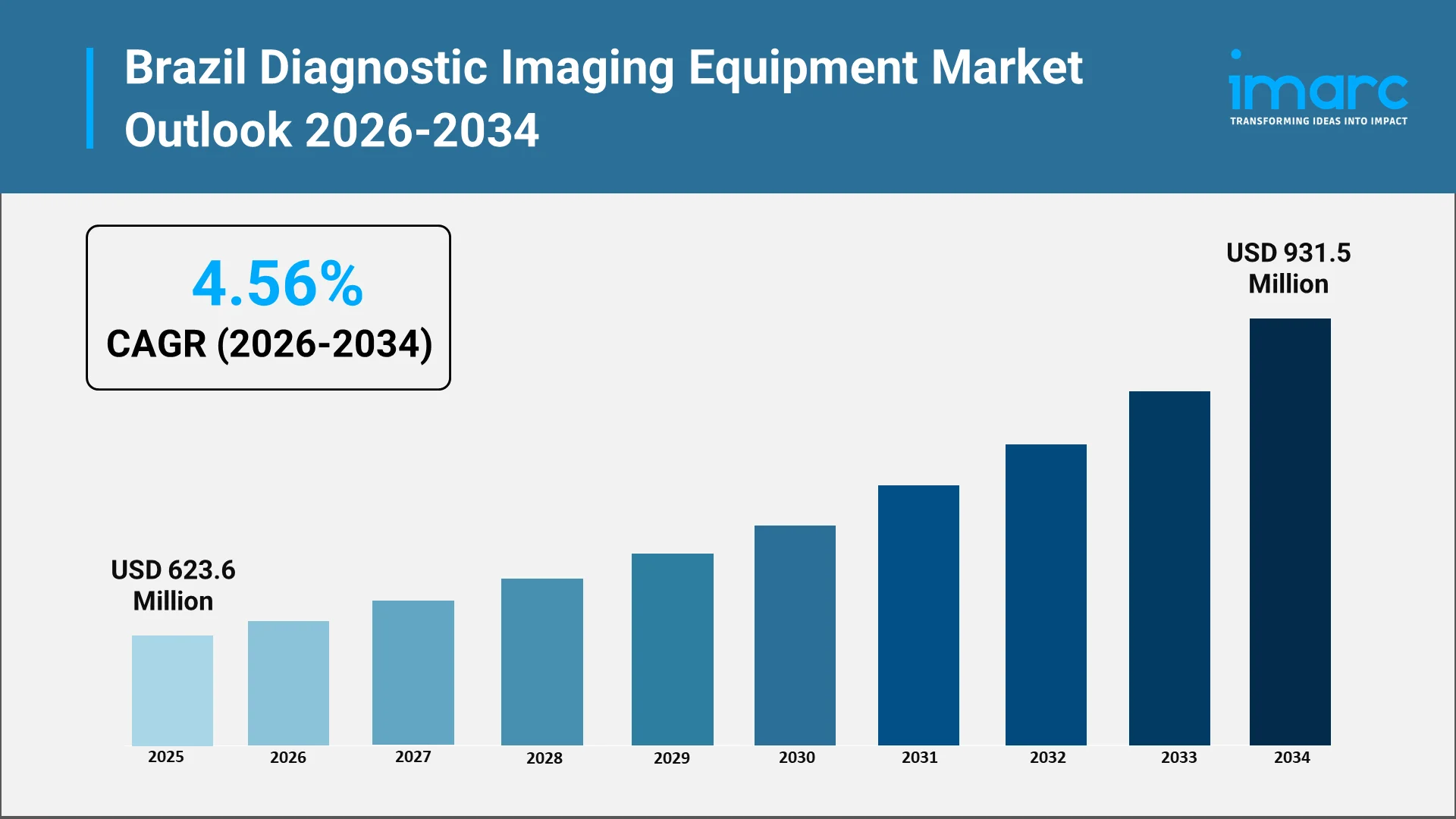

How Big Will the Brazil Diagnostic Imaging Equipment Market Be by 2034?

Brazil's diagnostic imaging equipment market stands at a pivotal moment as Latin America's largest and most dynamic healthcare arena. With substantial investments in hospital modernization, regulatory reforms, and artificial intelligence adoption, the market is transforming rapidly. As providers transition from analog to AI-ready platforms, Brazil emerges as a critical destination for medical device manufacturers seeking growth through the next decade.

