How Big Will the India Medical Devices Industry Be by 2033

Summary:

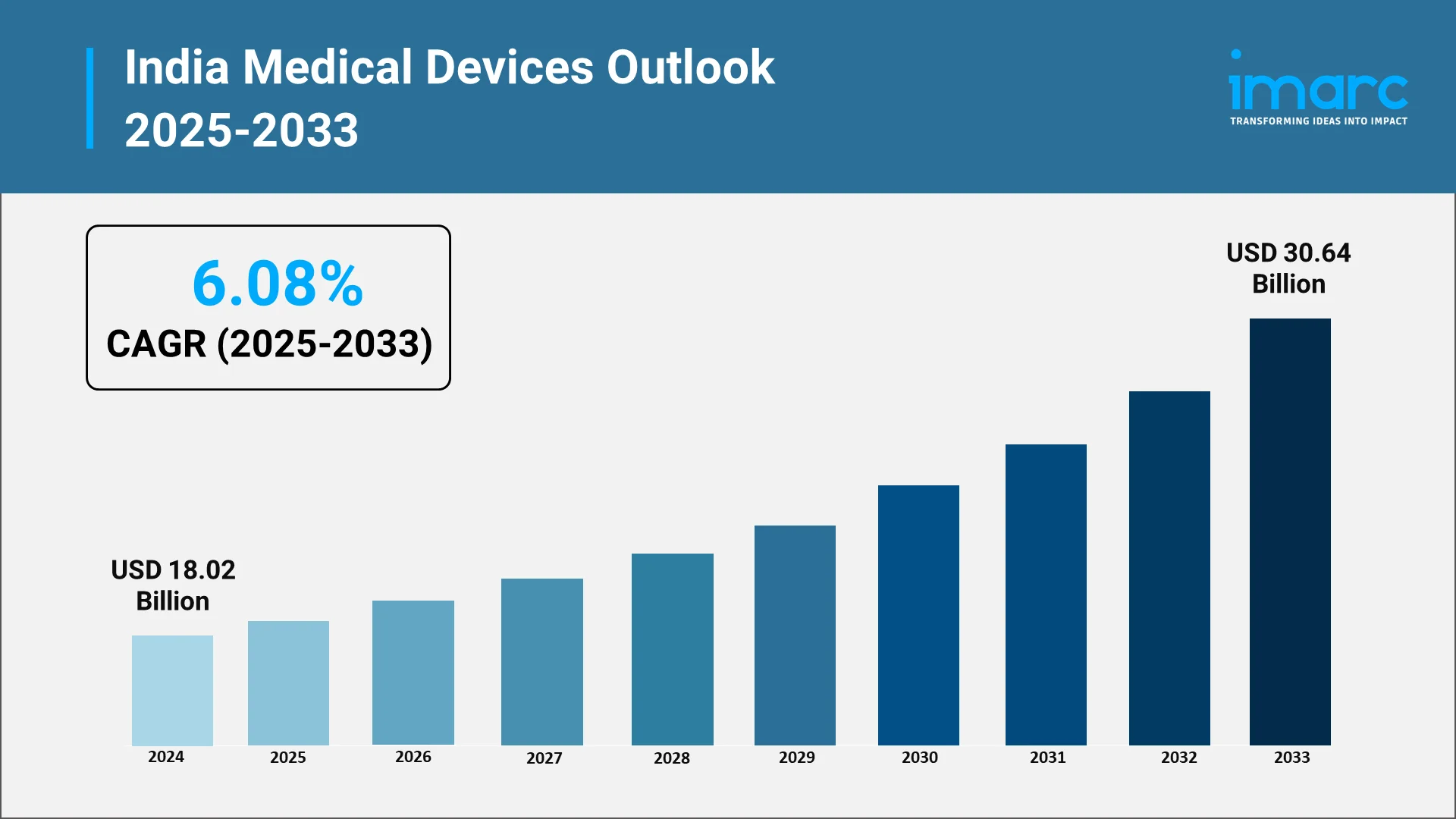

India’s medical devices industry is on a sustained growth trajectory driven by expanding hospital infrastructure, rising chronic disease burden, stronger local manufacturing supported by government incentives, and a rapidly growing shift toward portable and home care devices. Looking forward, the market is expected to reach USD 30.64 Billion by 2033, reflecting the sector’s expanding commercial potential as adoption increases across hospitals, clinics and households. This creates both broad opportunity and niche high-margin spaces for manufacturers, distributors and service providers, particularly those focused on innovation, affordability, and localized production.

