How the 3D Printing Market is Shaping the Global Manufacturing Industry: Trends, Challenges, and Opportunities

Introduction:

The 3D printing industry is currently experiencing a revolutionary growth that has had a radical change on the manufacturing operations within the industries of the world. The technology is also referred to as additive manufacturing (AM), and it is the way to create three-dimensional objects by adding layers to the digital model, thereby providing unprecedented flexibility in both design and production. The 3D printing sector of the world has become a pivotal source of innovation enabler, efficiency, supply chain resilience, and competitive edges to organizations as small-and-medium-sized as small businesses to Fortune 500 organizations.

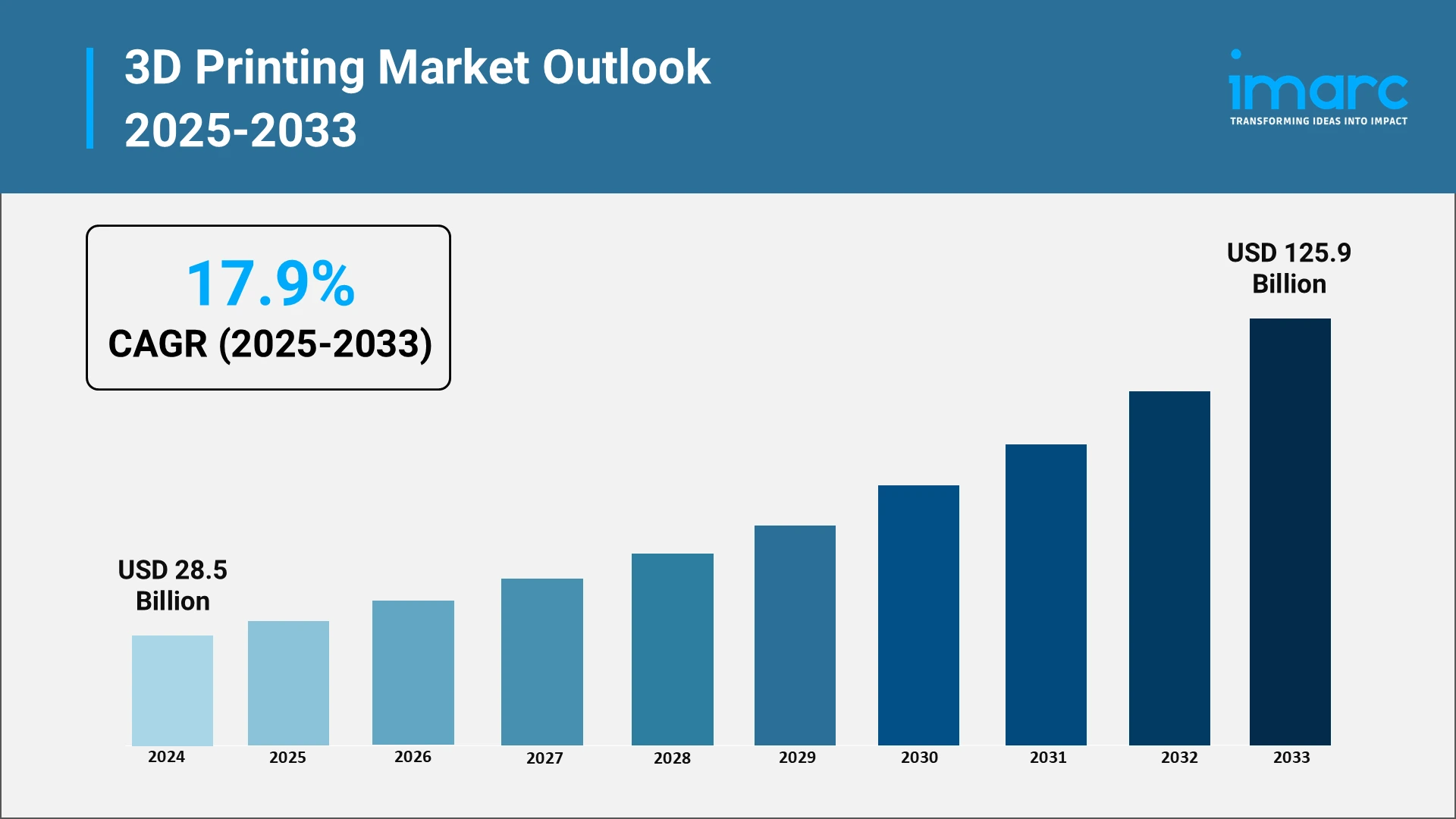

Recent market intelligence will signify exquisite growth paths of the sector. In 2024, the world 3D printing market will reach USD 28.5 Billion. This market will reach USD 125.9 Billion by 2033 with a CAGR of 17.9% in the 2025- 2033 period. This speed is an indication of how the technology is changing into a prototyping tool and a manufacturing solution that is ready to produce and deliver tailored, complicated parts at a reasonable cost.

The strategic significance of the 3D printing market is not restricted to the economic factors. The technology helps manufacturers to overcome the major challenges that include the vulnerabilities in the supply chain, the need to be sustainable, and the increasing pressure on mass customization. Additive manufacturing is a way forward to a more resilient, responsive, and responsible production system as organizations find their way in an increasingly complex global environment with geopolitical tensions, environmental regulations, and rapid technological change.

Explore in-depth findings for this market, Request Sample

The Role, Impact, and Benefits of 3D Printing in the Manufacturing Industry:

3D printing has fundamentally altered traditional manufacturing paradigms by offering capabilities that were previously impossible or economically prohibitive. Unlike conventional subtractive manufacturing methods that remove material from solid blocks, additive manufacturing builds objects layer by layer, enabling the creation of complex geometries with minimal waste. This approach delivers substantial operational and strategic advantages that are driving adoption across diverse industrial sectors.