Overview of Brazil's Diagnostic Imaging Equipment Market:

Brazil diagnostic imaging equipment market represents the cornerstone of the nation's medical technology sector. The country commands the largest share of Latin America's healthcare spending, with substantial government allocations driving procurement cycles for advanced medical imaging Brazil systems across public and private facilities throughout the nation.

The market encompasses major radiology equipment categories including X-ray systems, computed tomography scanners, magnetic resonance imaging units, ultrasound devices, and nuclear medicine equipment. Urban centers in the Southeast region demonstrate the highest concentration of advanced imaging infrastructure, while rural areas increasingly receive portable units addressing geographical access disparities.

Brazil's dual healthcare system creates unique market dynamics. The public Unified Health System serves the majority through universal coverage, while supplementary private insurance covers additional segments. Both sectors drive equipment demand with distinct purchasing patterns. Public procurement emphasizes cost-effectiveness through competitive bidding, whereas private facilities prioritize premium features and vendor-managed service contracts.

Market Size Forecast and Technology Outlook to 2034:

Looking toward the next decade, Brazil diagnostic imaging equipment market trajectory reflects converging factors promising sustained expansion. Healthcare facilities across public and private sectors recognize the imperative of upgrading imaging capabilities to meet rising patient volumes and increasing clinical complexity driven by demographic and epidemiological shifts.

Advanced modalities gain prominence in the equipment mix. MRI systems experience robust adoption driven by oncology and neurology applications requiring precise soft tissue visualization. CT scanners benefit from cardiac and trauma care expansion, with newer generations offering dose reduction features. Ultrasound equipment maintains strong demand across obstetrics, cardiology, and point-of-care applications.

The healthcare technology landscape evolves as digital transformation reshapes clinical workflows. Picture archiving and communication systems now represent mandatory infrastructure, with government e-health plans requiring PACS compatibility for reimbursement. Vendor-neutral archives gain traction among larger networks seeking interoperability. Cloud-based image storage emerges as a practical solution for institutions lacking on-premise capacity.

Import dependencies characterize the market structure, with substantial equipment value sourcing from international manufacturers. This positions Brazil as a strategic destination for global medical device companies establishing regional operations to optimize logistics and customer support.

Explore in-depth findings for this market, Request Sample

Key Drivers of Equipment Demand and Innovation:

Demographic shifts fundamentally reshape healthcare utilization patterns. Brazil's aging population generates disproportionate imaging volumes as elderly citizens require extensive diagnostic workups for chronic conditions. Life expectancy improvements mean more individuals reach ages where oncologic, neurologic, and musculoskeletal disorders necessitate regular imaging surveillance. This demographic dividend for the healthcare sector creates sustained baseline demand independent of technological advancement cycles.

Chronic disease prevalence escalates across multiple categories. Cardiovascular conditions, diabetes complications, and cancer incidence all trend upward in alignment with lifestyle and environmental factors. Each disease category drives specific imaging modality requirements—cardiac CT for coronary assessment, mammography for breast cancer screening, and MRI for tumor characterization and treatment monitoring. The epidemiological transition from predominantly infectious to predominantly chronic disease burden fundamentally alters imaging equipment portfolio requirements.

Hospital modernization accelerates as both public and private facilities compete for patient volumes and clinical reputation. Legacy institutions upgrade aging infrastructure to attract physicians and maintain accreditation standards. New specialty hospitals and diagnostic centers enter markets with state-of-the-art equipment configurations designed around efficient throughput and premium patient experience. These greenfield projects often specify the latest equipment generations, creating valuable opportunities for manufacturers to showcase innovation.

Clinical practice evolution demands enhanced imaging capabilities. Minimally invasive interventions require real-time imaging guidance with exceptional spatial resolution. Image-guided radiation therapy necessitates precise tumor localization through repeat imaging. Screening programs for early disease detection expand coverage to younger age cohorts, multiplying examination volumes. Each clinical trend translates into equipment specifications that push technological boundaries and justify capital investments.

Healthcare Infrastructure and Government Initiatives:

Brazil's Ministry of Health orchestrates ambitious digital transformation programs restructuring healthcare delivery. Substantial commitments target digitalization of the public system, with resources allocated toward IT equipment and software deployment across thousands of municipalities. Initiatives emphasize connectivity between primary care units and specialized diagnostic facilities, enabling remote consultation even in underserved regions.

The APS Digital program exemplifies government commitment to universal healthcare access through technology. By equipping basic care units in the majority of municipalities, the initiative creates a digital backbone supporting telemedicine and teleradiology services. Patients in remote areas gain access to specialized imaging interpretation without traveling to distant urban centers.