Explore in-depth findings for this market, Request Sample

Expansion Of Hospitals Clinics and Diagnostic Labs as The Demand Engine:

India is rapidly broadening its healthcare delivery ecosystem, driven by sustained investments from both public and private players. The expansion of hospitals, specialty centers, diagnostic chains, and primary health facilities is creating a strong and recurring demand cycle for medical devices, ranging from high-value capital equipment to routine consumables and disposables. In fact, according to the Secretary of the Department of Pharmaceuticals, India’s share of domestically produced medical devices has grown from under 10% to around 30% over the past five years. As healthcare access improves across metros, Tier II–III cities, and emerging rural clusters, institutions are increasingly required to modernize infrastructure, adopt advanced diagnostic capabilities, and upgrade patient-care systems, thereby strengthening the long-term outlook for domestic and global device manufacturers.

A major demand catalyst is the significant scale-up of hospital capacity nationwide. As institutions add intensive care unit beds, upgrade operation theatres, and enhance diagnostic laboratory capabilities, they require a wide spectrum of equipment including patient monitoring devices, anesthesia systems, ventilators, imaging platforms, and surgical tools. Parallel to this, India is witnessing strong momentum in diagnostics-led care models. The growing use of multimodality systems such as MRI, CT, and PET-CT, complemented by rising adoption of point-of-care testing, is expanding demand for both large, sophisticated imaging platforms and compact diagnostic systems suitable for high-throughput environments.

Additionally, the rapid expansion of private hospital groups, diagnostic chains, and franchised networks is altering procurement dynamics. According to reports, India’s hospital sector attracted US$4.96 billion in private-equity funding, driven largely by big chains like Manipal, Apollo, and Fortis, signaling strong investor confidence in scalable, organized healthcare delivery . Organized players prefer structured, large-scale procurement that shortens the sales cycle for reliable suppliers and supports predictable order volumes. This shift is also transforming purchasing behavior: instead of one-time capital buys, institutions are opting for lifecycle contracts that bundle installation, maintenance, service, and consumables. Such models enhance revenue visibility for manufacturers, strengthen long-term customer relationships, and benefit companies capable of delivering integrated device-plus-service solutions. As this transformation accelerates, India’s healthcare expansion will continue to drive robust, multi-segment demand for medical devices across the value chain.

Market Size and Growth Opportunity:

The India medical devices market size reached USD 18.02 Billion in 2024, exhibiting a growth rate (CAGR) of 6.08% during 2025–2033. India’s medical devices market is expanding rapidly, with major industry estimates showing minor variations due to differences in methodology and segment definitions. Key factors propelling this growth include the increasing prevalence of chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions, which are driving demand for diagnostic and therapeutic devices. Additionally, the government’s strategic initiatives, including Production Linked Incentive (PLI) schemes for medical devices, the establishment of medical device parks, and support for research and innovation, are encouraging local manufacturing and reducing reliance on imports. Rising awareness among consumers, the growth of private healthcare infrastructure, and the adoption of advanced technologies such as digital health monitoring and portable diagnostic devices are further expanding market opportunities. The combined effect of these factors positions India as one of the fastest-growing medical device markets globally, attracting both domestic and international investment and fostering innovation across multiple segments.

For strategic planning, companies typically model three scenarios: a base case with steady growth and moderate localisation, an upside case with stronger localisation backed by government investment and export gains, and a downside case reflecting weaker hospital spending or supply-chain challenges. Firms focusing on portable and home-care devices can expect faster-than-average growth given the rapid expansion of remote monitoring and home-based healthcare.

