional benefits, aluminum alloy wheels contribute to vehicle aesthetics, offering sleek designs and customization options that appeal to consumers. Their corrosion resistance and thermal conductivity further enhance braking performance and longevity. With increasing demand for fuel-efficient and stylish vehicles, aluminum alloy wheels play a crucial role in the global automotive sector, catering to OEMs, aftermarket suppliers, and performance vehicle manufacturers.

A tyre is a crucial component of a vehicle, serving as the outer covering of a wheel. Its main purposes are to support the vehicle's weight, provide traction for movement, and act as a flexible cushion that absorbs shocks from the road. Usually composed of rubber, tires are strengthened with steel and cloth. Tires for cars, trucks, motorbikes, bicycles, and other vehicles have different designs and compositions depending on the vehicle type and its intended usage. To improve stability and grip, they have a tread pattern on the outside.

Electric kick scooters are small, battery-operated personal transportation vehicles intended for short-distance and urban movement. They offer an economical and environmentally responsible substitute for conventional modes of mobility thanks to their electric engine, rechargeable battery, and lightweight frame. The need for sustainable transportation options, traffic congestion, and growing urbanisation have all contributed to their rise in popularity. Electric kick scooters are now the go-to option for last-mile connectivity and personal commuting because to developments in battery technology, connectivity features, and government programs encouraging micro-mobility.

An automotive wiring harness is an organized assembly of electrical wires, connectors, and terminals that transmit power and signals across a vehicle’s electrical system. It guarantees effective communication between several parts, including the engine control unit, lighting, and sensors. Wiring harnesses are intended to increase vehicle performance and safety by lowering the possibility of short circuits. By maximising electrical connectivity and lowering wire complexity, they are utilised in both conventional and electric automobiles and are essential to contemporary automotive technology.

In an automotive braking system, brake pads are the most important parts since they are engineered to contact the brake rotor to produce friction, thus stopping or slowing down a vehicle in virtually any driving condition safely and efficiently. The key way of classifying these pads is according to their material types: low metallic, ceramic, organic, and semi-metallic.

Tires are essential components of vehicles designed to provide traction, support, and absorb road shocks. Primarily made of rubber, tires consist of treads, belts, and sidewalls that work together to offer grip, stability, and durability. Modern tires come in various types – such as all-season, winter, and performance tires – each engineered for specific driving conditions. The two major tire categories are radial and bias tires, and they are available in different sizes to suit various vehicle types, including passenger cars, light commercial vehicles, medium and heavy commercial vehicles, two-wheelers, and off-road vehicles.

Electric Vehicles (EVs) are powered by electric motors instead of traditional internal combustion engines (ICEs). Electric motors propel EVs by utilizing electricity stored in rechargeable batteries or other energy storage systems. They produce lower or zero tailpipe emissions, reduce air pollution and greenhouse gas (GHG) emissions, and help in mitigating climate change. Electric vehicles consist of various components, such as battery cells and packs, reducers, fuel stacks, power control units, power conditioners, air compressors, humidifiers, motors, on-board chargers, battery management systems, and others. EVs are classified into four types based on propulsion, outlined below.

Saudi Arabia is the second-largest producer and exporter of crude oil and holds the second-largest proven oil reserves in the world, with around 267 billion barrels. The country's oil sector is a significant part of its economy, accounting for 75% of government revenue and approximately 90% of exports. However, due to the volatility of oil prices and the potential for economic instability, Saudi Arabia is increasingly focusing on non-oil activities to reduce its dependency on the oil sector. Non-oil commodities tend to have more stable prices, providing protection against these fluctuations and strengthening the country's social, economic, and financial sectors.