Operational Efficiency and Cost Reduction

The technology delivers significant cost savings through multiple mechanisms. Organizations can reduce material waste by up to 90% compared to traditional machining processes, as additive manufacturing only uses the exact amount of material required for each part. Lead times for prototyping and production shrink dramatically, enabling faster product development cycles and time-to-market acceleration. According to a global survey by Protolabs on market growth in 2024, 70% of businesses printed more parts in 2023 than in 2022, while 80% of respondents reported that 3D printing enabled them to save substantial costs.

Organizations in various industries are using them as a competitive edge. Manufacturers in the aerospace industry apply 3D printing to manufacture lightweight parts that are fuel-efficient and emit less carbon. The technology is used in the automotive industry to perform rapid prototyping, tooling, and more often in producing parts used in the final product. It is noteworthy that most of the respondents (47 percent) in the Protolabs survey expressed that they would choose 3D printing rather than any other manufacturing technique.

Design Freedom and Innovation Enablement

Additive manufacturing opens new design opportunities never before possible due to the restrictions of traditional manufacturing. This allows engineers to make parts that have internal lattice structures, complex cooling channels, and organic geometries optimized by computational design and topology optimization algorithms. This freedom of design allows it to perform better than the traditional techniques, including the consolidated assemblies that minimize the number of parts, weight, and failure points.

Healthcare is one of the areas that has demonstrated these transformational capabilities. Medical practitioners have been using 3D printing to make patient-specific surgical guides, custom implants, and anatomy models to use in pre-surgical planning. Approximately 77 percent of the respondents feel that the medical industry will be the most affected using 3D printing. Dental uses, such as the custom aligners, crowns, and bridges, are the fast-growing market segments where personalization is directly proportional to improved patient results.

Supply Chain Resilience and Localized Production

The COVID-19 pandemic brought unprecedented focus to supply chain weaknesses, spurring interest in additive manufacturing as a supply chain resilience strategy. With digital inventories instead of physical components, organizations can produce on-demand near end-use points, creating a distributed manufacturing paradigm that eliminates inventory carrying costs, obsolescence exposure, and transportation emissions while enhancing responsiveness to demand variability.

In January 2025, 3D Systems and Daimler Truck AG partnered to enable certified additive manufacturing partners to 3D print nearly 40,000 bus spare parts on demand, cutting delivery times by up to 75%. This collaboration demonstrates how 3D printing enables decentralized production networks that enhance supply chain agility and reduce service downtime in critical applications.

Key Growth Drivers in the Global 3D Printing Market:

Multiple converging factors are propelling the 3D printing market toward sustained double-digit growth through the end of the decade. Understanding these drivers provides insight into where opportunities and investments will concentrate in the coming years.

Technological Advancements and Material Innovation

Continuous improvements in printing technologies are expanding the performance envelope and application scope of additive manufacturing. The integration of hybrid manufacturing and the MELD process is revolutionizing production efficiency and expanding the application scope of 3D printing. Multi-laser systems now achieve deposition rates exceeding 150 cc/hour for high-performance alloys, addressing historical speed limitations that constrained industrial adoption.

Material science breakthroughs are equally critical to market expansion. Metals and alloys are expected to witness rapid expansion driven by their widening applications across aerospace, medical, and automotive sectors, supported by declining powder prices and advancements in multi-laser printing technologies. The availability of certified materials for regulated industries removes adoption barriers and enables qualification for flight-critical aerospace components and medical implants.

Industry 4.0 Integration and Digital Transformation

The convergence of additive manufacturing with broader Industry 4.0 technologies amplifies its strategic value. Cloud-based platforms enable collaborative design and distributed manufacturing networks. Artificial intelligence optimizes build parameters, predicts failures, and accelerates qualification processes. Real-time process monitoring through embedded sensors ensures quality assurance and enables closed-loop control systems.

These digital integrations transform 3D printing from a standalone technology into a fully networked manufacturing capability. Organizations can now implement lights-out production facilities where automated systems handle part removal, post-processing, and quality inspection with minimal human intervention. This automation drives down labor costs while improving consistency and traceability.

Rising Demand for Customization and Rapid Prototyping

Consumer expectations for personalized products are driving demand for manufacturing technologies capable of economic customization at scale. The 3D printing market benefits when OEMs bundle subscription-based machine leasing with remote monitoring, lowering financial barriers and expanding the user base. This shift toward servitization makes advanced manufacturing capabilities accessible to organizations that cannot justify large capital expenditures on equipment.

The prototyping market remains robust as companies seek to accelerate innovation cycles. However, the transition toward production applications is accelerating, with functional parts manufacturing expected to grow at the highest CAGR through 2030 as technologies mature and costs decline.

Regulatory Framework and Policy Landscape in the 3D Printing Industry:

Standardization and regulatory frameworks are evolving to address the unique challenges posed by additive manufacturing while enabling broader industrial adoption. International standards bodies and regulatory agencies are developing comprehensive guidelines that balance innovation with safety, quality, and intellectual property protection.

International Standards Development

The collaboration between ASTM International and the International Organization for Standardization (ISO) has produced a comprehensive framework for additive manufacturing standards. These organizations established a partnership to jointly develop and publish standards that harmonize requirements globally, reducing compliance complexity for multinational manufacturers.

Key standards address fundamental aspects of the technology. ISO/ASTM 52900:2021 defines Additive Manufacturing General Principles, Fundamentals And Vocabulary, establishing uniform terminology that reduces ambiguity across industries. Additional standards specify requirements for materials characterization, machine qualification, operator certification, and part acceptance testing.

The ISO/ASTM 52941-20 standard addresses Additive Manufacturing System Performance and Reliability for Laser Beam Powder Bed Fusion Machine Acceptance Testing for Aerospace Metallic Materials. This specification enables qualification of 3D prints for use in civil, commercial, and military aircraft, addressing one of the most demanding regulatory environments in manufacturing.

Industry-Specific Regulatory Developments

Regulated industries including aerospace, medical devices, and automotive have developed sector-specific qualification pathways. The Federal Aviation Administration (FAA) has published roadmaps for certifying additively manufactured aircraft components, while medical device regulators require extensive biocompatibility and performance testing for implantable parts.

