How Big will the Japan Warehouse Robotics Market be by 2033

Introduction to the Japan Warehouse Robotics Market:

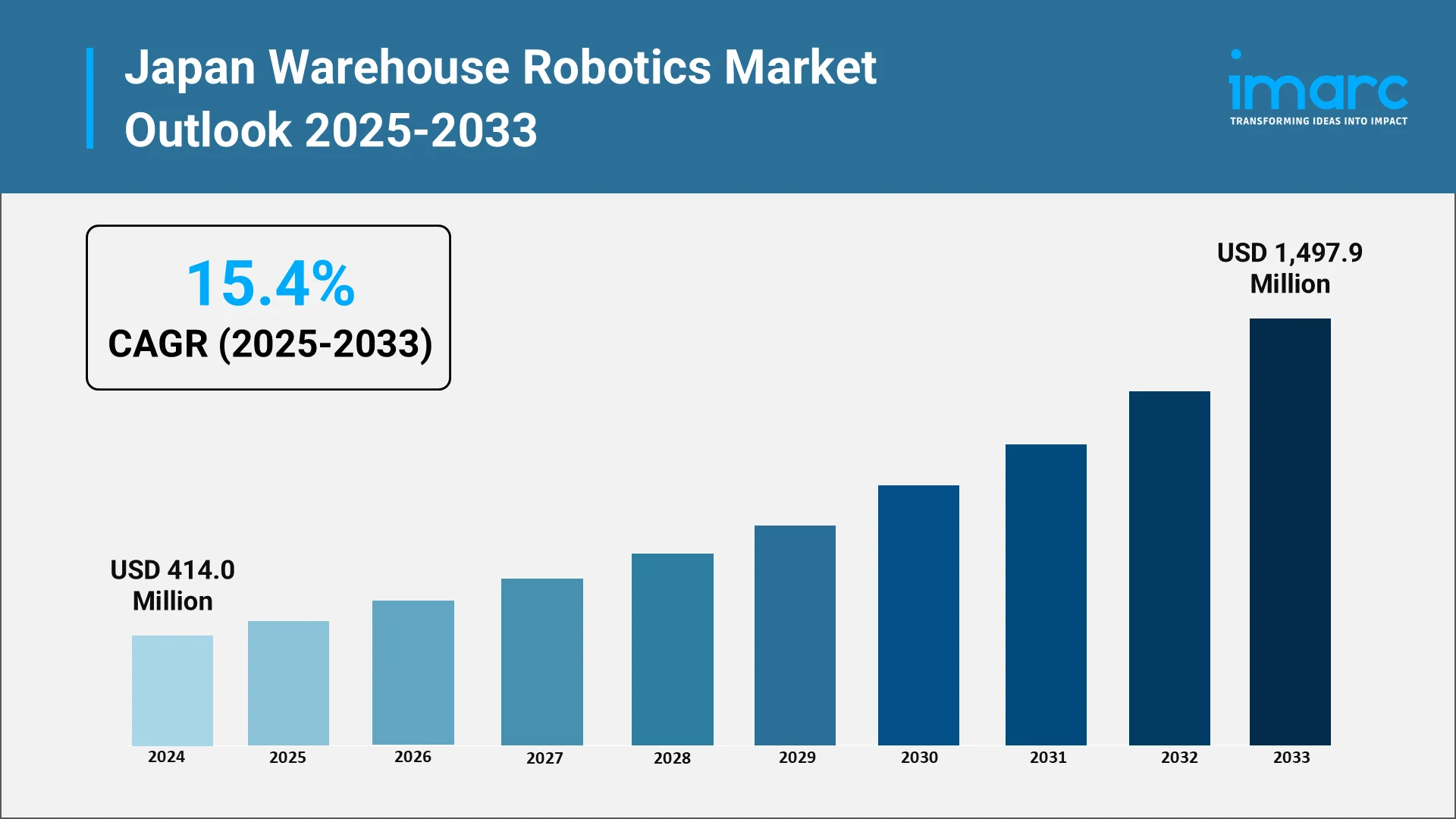

The Japan warehouse robotics market is a highly dynamic and rapidly expanding segment of the global automation industry. The market, valued at USD 414.0 Million in 2024, is on a sharp growth trajectory. Its growth is fueled by critical domestic factors, including a severe labor shortage, the rapid expansion of e-commerce, and Japan's strategic position as a world-leading robotics manufacturer. This exceptional growth is underpinned by Japan's unique demographic challenge: an aging population (over 28% of the total population is over 65) and a declining workforce. This creates an urgent need for automation across all sectors, especially logistics. Simultaneously, Japan e-commerce market is booming, valued at USD 258.0 Billion in 2024 and projected to grow to USD 692.8 Billion by 2033 (a CAGR of 11.02%). This digital shift demands the precision and speed that only advanced robotic solutions can provide.

Explore in-depth findings for this market, Request Sample

Japan is exceptionally positioned to capitalize on this demand, as it is the world's leading robot manufacturing country, producing 46% of industrial robots globally. This confluence of technological strength, a pressing need for operational efficiency, and strong government backing positions the Japan warehouse robotics market as a critical component of the nation's economic future.

Current Market Landscape and Adoption Trends:

The current Japanese warehouse robotics landscape is defined by technological innovation, diverse solutions, and accelerating adoption across sectors. The market utilizes a comprehensive range of systems, including automated guided vehicles (AGVs), autonomous mobile robots (AMRs), robotic arms, and specialized picking and sorting systems—all designed to replace manual labor and enhance operational efficiency.

The competitive landscape is robust, featuring both global powerhouses and domestic leaders. Japanese heavyweights include Fanuc and Yaskawa, two of the Big 4 industrial robot manufacturers worldwide. They compete alongside major international players like ABB Ltd., KUKA AG, and Omron Corporation, alongside Japanese firms such as Daifuku Co. Ltd. and Kawasaki Heavy Industries, which drives continuous innovation.