Dependence on Imports Along with Rising Domestic Manufacturing:

India has traditionally relied heavily on imports for high-sophistication medical devices such as advanced imaging systems, implants, high-end diagnostics, and specialized therapeutic equipment. This dependence exposes the healthcare sector to multiple risks. Foreign exchange volatility, fluctuations in global commodity prices, tariff revisions, and geopolitical disruptions can all influence the landed cost and availability of these critical devices. During periods of global supply chain stress, this vulnerability becomes even more evident, leading to delays, price spikes, and procurement challenges for hospitals and diagnostic networks. According to reports, between FY2020-21 and FY2024-25, India spent more than USD 25 billion on imported electromedical equipment (such as ventilators and diagnostic imaging systems) and surgical instruments. At the same time, the import-heavy landscape presents a substantial opportunity for domestic manufacturers to strengthen their presence, particularly in low- and mid-complexity product categories where technological barriers are lower and demand is consistently growing.

In recent years, a strong policy push has accelerated the shift toward localisation. Government initiatives such as the Production Linked Incentive (PLI) Scheme, the creation of medical device parks, and easier regulatory pathways for domestic innovators have encouraged both local firms and multinational corporations to increase manufacturing within India. Global companies are also expanding their footprint by setting up assembly lines, component manufacturing units, and R&D centers to serve India as well as export markets. This environment opens up multiple avenues for domestic industry growth—not only in the manufacturing of mid-complexity devices but also in component production, contract manufacturing for international brands, and the provision of aftermarket services such as maintenance, calibration, and consumables supply. These segments typically offer attractive margins, recurring revenue streams, and long-term customer relationships, making them key drivers of India’s evolving medical devices ecosystem.

Shift Toward Portable and Home Care Medical Equipment:

One of the most significant structural transformations in India’s medical devices landscape is the rapid rise in adoption of portable and home care equipment. Devices such as digital oximeters, blood pressure monitors, glucometers, portable ECG systems, remote monitoring kits, and various home therapy solutions including portable suction units, CPAP machines, and mobility aids are becoming integral to patient care beyond clinical settings. This shift reflects the growing preference for decentralized healthcare, where individuals increasingly manage routine monitoring and treatment from the comfort of their homes. For instance, Japan’s Omron is aggressively expanding in India, building its first manufacturing plant in Chennai to make blood pressure monitors and ECG devices more affordable and accessible for home use — partly because BP-monitor penetration remains low (around ~6%) despite high hypertension prevalence. As awareness of preventive health rises and digital literacy improves, home-based devices are steadily moving from niche products to mainstream essentials.

Multiple factors are fueling this movement toward portable and home care technologies. The growing burden of chronic illnesses such as diabetes, hypertension, and cardiovascular disorders requires frequent monitoring outside hospital environments. At the same time, India’s expanding elderly population is driving demand for solutions that support aging in place and reduce the dependence on caregivers. Telemedicine has also witnessed sharp adoption, and validated home measurements have become indispensable for virtual consultations and remote care models. Advances in technology including more affordable sensors, improved battery performance, compact device design, and seamless smartphone connectivity have further enhanced usability and accessibility, encouraging wider adoption across diverse population segments.

Market research consistently indicates that the home healthcare monitoring category is expanding much faster than the overall medical devices industry. The segment’s strong outlook highlights significant opportunities for companies focused on consumer health tools and clinically validated home care devices. Businesses that strengthen partnerships with pharmacy networks, direct to consumer channels, e-commerce platforms, and telehealth providers will be better positioned to capture a larger share of the growing demand. This strategic alignment not only increases market reach but also supports sustainable long term growth as home-based care becomes a core pillar of India’s healthcare system.