In June 2025, ASTM International launched a new manufacturer certification program to improve process control across the entire AM chain, featuring over 25 end users including Siemens Energy, Ford, Lockheed Martin, Boeing, and Medtronic. This certification validates activities specific to additive manufacturing that traditional quality management systems do not address, closing critical gaps in qualifying manufacturers for high-performance applications.

Intellectual Property and Data Security Considerations

The digital nature of additive manufacturing raises novel intellectual property challenges. Design files can be easily copied and distributed, creating enforcement difficulties for patent holders. Organizations must balance the need for secure file management with the collaborative opportunities enabled by digital manufacturing networks.

Regulatory frameworks are beginning to address these concerns through enhanced traceability requirements and digital rights management solutions. However, the pace of technological change continues to outstrip regulatory development, requiring organizations to implement robust internal controls and contractual protections.

Government Support and Initiatives for the 3D Printing Market:

Government programs worldwide recognize additive manufacturing as strategically important for economic competitiveness, national security, and technological leadership. Public sector investments are accelerating technology development, workforce training, and commercial adoption through multiple mechanisms.

United States Government Programs

The United States has established comprehensive programs to advance domestic additive manufacturing capabilities. America Makes, founded in 2012 as the Department of Defense's National Manufacturing Innovation Institute for AM and the first of the Manufacturing USA network, is based in Youngstown, Ohio, and managed by the National Center for Defense Manufacturing and Machining. This public-private partnership accelerates technology adoption and builds workforce capabilities through collaborative research projects.

In 2025, America Makes issued a new open project call worth $4.5 million, funded by the Office of the Under Secretary of Defense for Research and Engineering, titled "Improvements in Manufacturing Productivity via Additive Capabilities and Techno-Economic Analysis 3.0" (IMPACT 3.0). The initiative focuses on demonstrating improvements in lead time, productivity, and yield for casting and forging operations using additive manufacturing technologies.

The AM Forward initiative represents another major federal effort. Supported by the Applied Science & Technology Research Organization (ASTRO), the federal government is working with GE Aviation, Honeywell, Lockheed Martin, Raytheon, and Siemens Energy to drive AM adoption among small-and-medium sized enterprises through financing, technical assistance, and procurement commitments.

International Government Initiatives

Beyond the United States, governments worldwide are implementing supportive policies. Under China's "Made in China 2025" strategy, 3D printing has been identified as a key development area, with government support primarily focused on research and development (R&D) over commercialization, prioritizing aviation and metal printing. Between 2014 and 2016, the Ministry of Science and Technology launched 51 research and development (R&D) projects on 3D printing, with over 400 million CNY pledged for multi-year research initiatives.

Defense and National Security Applications

Military organizations represent significant drivers of additive manufacturing adoption and funding. The Department of Defense has invested heavily in research and development since launching a 2014 initiative to explore 3D printing for military applications, with many initiatives transitioning into operational use. The Marine Corps has used 3D printing to produce replacement parts for ground vehicles, while the Navy has used it to make components for aircraft.

In January 2025, America Makes awarded USD 2.1 Million to projects focused on in-situ metrology, sustainable powder recycling, and low-cost aluminum parameter sets. These investments address technical barriers to scaling production while reducing costs and environmental impacts.

Top 3D Printing Companies Worldwide:

The 3D printing market features a competitive landscape with established industry leaders, innovative challengers, and specialized players serving specific technology segments or applications. Understanding the capabilities and strategies of leading companies provides insight into competitive dynamics and future market evolution.

Market Leadership and Competitive Positioning

The 3D printing market remains highly fragmented, with the top five players, Stratasys (US), EOS GmbH (Germany), HP Development Company, L.P. (US), 3D Systems, Inc. (US), and General Electric Company (US), collectively accounting for just 15–18% of the total market share as of 2024. This fragmentation reflects the diversity of technologies, materials, and applications within additive manufacturing, with different companies excelling in specific niches.

Stratasys maintains leadership in polymer 3D printing through its diverse technology portfolio, including FDM and PolyJet systems. For the full year 2024, Stratasys revenue came in at $572.5 Million, with the company posting an adjusted net income of $4.2 Million, reflecting the impact of cost-cutting measures and strategic changes. The company maintained a strong cash position, ending the year with $150.7 Million in cash and equivalents, with no debt on its balance sheet.

In March 2025, Stratasys unveiled the Neo800+, a large-format SLA 3D printer at the AMUG conference, which integrates ScanControl+ to boost print speeds by up to 50%, while maintaining high accuracy. The company's focus on large-scale printing and industrial customers positions it to capture growth in production applications.

Technology Innovators and Specialists

EOS GmbH has established dominance in industrial metal printing through its direct metal laser sintering technology. In June 2024, EOS launched the EOS M 290-2, featuring dual 400W lasers and a 250×250×325mm build volume, with enhanced productivity through optimized gas flow and active cooling. Nearly 2,000 M 290 systems are already installed worldwide. This installed base provides recurring revenue through materials and services while establishing de facto industry standards.

HP Inc. entered the additive manufacturing market with its Multi Jet Fusion technology and has rapidly gained share in polymer powder bed fusion. In March 2024, HP and DyeMansion partnered to integrate HP's 3D printing technology with DyeMansion's postprocessing workflows, offering a complete solution for large-scale, high-quality part production. HP's emphasis on production-grade systems and ecosystem integration aligns with market shifts toward serial production.

Emerging Competitors and Market Consolidation

The market continues to see entry from specialized players and consolidation as companies seek scale and complementary capabilities. Following the earnings release, a major development is the pending $120 Million investment from Fortissimo Capital, which will give the Israeli private equity firm a 14% stake in Stratasys and a seat on its board, providing additional cash for potential acquisitions.