Adoption trends show strong momentum led by e-commerce and third-party logistics providers, but also by the automotive, electronics, and pharmaceutical sectors. The cold chain logistics segment is an increasingly high-value application, as robotic systems address the difficulties of operating in temperature-controlled environments, reducing human exposure to harsh conditions.

Recent market activity highlights accelerating innovation and strategic partnerships. For example, in July 2024, Sumitomo Corporation and Dexterity Inc. formed a new joint venture, Dexterity-SC Japan, focusing on AI-powered intelligent robotic solutions for logistics. Furthermore, the e-commerce drive is evident with Ocado Group and AEON's plan to construct a third Customer Fulfilment Centre (CFC) in Saitama Prefecture by 2027, following earlier launches in Chiba and Hachioji. These expansions demonstrate a commitment to using advanced automation to meet fast-delivery consumer expectations.

Market segmentation shows that while AGVs remain dominant for structured material handling, AMRs are rapidly gaining traction due to their flexibility and adaptability in dynamic warehouse environments. This adoption is being driven by the integration of artificial intelligence (AI), machine learning, and Internet of Things (IoT) capabilities, enabling sophisticated autonomous navigation and real-time operational monitoring.

Key Factors Driving Growth in Warehouse Robotics:

The market's significant growth is propelled by powerful, mutually reinforcing economic and structural factors:

- E-Commerce Expansion and Fulfilment Demands

The massive growth of Japan's e-commerce sector creates complex fulfilment challenges. The need to process vast numbers of small, diverse orders with high speed and accuracy is pushing demand for intelligent robots capable of item recognition, real-time sorting, and autonomous movement. This demand is further intensified by the shift toward mobile commerce, which accounts for over 50% of all e-commerce transactions.

- Demographic Challenges and Workforce Transformation

Japan's aging population reduces the available workforce while simultaneously increasing labor costs, strengthening the economic case for automation. Robotics solutions allow companies to maintain operational efficiency and competitiveness despite the demographic constraints and the difficulty in finding skilled staff for logistics roles.