Government Support Through PLI Device Parks and Incentives:

The Government of India is prioritizing the expansion of domestic medical device manufacturing, supported by initiatives such as the Production Linked Incentive (PLI) scheme. The PLI program provides financial rewards for incremental sales of approved products, encouraging new projects and greenfield investments. Updated guidelines and approved beneficiary lists released through 2023 and 2024 have broadened both the eligible device categories and the number of participating companies. By March 2023, 21 companies had been approved under the PLI scheme to manufacture medical devices across four target segments such as imaging, cardio-respiratory devices, implants, and cancer-care equipment. Moreover, 50 new greenfield plants are expected to be established over the next two years under the pharma-and-medical-device PLI scheme, according to the Department of Pharmaceuticals.

Alongside the PLI scheme, central and state governments are developing medical device parks, offering capital subsidies, and implementing dedicated manufacturing policies to build a stronger ecosystem. These initiatives provide manufacturers with access to testing labs, shared infrastructure, and regulatory support. For businesses, incorporating these incentives into project planning is crucial, as they can significantly improve returns, shape capital expenditure decisions, shorten break-even timelines, and enhance export strategies.

.webp)

Competitive Landscape and Leading Companies:

India’s medical devices market features a strong mix of multinational corporations and established domestic manufacturers, each contributing differently across product categories and technology tiers.

GE Healthcare remains one of the most influential global players, with a deep portfolio in imaging, diagnostics, patient monitoring and ultrasound systems. The company has expanded its manufacturing and R&D footprint in India through joint ventures and local partnerships, enabling faster product customization, competitive pricing and adherence to government localisation norms.

Siemens Healthineers holds a similarly strong position in advanced imaging, laboratory diagnostics and digital health platforms. Its emphasis on precision diagnostics, automation and AI-driven imaging solutions aligns well with India’s fast-modernizing tertiary hospitals. Supporting this, in April 2023, Siemens inaugurated an MRI manufacturing facility in Bengaluru to locally produce its MAGNETOM Free.Star (helium-free) scanner, under India’s PLI scheme . Continuous investments in local training centers and manufacturing expansion further strengthen its competitive edge.

Philips Healthcare is another dominant multinational, known for imaging, critical care monitoring, respiratory devices and home-health technologies. Philips has focused heavily on integrated care and telehealth in India, leveraging its global expertise to address the country’s growing demand for connected care solutions.

Mindray, a major Chinese manufacturer, has rapidly gained market share in patient monitoring, anaesthesia machines, ventilators and ultrasound devices by offering technologically strong products at competitive price points. Its expanding distribution network and service infrastructure have helped it penetrate both public and private healthcare sectors.

On the domestic front, Trivitron Healthcare stands out as one of India’s most diversified medical device manufacturers, with strengths in diagnostics, imaging, in vitro diagnostics (IVD), radiation protection and critical-care equipment. The company has expanded through strategic acquisitions and overseas manufacturing facilities, helping it compete in both domestic and export markets.

BPL Medical Technologies remains a key Indian brand in patient monitoring, ECG machines, defibrillators and home-health equipment. Its strong brand recall, cost-effective product range and distribution reach allow it to compete effectively in value-driven segments. Several other Indian companies specializing in consumables, disposables and mid-complexity devices are scaling rapidly through technology partnerships, OEM manufacturing and product innovation.

Overall, multinational corporations continue to dominate high-end capital equipment, while domestic players excel in consumables, monitoring devices and price-sensitive categories. With global firms expanding local manufacturing and Indian companies investing in R&D and international acquisitions, competition is intensifying, signalling a more mature and innovation-driven market ahead.

Choose IMARC Group for Unmatched Expertise in Medical Devices:

IMARC Group empowers healthcare leaders with precise, actionable insights to navigate India’s dynamic medical devices market. We provide data-driven market research, delivering comprehensive market sizing, trend analysis, and competitive benchmarking to support evidence-based decisions. Through strategic growth forecasting and scenario modeling, we help companies plan for multiple outcomes, reducing risk and enabling informed long-term strategies.

Our policy and infrastructure advisory guides businesses in leveraging government initiatives, such as PLI schemes and medical device parks, to optimize investment and production planning. IMARC also offers custom reports and consulting, tailored to market entry, localization, and expansion strategies, ensuring solutions fit each client’s specific goals.