The competitive landscape is also being reshaped by Asian manufacturers expanding into Western markets with cost-competitive offerings. In July 2025, India's first 3D-printed flexible toy brand, Vinglits, was launched by WOL3D, demonstrating how additive manufacturing is enabling new product categories and business models in emerging markets.

.webp)

Opportunities and Challenges in the Global 3D Printing Market:

The 3D printing market presents substantial growth opportunities alongside significant challenges that organizations must navigate to capture value from this transformative technology. Understanding both sides of this equation is essential for strategic planning and investment decisions.

Market Opportunities

- Production Scale Applications: The transition from prototyping to production represents the largest opportunity in additive manufacturing. Industrial platforms dominate market spending as the automotive, energy, and aerospace sectors shift from prototype tooling toward large-scale, serial production, reflecting accelerating adoption of advanced manufacturing technologies. Technologies now achieve speeds and costs approaching conventional manufacturing for specific applications, opening addressable markets worth billions of dollars.

- Services and Distributed Manufacturing: Contract manufacturers such as Stratasys Direct Manufacturing, Materialize, and Protolabs leverage multi-site networks to distribute load, allowing customers to prototype and receive production ISO-13485 parts within ten days. This services boom lowers financial barriers and expands the user base by enabling access to capabilities without capital expenditure.

- Sustainability and Circular Economy: Additive manufacturing inherently supports sustainability objectives through material efficiency, localized production that reduces transportation emissions, and the ability to use recycled materials. Organizations pursuing ESG objectives can leverage 3D printing to demonstrate tangible environmental improvements.

Market Challenges

- High Capital Investment Requirements: Despite declining equipment costs for desktop systems, industrial-grade 3D printing systems require substantial capital outlays. Advanced metal printers can cost hundreds of thousands to millions of dollars, while supporting infrastructure, including powder handling, post-processing equipment, and quality inspection systems, adds significant expenses. This investment threshold limits adoption among small and medium enterprises without access to financing or government support programs.

- Material Limitations and Certification: While material options continue expanding, many industries require specialized materials that lack established supply chains or regulatory approvals. Qualification processes for new materials in regulated industries can require extensive testing spanning months to years, delaying commercialization of innovative material formulations. Material costs remain significantly higher than conventional manufacturing feedstocks, constraining economic viability for price-sensitive applications.

- Skilled Workforce Shortage: The interdisciplinary nature of additive manufacturing demands expertise spanning materials science, mechanical engineering, software development, and quality assurance. However, translating academic exposure into industry-ready capabilities requires sustained workforce development investments that many organizations struggle to justify.

- Macroeconomic Headwinds: Interest rate changes had a downstream effect that discouraged purchases of 3D printing equipment in 2024, while generally poor macroeconomic conditions, especially in Europe, impacted the 3D printing industry's growth. Economic uncertainty causes organizations to defer capital investments and technology transitions, creating cyclical challenges for equipment manufacturers and service providers.

- Quality Assurance and Process Control: Ensuring consistent part quality remains challenging due to the complex interplay of process parameters, material properties, and equipment capabilities. Real-time process monitoring and in-situ quality inspection technologies are advancing, but not yet universally deployed. Industries with stringent quality requirements demand extensive validation that increases time-to-qualification and costs.

Conclusion:

The 3D printing market stands at a pivotal juncture in its evolution from emerging technology to mainstream manufacturing solution. Market fundamentals remain strong, supported by rapid technological progress, broader material innovations, and rising adoption across a wide range of industrial applications. The technology has proven its value proposition through countless applications spanning aerospace, automotive, healthcare, consumer goods, and beyond.

Government support through initiatives like America Makes and AM Forward provides crucial backing for continued innovation and commercialization. International standards development by ASTM and ISO removes adoption barriers while ensuring quality and safety. Leading companies, including Stratasys, 3D Systems, EOS, and HP continue investing in next-generation capabilities that push performance boundaries and expand addressable markets.

However, realizing the full potential of additive manufacturing requires addressing persistent challenges. Organizations must justify capital investments in uncertain economic environments, develop skilled workforces capable of leveraging advanced technologies, and navigate complex regulatory landscapes. The transition from prototyping to production-scale applications demands sustained focus on quality assurance, process control, and total cost of ownership optimization.

For corporate strategy teams, investors, and business development professionals, the 3D printing market represents both opportunity and imperative. Companies that successfully integrate additive manufacturing into their operations will gain competitive advantages through faster innovation cycles, more resilient supply chains, and superior customization capabilities. Those that delay risk being disrupted by more agile competitors who leverage these capabilities to deliver better products faster and at lower costs.

The future of manufacturing is undoubtedly additive. The question is not whether organizations will adopt 3D printing, but when and how effectively they will do so.

Partner with IMARC Group for Strategic 3D Printing Market Intelligence:

Choose IMARC Group as your trusted partner in navigating the rapidly evolving 3D printing market and unlocking opportunities within the global manufacturing landscape.

- Data-Driven Market Research: Gain comprehensive insights into market dynamics, technology trends, and competitive positioning through our in-depth research reports covering additive manufacturing adoption across aerospace, automotive, healthcare, and industrial sectors.

- Strategic Growth Forecasting: Anticipate emerging trends in 3D printing technologies—from metal powder bed fusion and binder jetting to advanced polymer systems and hybrid manufacturing—segmented by geography, application, and end-user industry.

- Competitive Benchmarking: Analyze the strategies of leading 3D printing companies, evaluate technology portfolios, and monitor innovations in materials science, software platforms, and production workflows that are reshaping manufacturing competitiveness.

- Policy and Infrastructure Advisory: Stay ahead of regulatory developments, government funding programs, and standardization initiatives affecting additive manufacturing adoption, qualification processes, and supply chain integration.

- Custom Reports and Consulting: Access tailored market intelligence aligned with your strategic objectives—whether expanding into new geographic markets, evaluating technology investments, assessing acquisition targets, or developing go-to-market strategies for 3D printing solutions.