- Industry 4.0 Integration and Technological Advancement

The adoption of Industry 4.0 technologies, including AI, machine learning, and advanced sensor and vision systems, has dramatically improved the capabilities and cost-effectiveness of warehouse robotics. These innovations enable robots to perform more complex tasks and integrate seamlessly with existing warehouse management systems (WMS).

- Cold Chain and Temperature-Sensitive Logistics

The increasing demand for temperature-sensitive products, such as pharmaceuticals and fresh food, has created a specialized need for highly efficient robotic systems in cold storage. Automation is often a more viable solution than human labor in these demanding, freezing environments, delivering both operational and safety benefits.

- Cost Efficiency and Return on Investment

The economic value proposition is strengthening as robotics technology costs decline while labor costs rise. Robotic systems enable warehouse operations to be more flexible, require less space per volume of goods, reduce product damage, and lower long-term operating expenses, ensuring a strong Return on Investment (ROI).

Government Support and Technological Advancements:

Japan's technological advantage is strongly supported by comprehensive government policy and a world-class R&D infrastructure.

- Government Policies and Strategic Initiatives

The Japanese government actively promotes robotics adoption through strategic programs. The "New Robot Strategy" (2016-2020) and the Robotics for Social Transformation Promotion Plan (2019) aim to use robot technology to solve social issues—specifically the labor crisis—and achieve a sustainable economy. These initiatives position robotics as a core technology for the government's Society 5.0 vision, which seeks a technology-enabled social transformation.

- Financial Support and Investment Programs

Substantial public funds are committed to robotics R&D and deployment. Key investments include hundreds of millions of dollars appropriated for robotics-related projects across manufacturing, nursing, and infrastructure. Furthermore, the government focuses support on creating a "robot-friendly" environment in key sectors like logistics warehouses, offering various national and local support systems to reduce barriers to adoption.

- Technological Innovation and Breakthroughs

Japan's leadership in robotics is driving continuous innovation. Advancements in articulated arms, AMRs, and AGVs for heavy tasks are increasing demand. The integration of advanced sensors, machine learning, and AI has fundamentally improved robot performance, enabling greater precision and reliability. Furthermore, new business models like Robot-as-a-Service (RaaS) are gaining traction, allowing businesses to reduce capital costs and increase accessibility to advanced automation.

- Regulatory Framework and Standards Development

Japan maintains a progressive regulatory environment. A New International Standard for the Safe Operation of Service Robots, originating from a Japanese proposal, was issued in November 2023, and automated delivery robots began operating on public roads in April 2023. This proactive stance on establishing global standards for robotics ensures rapid deployment and commercialization.

.webp)

Market Size Forecast and Projections to 2033:

The Japan warehouse robotics market is set for exceptional, sustainable growth, driven by deep structural factors and continuous technological advancement.

- Market Size and Growth Trajectory

Projections indicate the Japan warehouse robotics market is anticipated to reflect a compound annual growth rate (CAGR) of 15.4% during the forecast period (2025-2033). This strong momentum is projected to continue, with the market reaching will reach USD 1,497.9 Million in fiscal year 2033. This strong consensus among independent market analyses reinforces the long-term confidence in the market's expansion.

- Segment-Specific Growth Projections

Growth is not uniform across all technologies:

- The autonomous mobile robots (AMRs) segment is a key growth driver, holding a significant market share in 2024. Their flexibility and AI-based navigation make them ideal for dynamic, high-speed e-commerce fulfilment environments.

- Automated guided vehicles (AGVs) also show substantial growth globally, reflecting their continued importance in high-volume, fixed-route material handling in large-scale warehouses and manufacturing facilities.

- Integration with Broader Logistics Automation

Warehouse robotics growth is part of a larger, systemic change in Japan's logistics sector. The overall logistics automation market size in Japan was USD 5 Billion in 2024 and is expected to reach USD 17.6 Billion by 2033 (15.1% growth rate). This comprehensive automation encompasses robotics, WMS, and supply chain integration platforms, working together to deliver end-to-end operational improvements.