We deliver deep insights across domestic manufacturing, home care devices, diagnostics, and high-end capital equipment, helping firms identify high-growth, profitable segments. Additionally, we provide guidance on investment planning, export strategies, and operational efficiency to maximize returns.

By combining global expertise with local market knowledge, IMARC enables clients to capture emerging opportunities and gain a competitive edge. Our focus on innovation, sustainable growth, and long-term advantage ensures that businesses not only keep pace with the evolving medical devices ecosystem but also lead it, driving success in India’s fast-growing healthcare market.

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

Pectin represents a naturally occurring polysaccharide mainly extracted from cell walls of fruits (mainly from citrus peel and apple pomace). It is a soluble dietary fiber and a hydrocolloid with gelling, thickening, and stabilizing properties. It is mostly composed of galacturonic acid units.

Paracetamol, also referred to as acetaminophen, is an analgesic and antipyretic compound that is commonly used worldwide for the treatment of mild to moderate pain and the management of fever. The mechanism of action occurs mainly in the central nervous system, where it inhibits the mechanisms that regulate pain and body temperature, but lacks anti-inflammatory properties.

The Australia wellness tourism industry has emerged as a critical segment of the country’s broader travel and hospitality sector. It reflects a growing global emphasis on health, self-care, and holistic well-being, capturing the attention of travelers seeking experiences that combine relaxation, rejuvenation, and personal growth.

The Brazil cardiovascular devices market represents a crucial segment in the country’s healthcare ecosystem, addressing one of the leading causes of morbidity and mortality: cardiovascular diseases. Conditions such as heart attacks, stroke, arrhythmias, and heart failure require ongoing medical intervention and advanced heart disease treatment solutions. With the rising prevalence of cardiovascular disorders, demand for comprehensive cardiac care equipment and innovative treatment modalities is increasing.

India's Ayurvedic products market is experiencing remarkable transformation as consumers increasingly prioritize holistic wellness and natural remedies over conventional alternatives. The convergence of traditional healing wisdom with modern consumer preferences has created a dynamic landscape where herbal medicines, chemical-free personal care products, and immunity-boosting supplements are becoming household staples.

Nicotine pouches are small, smokeless oral delivery products of nicotine, free from tobacco, designed to allow for controlled release of the active principle without burning, vaporizing, or use of traditional tobacco leaves. It consists of a small pouch that contains a matrix made basically from plant fibers, flavorings, pH adjusters, and stabilizers impregnated with nicotine, encased in a permeable material permitting the gradual absorption of the product via the oral mucosa.

The pharmaceutical industry in Japan is among the most advanced globally, recognized for combining innovation, high-quality standards, and patient-centered care. Its extensive value chain includes drug discovery, clinical trials, manufacturing, distribution, marketing, and post-market surveillance. Serving both domestic and international markets, Japanese pharmaceutical companies are respected for regulatory compliance, safety, and reliability, establishing them as trusted global collaborators in drug development.

The pharmaceutical industry in Japan is among the most advanced globally, recognized for combining innovation, high-quality standards, and patient-centered care. Its extensive value chain includes drug discovery, clinical trials, manufacturing, distribution, marketing, and post-market surveillance. Serving both domestic and international markets, Japanese pharmaceutical companies are respected for regulatory compliance, safety, and reliability, establishing them as trusted global collaborators in drug development.

The global healthcare IT industry is on a remarkable upswing, fueled by the surge in preventive care, digital health platforms, and smarter patient management systems. According to IMARC Group, the market hit USD 363.15 Billion in 2024, a clear sign of worldwide adoption. An aging population, the growing comfort with remote care, and the push toward personalized medicine are all speeding this momentum.

The global endoscopy devices market is on a sharp growth path, fueled by the shift toward minimally invasive procedures, the need for early diagnosis, and cutting-edge imaging technologies. IMARC Group reported the market hit USD 50.01 Billion in 2024, underscoring its worldwide acceptance.