At IMARC Group, we empower manufacturing leaders, investors, and policymakers with the clarity and intelligence required to make confident decisions in the transformative 3D printing market. Connect with us to accelerate your organization's journey toward advanced manufacturing excellence—because innovation demands insight.

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

The education sector in India is witnessing a sea change with digital learning becoming integral to both formal and informal education. The rapid rise of online education platforms has reshaped the way schools, coaching institutes, and higher education centers impart learning experiences, accelerated by pandemic-driven digital acceleration. And today, technology-enabled education is no longer confined to urban centers; it is reaching Tier-2 and Tier-3 cities, democratizing access to quality learning resources for millions of students.

India’s healthcare sector is undergoing a technological transformation, with artificial intelligence positioned as a central driver of change. With a population exceeding 146.39 crore and a system challenged by issues of accessibility, affordability, and quality, AI is no longer optional but essential for building sustainable healthcare solutions.

India health and wellness market is on a fast track, with more people paying attention to preventive care and overall well-being. IMARC Group stated that the market hit USD 156.01 Billion in 2024, owing to the boom in nutraceuticals, fitness, and digital health platforms. Artificial intelligence (AI) is bringing a fresh wave of innovation to health and wellness, enhancing personalized fitness routines, predictive health insights, and more efficient wellness tracking.

Japan's ecotourism industry is experiencing a remarkable transformation, positioning the country as Asia's leading destination for sustainable travel experiences. The market, which is reaching unprecedented valuations of USD 12,999.78 Million in 2024, is demonstrating exceptional growth momentum with projections indicating an expansion to USD 34,542.85 Million by 2033, representing a robust compound annual growth rate (CAGR) of 11.47% during the 2025-2033 period.

The United Kingdom is currently establishing itself as one of Europe's most dynamic blockchain innovation hubs, demonstrating remarkable resilience and growth despite global economic uncertainties. The UK blockchain market reached a valuation of USD 0.66 Billion in 2024 and is projecting explosive growth toward USD 54.63 Billion by 2033, exhibiting a compound annual growth rate (CAGR) of 63.26% during the forecast period. This extraordinary trajectory is placing the nation at the forefront of distributed ledger technology adoption and development.

Japan has been a world leader in robotics, especially industrial, for decades. The nation's unflinching faith in technology development, precision manufacturing, and automation has made it a world leader in industrial robotics. Industrial robots have transformed the manufacturing process to become necessary equipment in today's manufacturing, helping companies increase productivity, retain quality, decrease errors in operations, and enhance efficiency in processes.

The Europe 3D printing market stands at the forefront of a manufacturing revolution that is reshaping industries across the continent. As additive manufacturing technologies mature and expand beyond prototyping into full-scale production, European manufacturers, healthcare providers, and aerospace companies are increasingly embracing these transformative solutions. With substantial government backing, strategic industry collaborations, and breakthrough material innovations, the European 3D printing landscape is positioned for remarkable expansion through 2033.

The Philippines gaming industry has emerged as Southeast Asia's fastest-rising digital entertainment powerhouse, achieving USD 4,822.00 Million in gross gaming revenue for 2024. This explosive growth signals a fundamental transformation in how Filipinos engage with interactive entertainment, driven by the rapid adoption of augmented reality (AR) and virtual reality (VR) technologies.

The data monetization market has emerged as a critical pillar of the modern digital economy, transforming how organizations create value from their information assets. As businesses recognize data as a strategic asset, the ability to extract financial value has become a competitive imperative. The global data monetization industry encompasses diverse approaches, ranging from direct data sales to indirect monetization through enhanced decision-making. According to IMARC Group, the industry reached USD 4.1 Billion in 2024. It is projected to reach USD 16.1 Billion by 2033, at a CAGR of 15.76% during 2025-2033.

The global access control market is entering a phase of serious expansion and transformation. In 2024, IMARC placed its value at USD 10.6 Billion, with a forecast of USD 18.8 Billion by 2033 (CAGR of 6.5 %). This reflects how rapidly the underlying technologies, threat landscape, and regulatory regimes are shifting. Across enterprises, campuses, infrastructure sites, and smart buildings, access control is evolving from door-level locks to identity, context, behavior, and integration. In many markets, access control is becoming an essential bridge between physical security and cybersecurity.

The media consumption landscape in Japan is in the midst of a revolutionary change with over-the-top (OTT) services as a leading force behind the way viewers are consuming entertainment content. OTT services, which provide video content directly on the internet and not via conventional cable or satellite television, are fast becoming a standard in Japanese homes. The growth of the Japanese OTT industry has been shaped by various factors, from technological innovations to changing consumer tastes.

The e-commerce market in Mexico is thriving, driven by increased internet access, mobile shopping, and smooth digital payment options. IMARC Group estimated that the market reached an impressive USD 47.52 Billion in 2024, signifying a distinct transition towards online shopping.

The global Industry 4.0 market is experiencing strong momentum, propelled by the integration of smart technologies across manufacturing, logistics, and energy sectors. With automation, connectivity, and data intelligence at its core, Industry 4.0 is reshaping how enterprises design, produce, and deliver products.

The global soft skills training market size was valued at USD 33.39 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 92.59 Billion by 2033, exhibiting a CAGR of 11.40% during 2025-2033. This substantial growth reflects a fundamental shift in how organizations approach workforce development, as the recognition of soft skills as strategic assets rather than supplementary competencies becomes universal across industries.

The global Wi-Fi infrastructure market is experiencing unprecedented expansion, fundamentally reshaping how organizations operate and consumers interact with technology. According to Wi-Fi Alliance, the official industry certification body, 4.1 Billion Wi-Fi devices are forecast to ship in 2024, contributing to 45.9 Billion cumulative Wi-Fi shipments over the technology's 25-year lifetime.

Australia's mobile money industry is experiencing unprecedented transformation as artificial intelligence reshapes the landscape of digital payments, mobile wallets, and financial services. The integration of sophisticated AI technologies has revolutionized how Australians conduct transactions, manage their finances, and interact with digital payment platforms. From smartphone-based payment solutions to advanced fraud detection systems, AI is driving innovation across every facet of the mobile money ecosystem.