Future Opportunities and Strategic Outlook:

The long-term outlook for the Japan warehouse robotics market is highly positive, driven by several key future opportunities:

- Emerging Technology Integration Opportunities

The ongoing integration of AI and machine learning will drive the next wave of innovation, enabling sophisticated automation capabilities like adaptive task allocation and predictive maintenance. This advancement will be further enhanced by the widespread use of collaborative robots (cobots) for precision tasks alongside human workers.

- Business Model Innovation and Service Delivery

The increased adoption of the robot-as-a-service (RaaS) model is a critical opportunity. By reducing significant upfront capital costs, RaaS increases accessibility for small and medium-sized enterprises, substantially expanding the addressable market and accelerating overall adoption rates.

- Cold Chain and Specialized Logistics Expansion

The temperature-controlled logistics segment, particularly for pharmaceuticals and fresh food, will be a high-growth area. The stringent requirements for precision, traceability, and reliability in these segments align perfectly with advanced robotics capabilities, creating a high-value, defensible market niche.

- E-Commerce Fulfilment Center Transformation

The continuous construction and technological upgrades of large-scale automated fulfilment centers, such as those planned by AEON and Ocado, will serve as powerful demonstration effects, validating the economic and operational benefits of robotics and accelerating broader market adoption across the entire logistics sector.

- Sustainability and Environmental Performance

Warehouse robotics contributes to corporate sustainability goals. Robotic warehouses use less space per volume of goods, reduce energy consumption, and limit product damage. This alignment with environmental performance targets provides an additional, compelling value proposition for investment.

The long-term outlook remains exceptionally positive. The convergence of demographic imperatives, e-commerce growth, and sustained government support creates a multi-decade opportunity. The transformation of Japanese logistics through warehouse robotics is not just a technological change; it is a fundamental reimagining of the supply chain, positioning the country as a global exemplar for advanced automation.

Choose IMARC Group to Automate Your Success in the Japan Warehouse Robotics Market—We Offer Unmatched Expertise and Core Services:

- Data-Driven Market Research: Deepen your knowledge of the market size, growth drivers (e-commerce surge, aging workforce), and technological adoption across key segments like Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), and Automated Storage and Retrieval Systems (AS/RS).

- Strategic Growth Forecasting: Predict emerging trends in logistics automation, from the proliferation of 'Robot-as-a-Service (RaaS)' and AI-driven picking systems to the integration of robotics within cold chain logistics and cross-border fulfilment centers.

- Competitive Benchmarking: Analyze the competitive landscape, review the product pipelines of local giants (Fanuc, Yaskawa, Daifuku), and monitor breakthroughs in human-robot collaboration (Cobots) and vision-guided robotics tailored for high-mix, low-volume Japanese operations.

- Policy and Infrastructure Advisory: Stay one step ahead of government incentives (Industry 4.0/Society 5.0), local regulatory paradigms, and the required capital expenditure for next-generation warehouse build-outs and retrofitting existing facilities.

- Custom Reports and Consulting: Get tailored insights geared to your organizational objectives—be it market entry strategy, identifying potential M&A targets among domestic technology providers, or optimizing your supply chain's response to Japan's relentless fulfillment speed expectations.

For more details, click: https://www.imarcgroup.com/japan-power-electronics-market

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

The UK is rapidly evolving into a dynamic hub for autonomous vehicle research, testing, and early-stage deployments. A strong ecosystem comprising academic institutions, technology start-ups, automakers, and mobility service providers fosters continuous innovation. Supported by a skilled workforce specializing in software, sensing, robotics, and transportation systems, the nation has become a fertile ground for experimentation.

Japan’s transportation landscape is on the brink of a major shift, with robo taxis, autonomous, driverless vehicles designed for passenger and goods transport, emerging as a practical mobility solution. The Japan robo taxi market reached USD 83.2 Million in 2024 . This remarkable expansion reflects Japan’s broader move toward smart mobility, sustainability, and automation.

The Japan electric truck market is experiencing transformative growth as the nation accelerates toward sustainable transportation and carbon neutrality. As a leading automotive manufacturing hub, Japan is witnessing unprecedented momentum in commercial vehicle electrification, driven by stringent environmental regulations, technological innovation, and strategic government support. The electric truck industry represents a critical component of Japan's commitment to achieving 100% electrified vehicle sales by 2035 and carbon neutrality by 2050.