The global business-to-business (B2B) payments landscape is experiencing a fundamental transformation that is reshaping how enterprises conduct financial transactions across borders and industries. The market, valued at approximately 1,189.6 Billion in 2024, is projecting remarkable growth with expectations to reach USD 2,189.0 Billion by 2033, exhibiting a CAGR of 7% from 2025-2033. This exponential expansion is signaling a paradigm shift in commercial finance, driven by technological innovation, changing business expectations, and the urgent need for more efficient payment infrastructures.

The smart medical devices market is entering a decade defined by connected care, real-time diagnostics, and patient empowerment. Valued at USD 45.9 Billion in 2024, the market is projected to reach USD 82 Billion by 2033, expanding at a compound annual growth rate (CAGR) of 6.33% between 2025 and 2033 by IMARC Group. This steady rise reflects growing confidence in data-driven healthcare systems, integration of IoT in medical environments, and the increasing role of artificial intelligence in clinical decision-making.

Active Pharmaceutical Ingredients (APIs) are the bioactive molecules of any drug used in pharmaceuticals, which cause the desired therapeutic action in the body of a human being. APIs are the central core of all drugs, chemical or biological and are responsible for the efficacy, strength, and safety of the drug. APIs are synthesized by various complex chemical synthesis, fermentation, biotechnological, or extraction processes based on the type of drug.

A bio medical incinerator is a high-temperature combustion system specialized for biomedical waste disposal by hospitals, clinics, laboratories, and research institutions. Biomedical waste usually consists of infectious waste, pathological waste, sharps, pharmaceuticals, and contaminated disposables that are very hazardous to human health and the environment if not treated.

Obesity, once viewed primarily as a lifestyle choice, is now widely recognized as a complex and chronic disease characterized by excessive body fat accumulation. Its global prevalence is escalating at an alarming rate posing a significant and growing challenge to public health systems worldwide.

Gonorrhea, a sexually transmitted infection caused by the bacterium Neisseria gonorrhoeae, is a major public health issue globally. Reports show that over one million new cases of curable STIs are contracted every day by individuals aged 15 to 49 years, with the majority being asymptomatic.

The 7 major allergic conjunctivitis markets reached a value of USD 2.1 Billion in 2024. Looking forward, IMARC Group expects the 7MM to reach USD 2.9 Billion by 2035, exhibiting a growth rate (CAGR) of 3.00% during 2025-2035.

The healthcare sector is changing rapidly because of the growing demand for better ways to manage chronic diseases. As we move toward 2025 and beyond, digital tools are playing an important role in dealing with conditions like diabetes, heart disease, cancer, and respiratory problems.

The global multivitamin gummies market consists of chewable dietary supplements that are charged with key vitamins and minerals aimed at maintaining general health and wellness. The gummies present a handy, enjoyable, and easy-to-swallow option to classic pills or tablets, hence are predominantly preferred by children and adults who do not like taking pills.

India's pharmaceutical sector is evolving rapidly, supported by the integration of artificial intelligence (AI) across the value chain. As of 2023, India ranked as the third-largest pharmaceutical producer by volume, accounting for 20% of global generic drug exports.

As Lung Cancer Awareness continues to build global momentum in 2025, Artificial Intelligence (AI) is proving to be a transformative force—not only in clinical diagnostics but also in public education and preventive health efforts. Given that lung cancer remains one of the world’s deadliest cancers, accounting for over 1.8 million deaths each year and a five-year survival rate of just 28.4%, the integration of AI marks a critical turning point.

Observed on May 19, Hepatitis Testing Day 2025 emphasizes the need to "Test. Treat. Eliminate," highlighting the gap in diagnosing hepatitis B and C, which cause over 1.3 million deaths annually. Hepatitis remains a major global health threat, on par with HIV, tuberculosis, and malaria. The growing viral hepatitis market <Viral Hepatitis Market Size | Share, Trends - 2034 > reflects rising demand for better diagnostics, treatments, and integrated care. The WHO warns that without faster testing and treatment, the goal of eliminating hepatitis by 2030 may not be achieved, with disparities in diagnostics, particularly in low- and middle-income countries, hindering progress.