India vehicle tracking market is undergoing a significant transformation, with artificial intelligence emerging as a central driver of innovation. According to the IMARC Group’s report, the market size reached USD 0.90 Billion in 2024.

India stands at a decisive stage where economic growth must advance in parallel with environmental sustainability. According to an IMARC Group report, the Indian green technology and sustainability market reached USD 837.2 Million in 2024, reflecting the nation’s growing commitment to sustainable development.

Closed-Circuit Television (CCTV) cameras are electronic monitoring systems that are used to watch, record, and send video images for security and observational reasons. Unlike television broadcasting, CCTV signals are sent to selected monitors or recording devices, and hence they are the backbone of contemporary security infrastructure.

India's educational technology sector stands at the precipice of a transformative revolution, with artificial intelligence (AI) emerging as the primary catalyst driving unprecedented growth and innovation. The convergence of AI technologies with educational platforms is fundamentally reshaping how millions of Indian students access, consume, and engage with learning content, creating an ecosystem that democratizes access to quality education across the country’s diverse linguistic and socioeconomic groups.

Japan’s higher education sector is at a major turning point as demographic and economic pressures converge with technological disruption. One of the major trends in the Japan higher education market include the number of students entering universities has been shrinking for decades due to the country’s aging population, creating structural challenges for institutions that once relied on a stable or growing pool of applicants.

Japan, a global leader in technological innovation, is at the forefront of a new digital revolution in its satellite communication sector. As the nation pushes toward a more connected and resilient future, the integration of Artificial Intelligence (AI) is proving to be a critical catalyst. From enhancing network performance to automating complex operations AI is not just an add-on it is a foundational technology reshaping the very fabric of satellite communication.

Generative artificial intelligence (AI) is rapidly becoming one of the most influential technologies of the decade, and its global footprint is continuously expanding. Nations across the world are exploring its transformative potential, with Japan emerging as a unique hub where technological innovation, traditional industries, and forward-looking government policies are converging.

A battery charger is a piece of electrical equipment that is used to recharge a rechargeable battery by imposing an electric current upon it. The main purpose of a charger is to transfer alternating current (AC) from the power source into an appropriate direct current (DC) that has the required voltage and current for the particular type of battery. Battery chargers play a vital role in a broad variety of applications, from consumer devices and electric vehicles (EVs) to industrial equipment and renewable energy systems.

Indian manufacturing continues to grapple with significant losses caused by defects, rework, and product returns, which weaken profitability and competitiveness. As per an industry report, in FY22, the total return order volume in India stood at 14.86%. Furthermore, high-volume industries such as automotive, FMCG packaging, textiles, and electronics are particularly exposed, where even a small defect rate can translate into substantial financial setbacks. Industry research states that in mature operations, the Cost of Poor Quality (COPQ) can account for as much as 15–20% of total sales. Moreover, Return Prime’s recent report shows that returns remain a major challenge in e-commerce sales, with 17.6% of all orders being sent back.

Industry 4.0 has been a defining milestone in the advancement of manufacturing. It is responsible for introducing automation, digitization, and data-driven processes that significantly enhanced productivity and precision. Presently, India is moving into the next phase of manufacturing, that is, autonomous factories. Here, artificial intelligence (AI) goes beyond simple automation, enabling systems to render decisions, learn from changing conditions, and continuously improve operations. This shift has the potential to reshape industrial growth in the country and establish new standards for smart manufacturing.

Indian manufacturers are facing difficulties due to rising input costs, shortages of skilled labour, unplanned machine downtime, and inconsistent product quality. According to an industry report, during the July–September quarter of FY25, raw material expenses for 1,679 listed non-financial manufacturing companies increased by 5.1%, outpacing sales growth, which rose by only 3.3%. Similarly, the Global Talent Shortage Survey 2025 reported that 80% of Indian employers report difficulty finding skilled talent, compared to the global average of 74%, highlighting a severe talent crunch.

According to the International Energy Agency (IEA), global energy-related CO2 emissions grew by 0.8% in 2024 to a record 37.8 gigatonnes, driving atmospheric concentrations to an unprecedented 422.5 ppm. This has led to an increased urgency in addressing climate change. Similarly, the industries are facing unprecedented pressure to rethink their operations due to the energy demand rising by 2.2% in 2024, which is faster than the annual average of 1.3% witnessed between 2013 and 2023.

India is among the fastest-growing economies globally. The nation is currently the fourth-largest economy in the world and is on its way to becoming the third-largest, with an estimated GDP of USD 7.3 Trillion by 2030. This momentum is not only strengthening India’s economic resilience but also opening lucrative opportunities for businesses, investors, and technology providers aligned with the country’s growth vision.

The role of artificial intelligence (AI) in modern project management has transitioned from a theoretical concept to a strategic imperative. As businesses navigate increasingly complex projects in a data-driven world, AI is emerging as a powerful force for efficiency, accuracy, and innovation.

The artificial intelligence market is no longer niche. Current projections value the market at a significant level today, with strong growth expected as generative AI matures, computing costs decline, and enterprise pilots scale into full production.

The data center sector in Japan is at the epicenter of a tech revolution, wherein artificial intelligence (AI) is fundamentally redefining how digital infrastructure manages, scales, and adapts. With the country progressing toward digital transformation in various industries, AI has been the force behind unprecedented innovation in the design, management, and optimization of data centers.

In the modern era, the global video streaming market is fundamentally reshaping the entertainment landscape, driven by the dual forces of digitalization and the escalating demand for on-demand content. Artificial intelligence (AI) also serves as a pivotal catalyst for this growth, enabling the personalization of user experiences through tailored recommendations, improved content discovery, and enhanced audience engagement.

The global gaming console market is undergoing a significant transformation, fueled by the adoption of artificial intelligence (AI) and an increasing demand for interactive entertainment.