An EV charging station represents the necessary main infrastructure that allows electrical energy to be transferred from the power grid into electric vehicles to enable their use for transportation. Unlike conventional fueling stations that offer liquid fuels, EV charging stations provide electric power through the use of standardized connectors and smart control systems. The core components include a power conversion unit, which transforms alternating current from the grid into direct current for the vehicle battery; a charging controller controlling communication between the charger and the EV; and a connector or plug matched to the vehicle's charging interface.

An electric scooter is a two-wheeled vehicle powered by an electric motor and rechargeable battery, aimed at offering the means for efficient, eco-friendly, and cost-effective urban mobility. Apart from the traditional scooters that are powered by internal combustion engines, the electric scooters make use of lithium-ion or lead-acid batteries that feed an electric supply to a BLDC motor, which drives the wheels either directly or via a belt or chain mechanism.

Electric bikes, commonly referred to as e-bikes, are one of the most transformational innovations in modern personal mobility, combining conventional bicycle mechanics with advanced electric propulsion technology. At the heart of e-bikes are an electric motor, a rechargeable battery, and a control system that add assistance to the rider while pedaling, making cycling easier, faster, and more accessible across varied terrains. Based on their design, they can be further categorized into pedal-assist, throttle-controlled, or hybrid models, each providing different levels of rider control and engagement of the motor.

The micro-mobility industry has emerged as a transformative force in urban transportation, revolutionizing how people navigate cities worldwide. According to IMARC, the global micro-mobility market size was valued at USD 63.10 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 204.83 Billion by 2033, exhibiting a CAGR of 12.86% from 2025-2033.

India's electric vehicle (EV) revolution is accelerating at a breakneck speed, powered by a strategic combination of government incentives, infrastructure investments, and manufacturing policies that are transforming the automotive landscape. The IMARC Group forecasts that the Indian electric car market reached USD 963 Million in 2024.

The diesel engine industry is standing at a transformative crossroads. As global markets are pushing for sustainability, stricter emissions compliance, and cutting-edge innovations, diesel powertrains are facing both immense pressure and promising potential.

The global tire market is a multi-billion-dollar industry, driven by the growing demand for vehicles across emerging economies and the replacement tire segment in developed countries. The global tire market is expected to grow at a compound annual growth rate (CAGR) of 4.70% between 2025 and 2033. The industry is heavily influenced by factors such as technological advancements, raw material prices, environmental regulations, and consumer preferences.

Australia's electric vehicle (EV) sector is experiencing swift expansion, fueled by increasing interest in eco-friendly transportation alternatives. In 2024, sales of battery electric and plug-in hybrid vehicles hit an all-time high, totaling around 114,000 units.

The electric bus industry is the part of the transportation sector that deals with the production and installation of buses that run completely or partially on electricity, employing battery packs or fuel cells in place of conventional diesel or gasoline engines. The buses deliver lower greenhouse gas emissions, lesser noise levels, and enhanced energy efficiency, and thus they are a prime solution for environmentally friendly public transport.

India's electric vehicle market is undergoing a profound transformation, impelled by green priorities, economic imperatives, and changing consumer trends. With rising concerns about air pollution and fossil fuel dependence, electric mobility has become a strategic option for India's transport industry. Policy clarity, technology development, and an emerging ecosystem of makers and suppliers are driving this market shift.

The global electric vehicle market size was valued at USD 755 Billion in 2024. The global EV market is rapidly expanding, driven by technological advancements, government incentives, stricter emission regulations, rising fuel costs, extended battery range, growing environmental consciousness, and significant investments in charging and production infrastructure.

Electric Vehicles, or EVs, are vehicles operated partially or wholly by electrical power, generally with rechargeable battery packs as their fuel. In contrast to conventional internal combustion engine cars, EVs emit no tailpipe emissions, making them a cleaner, environmentally friendly transportation choice. EVs comprise Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Hybrid Electric Vehicles (HEVs), and are gaining ground in passenger, commercial, and two-wheeler segments owing to developments in battery technology, charging infrastructure, and policy support.