Observed on May 8, World Ovarian Cancer Day 2025 carries the theme “No Woman Left Behind,” reinforcing the urgent need to close the gaps in access, diagnosis, treatment, and care across all regions and socioeconomic groups. Ovarian cancer remains one of the deadliest gynecological cancers, often detected too late due to vague symptoms and limited screening tools. The World Ovarian Cancer Coalition projects a 55% rise in annual cases and nearly 70% more deaths by 2050, with the heaviest burden falling on low- and middle-income countries. Equitable access to early diagnostics, genetic testing, and targeted therapies is critical.

In clinics around the world, a concerning pattern is becoming increasingly evident: a growing number of patients are experiencing wheezing, breathlessness, and persistent coughing. This surge reflects a broader global trend. According to the World Health Organization (WHO), more than 260 million people are currently living with asthma, making it one of the most widespread and persistent chronic respiratory conditions globally.

Observed on April 25, World Malaria Day 2025 carries the theme “Accelerating Equity in Malaria Prevention and Cure,” underscoring the urgent need to reach communities still lacking access to life-saving vaccines and diagnostics. While global malaria death rates have seen modest declines, the disease continues to claim the life of one child every minute, highlighting the critical need for swift, equity-driven action

Sulfamethoxazole is a common synthetic antibacterial that is a member of the sulfonamide class of antibiotics. This substance plays a very significant role in modern medicine due to the amazing capabilities offered by the substance for curing infections and bacterial diseases. Trimethoprim and sulfamethoxazole are frequently used together to create the well-known antibiotic co-trimoxazole, which is well-known for its potency against a variety of bacterial infections. It works by preventing the manufacture of folic acid, which is necessary for the growth of bacteria. Sulfamethoxazole is an essential part of modern antibiotic therapy since it has been used to treat lung infections, urinary tract infections, and other common bacterial illnesses.

Healthcare consumables are necessary medical supplies used for patient treatment, diagnostics, and cleanliness in clinics, hospitals, and home care settings. These consist of supplies such as surgical masks, bandages, gloves, syringes, catheters, and disinfectants. Usually, they are disposable or single use to preserve sterility and stop infections. Healthcare consumables are an essential component of the global healthcare ecosystem and are in high demand due to expanding healthcare needs, an increase in operations, infection control measures, and technological improvements.

Catheters are flexible, tubular medical devices designed to access various body cavities, organs, or blood vessels for diagnostic or therapeutic purposes. They can be broadly classified into types based on their application, including urinary catheters, cardiac catheters, and intravenous (IV) catheters. Catheters are commonly used in diverse healthcare settings for managing chronic conditions, enabling fluid drainage, delivering medications, or facilitating minimally invasive surgeries.

Bioinformatics involves applying computational techniques and tools to study and understand biological systems at the molecular level. It is a field of study that combines mathematics, biology, computer science, and statistics to research genomic data and biological networks. The goal is to interpret information from large biological data sets, such as DNA sequences, protein structures, gene expressions, and other high-throughput experimental data. This field provides various products and services, such as knowledge management tools, bioinformatics platforms, and services.

A non-animal model refers to an experimental system or method used in scientific research or testing that does not involve the use of animals. These models are developed to simulate biological processes, test hypotheses, or study diseases without the need for live animals. The aim is often to reduce the reliance on animal testing, which has ethical implications and raises concerns about animal welfare.

Cell therapy involves the transplantation and manipulation of living cells to replace and repair damaged tissue. Its primary branches include stem cell therapy and non-stem cell therapy. Stem cell therapy utilizes stem cells to repair, replace, or rejuvenate damaged or diseased cells and tissues as they possess the ability to differentiate into various specialized cell types, making them valuable for regenerative medicine. Non-stem cell-based therapies typically involve somatic cells isolated from the human body. These cells are propagated, expanded, selected, and then administered to patients for curative, preventive, or diagnostic purposes. On the other hand, gene therapy seeks to treat diseases by introducing, replacing, or inactivating genes within cells.