For decades, call centers have played a central role in customer service. Traditionally staffed with large teams of agents, they operated as cost-heavy units designed to handle inquiries, complaints, and service requests. While essential, this model was often associated with inefficiencies, long wait times, and high employee turnover.

According to IMARC Group, the global identity verification market was valued at USD 13.8 Billion in 2024 and is projected to reach USD 46.4 Billion by 2030, expanding at a CAGR of 14.4% during 2023–2030. This strong growth is being fueled by the increasing adoption of artificial intelligence (AI) and machine learning (ML), which are enabling higher levels of automation, fraud detection, and real-time authentication.

Japan is a leader in digital transformation, known for being one of the most advanced nations in technology globally. Artificial Intelligence (AI) is becoming an integral force across various sectors, and the telecom industry is no exception.

Generative AI is revolutionizing industries by bringing fresh, game-changing solutions that boost creativity and streamline workflows. Whether it’s automating content creation or optimizing complex processes in fields like healthcare and finance, AI is opening doors to exciting new possibilities.

The e-commerce market has undergone a seismic shift in the past twenty years. What started as simple, text-based product pages has grown into a complex web of intelligent platforms capable of customizing experiences for every individual user. At the core of this evolution is Artificial Intelligence (AI).

The global laptop and tablet market includes portable computing devices for both personal and commercial use, providing mobility, flexibility, and connectivity. Laptops extend desktop computers' power and functionality in a portable package, while tablets provide light-touch screen interfaces for consumption of media, creative work, and on-the-go productivity.

The global cloud gaming industry is experiencing an unprecedented surge, driven by technological advancements and evolving consumer preferences. As the market expands, Artificial Intelligence (AI) stands out as a pivotal force, reshaping every facet of the cloud gaming landscape, from infrastructure to player experience. It enables smarter resource allocation, real-time content personalization, latency reduction, and advanced game logic.

The global power bank market is experiencing steady growth as digital lifestyles become more integrated into everyday routines. With rising dependence on smartphones, tablets, laptops, and wearables, power banks have shifted from being simple backup batteries to versatile, feature-rich accessories that fulfill the needs of a wide range of users. Consumers now prefer power banks with fast-charging capabilities, higher battery capacity, and environmentally responsible designs.

The hybrid cloud market across the world has been changing at a very fast rate, with companies globally adopting the mix of on-premises and cloud-based infrastructures to fuel innovation and operational effectiveness.

Japan’s artificial intelligence (AI)-driven three-dimensional (3D) printing startups are redefining manufacturing by merging speed, sustainability, and precision. Japan’s additive manufacturing scene is moving beyond prototypes—it's rewriting how industries build, design, and innovate.

As a global leader in technology and innovation, Japan has increasingly recognized the critical importance of cybersecurity to protect its digital infrastructure.

Electric cables or power cables are the fundamental parts employed for the transfer of electrical power or signals over short and long distances. They generally comprise one or more conductors, typically composed of copper or aluminum, covered with insulating materials and protective sheaths. Electric cables, based on their use, differ in structure, including low-voltage, medium-voltage, and high-voltage power cables, control cables, instrumentation cables, or data transfer cables like fiber optics.

Smart Factory and Industry 4.0 Integration is a comprehensive set of services that helps firms overhaul their manufacturing processes by embracing new technologies such as the Internet of Things (IoT), Artificial Intelligence (AI), robotics, big data analytics, and cloud computing.

Digitalization is reshaping the very essence of travel, transforming it into a more personalized, convenient, and efficient experience than ever before. With the growing popularity of travel platforms, travelers now have the power to plan and book their entire journey with just a few taps on their smartphones.

Product and facility certification support offers professional assistance to companies in resolving complicated processes of product certification and facility certification. Our services facilitate adherence to global standards and regulatory guidelines to ensure hassle-free market entry and operational continuity across global markets.

The global e-commerce landscape is rapidly transforming, propelled by several evolving e-commerce industry trends. These fundamental shifts encompass changes in consumer behavior, rapid technological advancements, and increasing internet accessibility worldwide. As a direct result, brands are now prioritizing quick delivery, mobile-centric platforms, and deeply customized digital experiences.

Setting up a drone manufacturing plant with a step-by-step business plan covering setup, costs, equipment, compliance, and market strategy.

India’s textile industry is undergoing a transformative shift led by the government’s visionary PM MITRA (Mega Integrated Textile Region and Apparel) Parks initiative. With a mission to establish India as a worldwide leader in textiles, this program is creating world-class integrated manufacturing zones that drive innovation, reduce production costs, and boost sustainability.

India’s sports technology sector is gaining extraordinary momentum, driven by the digitalization of sports leagues, enhanced fan engagement, and increasing investments in athletic performance solutions. With the Indian Premier League (IPL) 2025 poised to become the most tech-driven tournament to date, the market is no longer restricted to wearables and broadcasting; it now powers every aspect of sports, from grassroots training to AI-based strategic decision-making.

India is becoming a popular location for foreign manufacturers because of its quickly expanding economy, affordable labour costs, and consistent government support. For businesses looking to establish manufacturing facilities in the nation, the Government's "Make in India" incentive program offers an alluring alternative. This guide will assist in comprehending the crucial requirements for setting up a manufacturing facility in India.

Factory audits are important for companies that intend to ensure compliance and quality in operations as well as supply chain efficiency. India is experiencing unparalleled growth in manufacturing. The skills to perform factory audits effectively can be used to counter most risks related to Indian supplier relationships. This blog gives a complete step-by-step guide on how to perform factory audits in India, including a complete checklist.

Establishing a manufacturing plant is a major investment that requires meticulous planning and a thorough understanding of the associated costs. Whether a seasoned entrepreneur or an industrial novice, understanding the "cost equation" is vital for making informed financial decisions and ensuring the long-term profitability of the operations. This blog will break down the various expenses associated with establishing a manufacturing facility in India.