Aluminum alloy wheels are high-performance, lightweight, and durable components widely used in the automotive industry. Their superior strength-to-weight ratio enhances vehicle efficiency, fuel economy, and handling, making them a preferred choice for both passenger and commercial vehicles. Beyond their functional benefits, aluminum alloy wheels contribute to vehicle aesthetics, offering sleek designs and customization options that appeal to consumers. Their corrosion resistance and thermal conductivity further enhance braking performance and longevity. With increasing demand for fuel-efficient and stylish vehicles, aluminum alloy wheels play a crucial role in the global automotive sector, catering to OEMs, aftermarket suppliers, and performance vehicle manufacturers.

A tyre is a crucial component of a vehicle, serving as the outer covering of a wheel. Its main purposes are to support the vehicle's weight, provide traction for movement, and act as a flexible cushion that absorbs shocks from the road. Usually composed of rubber, tires are strengthened with steel and cloth. Tires for cars, trucks, motorbikes, bicycles, and other vehicles have different designs and compositions depending on the vehicle type and its intended usage. To improve stability and grip, they have a tread pattern on the outside.

Electric kick scooters are small, battery-operated personal transportation vehicles intended for short-distance and urban movement. They offer an economical and environmentally responsible substitute for conventional modes of mobility thanks to their electric engine, rechargeable battery, and lightweight frame. The need for sustainable transportation options, traffic congestion, and growing urbanisation have all contributed to their rise in popularity. Electric kick scooters are now the go-to option for last-mile connectivity and personal commuting because to developments in battery technology, connectivity features, and government programs encouraging micro-mobility.

An automotive wiring harness is an organized assembly of electrical wires, connectors, and terminals that transmit power and signals across a vehicle’s electrical system. It guarantees effective communication between several parts, including the engine control unit, lighting, and sensors. Wiring harnesses are intended to increase vehicle performance and safety by lowering the possibility of short circuits. By maximising electrical connectivity and lowering wire complexity, they are utilised in both conventional and electric automobiles and are essential to contemporary automotive technology.

In an automotive braking system, brake pads are the most important parts since they are engineered to contact the brake rotor to produce friction, thus stopping or slowing down a vehicle in virtually any driving condition safely and efficiently. The key way of classifying these pads is according to their material types: low metallic, ceramic, organic, and semi-metallic.

Tires are essential components of vehicles designed to provide traction, support, and absorb road shocks. Primarily made of rubber, tires consist of treads, belts, and sidewalls that work together to offer grip, stability, and durability. Modern tires come in various types – such as all-season, winter, and performance tires – each engineered for specific driving conditions. The two major tire categories are radial and bias tires, and they are available in different sizes to suit various vehicle types, including passenger cars, light commercial vehicles, medium and heavy commercial vehicles, two-wheelers, and off-road vehicles.

Electric Vehicles (EVs) are powered by electric motors instead of traditional internal combustion engines (ICEs). Electric motors propel EVs by utilizing electricity stored in rechargeable batteries or other energy storage systems. They produce lower or zero tailpipe emissions, reduce air pollution and greenhouse gas (GHG) emissions, and help in mitigating climate change. Electric vehicles consist of various components, such as battery cells and packs, reducers, fuel stacks, power control units, power conditioners, air compressors, humidifiers, motors, on-board chargers, battery management systems, and others. EVs are classified into four types based on propulsion, outlined below.

Saudi Arabia is the second-largest producer and exporter of crude oil and holds the second-largest proven oil reserves in the world, with around 267 billion barrels. The country's oil sector is a significant part of its economy, accounting for 75% of government revenue and approximately 90% of exports. However, due to the volatility of oil prices and the potential for economic instability, Saudi Arabia is increasingly focusing on non-oil activities to reduce its dependency on the oil sector. Non-oil commodities tend to have more stable prices, providing protection against these fluctuations and strengthening the country's social, economic, and financial sectors.