Setting up a manufacturing plant is a significant milestone for any business, but it comes with complexities that require careful planning, research, and execution. From selecting the right location to ensuring regulatory compliance and operational efficiency, every aspect needs expert attention to guarantee success. This is where IMARC Group steps in, offering comprehensive pre-feasibility studies and consultation services to help businesses establish manufacturing plants seamlessly.

The manufacturing sector is a cornerstone of India's economy. It accounted for about 14% of the overall GDP of the nation in 2024 and has employed millions of people across the country. India has been a rising manufacturing powerhouse globally and 2025 is expected to be a turning point. Given the better government focus and strong labor force, along with the increasingly effective infrastructure, India is likely to be sealed as a prime destination for global manufacturers.

Many have encountered this scenario: visiting a website with enthusiasm to purchase a product seen in an advertisement, only to face challenges such as navigating a complex interface, unresponsive customer service, and a cumbersome checkout process.

The OTT industry is experiencing a pivotal transformation, signaling the advent of a new digital entertainment era. Consumers are increasingly demanding convenience and personalized experiences on OTT platforms. As a result, platforms are investing massively in technologies such as AI to enhance the recommendations of content and improve user experience.

From established giants in the United States and Europe to fast-paced markets in Asia, the e-commerce revolution is creating a competitive marketplace that transcends geographical boundaries. Vietnam stands out as a key force in this global trend, showcasing the potential of e-commerce to drive national economic transformation. The country’s e-commerce industry is witnessing tremendous growth, driven by new markets and growth opportunities in established markets.

Head-mounted displays consist of small displays with in-built sensors and optics that project images directly onto the user's eyes. They provide a virtual reality (VR) or augmented reality (AR) experience that allows users to interact with digital objects or environments. They resemble glasses or goggles and are designed to be worn on the head. They comprise many components, such as a controller, sensor, camera, lens, goggles, head tracker, case, connector, display, battery, processor, memory, pico projector, and accessories. Tracking systems and sensors detect the user's head movements and adjust the displayed content accordingly, offering the user a more realistic, immersive, and interactive experience.

5G technology or fifth-generation wireless technology is the latest advancement in mobile communication systems that provides enhanced data transfer speeds, reduces latency rates, improves reliability, and increases network capacity. This technology operates in the mm-wave spectrum, the spectrum band ranging from 30 to 300 gigahertz (GHz), which facilitates high-speed networks and faster data delivery. 5G technology supports the growth of emerging technologies like artificial intelligence (AI), machine learning (ML), and edge computing, enabling new business models and unlocking economic potential. It enhances the performance of business applications and digital experiences, such as video conferencing, online gaming, live streaming media, and self-driving cars. The components included in 5G technology are hardware, software, and services, and it is utilized in a wide range of applications, such as automation, video services, connected vehicles, smart homes, virtual & augmented reality, and monitoring & tracking. For better connectivity of networks, various industries, such as manufacturing, automotive, transportation & logistics, media & entertainment, energy & utilities, healthcare, government, and others, have deployed 5G technology extensively.

Robotics is the branch of engineering that deals with designing, constructing, and operating robots. Robots are programmable machines capable of carrying out tasks autonomously or semi-autonomously. Major types of robotics include industrial and service robots, combining elements of mechanical engineering, electrical engineering, computer science, and artificial intelligence (AI). Industrial robots encompass articulated, Cartesian, SCARA, and cylindrical robots. Service robots serve personal, domestic, and professional purposes, used in various applications, such as household tasks, entertainment, defense, fieldwork, logistics, healthcare, infrastructure, mobile platforms, and cleaning, and more. Robotics can efficiently and accurately perform tasks in environments that may be hazardous or challenging for humans. Robots reduce human labor, enhance production efficiency, lower costs, and improve product quality in various industries. Robotics is further categorized into types such as industrial robotics, food robotics, warehouse robotics, smart robotics, automotive robotics, agriculture robotics, logistics robotics, construction robotics, space robotics, and others. Nowadays, robotics has become an important part of many industries, even being used to explore deep oceans and space. Additionally, it is employed in creating autonomous vehicles, performing surgery, and conducting medical diagnoses.

Artificial Intelligence (AI) chips are designed to accelerate and optimize AI and Machine Learning (ML) workloads. The field of AI involves tasks such as pattern recognition, data analysis, and decision-making, which often require massive parallel processing. AI chips perform various tasks like deep learning, neural network processing, and other computationally intensive operations. These chips are tailored to support the parallel computing needs of AI workloads, making them well-suited for these tasks.

Oman is situated on the southeastern coast of the Arabian Peninsula. It boasts a rich cultural heritage, stunning landscapes, and a diverse range of attractions, making it an emerging destination in the tourism market. The country offers a wide array of tourist activities, including sunbathing, swimming, kitesurfing, diving, snorkeling, boating, among many others. Beach activities and kite surfing are popular in Muscat, Al Sawadi Beach, Alzaiba Beach, and Masirah Island, while desert safaris are a highlight in Wahiba Sands. Oman's rich historical heritage includes numerous UNESCO World Heritage Sites, ancient temples, forts, and palaces, such as Bahla Fort and the Archaeological Sites of Bat, Al-Khutm, and Al-Ayn.

Virtual reality (VR) gaming represents a new generation of computer games that leverage VR technology to provide high-definition visuals, spatial audio, and precise motion tracking, creating a sense of presence and immersion. VR gaming offers a 360-degree view of the virtual environment, keeping players engaged for longer periods compared to traditional gaming. Additionally, VR gaming is used in rehabilitation and the treatment of phobias, anxiety disorders, and other psychological conditions. It is also employed to train soldiers in combat scenarios, strategy, and decision-making.

Cloud computing delivers computing services over the internet, including servers, storage, databases, networking, software, analytics, and intelligence. It promotes faster innovation, flexible resource allocation, and economies of scale. Moreover, it offers numerous advantages, such as cost efficiency, mobility, scalability, reliability, and automatic software updates, among others.