Regulatory modernization through ANVISA accelerates market access for innovative devices. Recent reforms align Brazilian device classification with International Medical Device Regulators Forum standards, incorporating provisions for software as a medical device and nanomaterial-based technologies. The agency now recognizes regulatory clearances from Australia, Canada, Japan, and the United States, substantially reducing local review timelines.

In a significant regulatory milestone, ANVISA officially launched its Unique Device Identification system (Siud) in July 2025, during an event at its headquarters in Brasília. This national system aligns Brazil with IMDRF standards, requiring manufacturers to register devices in the centralized database and apply standardized UDI labels across all risk classifications, supporting enhanced post-market surveillance and global interoperability.

Public-private partnerships gain momentum as financing mechanisms for equipment acquisition. Service contracts with extended warranties, AI-subscription bundles, and performance-based payment models enable institutions to access premium equipment without large upfront capital expenditures.

Adoption of AI and Digital Imaging Technologies:

AI in diagnostics emerges as the defining characteristic of next-generation imaging infrastructure. Artificial intelligence algorithms integrate across the imaging workflow from examination scheduling through image acquisition, reconstruction, analysis, and reporting. Early adopters demonstrate measurable improvements in radiologist productivity, examination throughput, and diagnostic accuracy. The technology proves particularly valuable in addressing radiologist shortages in secondary cities and rural areas.

On October 30, 2025, Brazil became the first South American member of the HealthAI Global Regulatory Network through a formal agreement signed by Minister of Health Dr. Alexandre Padilha at the ABRAMGE Congress in São Paulo. This partnership positions Brazil as a regional catalyst for responsible AI governance in healthcare, emphasizing proper regulation, data protection safeguards, and transparent oversight.

Leading manufacturers bundle AI capabilities as standard features. Smart algorithms automatically adjust acquisition parameters based on patient characteristics, reducing radiation exposure while maintaining diagnostic quality. Computer-aided detection highlights suspicious findings for radiologist review, minimizing oversight errors in high-volume workflows. Automated quantification tools measure anatomical structures with precision exceeding manual assessment.

Telemedicine platforms incorporating AI-assisted interpretation expand rapidly. Portal Telemedicine operates cloud-based systems processing thousands of reports daily, enabling tier-two hospitals to access on-demand reads from remote radiologists. Machine learning applications extend beyond radiology into broader analytics, with predictive algorithms identifying patients requiring earlier intervention based on imaging findings combined with electronic health record data.

.webp)

Competitive Scenario and Future Growth Potential:

The competitive landscape features moderate consolidation with established corporations commanding substantial market shares. GE Healthcare, Siemens Healthineers, and Philips maintain strong positions reinforced by in-country subsidiaries, comprehensive product portfolios, and extensive service networks capable of supporting diverse institutional needs.

GE Healthcare pursues digital transformation through cloud partnerships and remote control specialists. Siemens Healthineers targets cost-sensitive markets with value-engineered products and diversifies into radiopharmaceuticals. Philips Healthcare leads in AI-enabled systems and integrated ecosystems extending beyond equipment to software and services.

Emerging competitors challenge incumbents through differentiated propositions. United Imaging Healthcare offers price-performance advantages with flexible financing. Local innovators like Mobissom's wireless ultrasound fill niche applications. Brazilian developers create tailored radiology information systems understanding local requirements.

Distribution strategies evolve toward life-cycle partnerships with extended warranties, maintenance contracts, and software licensing creating recurring revenues. The refurbished equipment segment addresses budget constraints in resource-limited settings.

The market outlook remains constructive supported by demographic aging, chronic disease proliferation, government spending commitments, and technological innovation consistently delivering clinical value. However, economic volatility, currency depreciation, and workforce shortages present ongoing challenges requiring strategic navigation.

Choose IMARC Group as We Offer Unmatched Expertise and Core Services:

- Data-Driven Market Research: Deepen your knowledge of diagnostic imaging adoption rates, equipment specifications, and technological advancements such as AI-powered diagnostics, cloud-based PACS systems, and telemedicine platforms through in-depth market research reports.

- Strategic Growth Forecasting: Predict emerging trends in Brazil's imaging sector, from portable ultrasound devices and low-field MRI systems to regulatory changes and public health digitalization initiatives across federal and state levels.

- Competitive Benchmarking: Analyze competitive forces in the diagnostic imaging equipment market, review manufacturer product pipelines, and monitor breakthroughs in digital imaging technologies and hybrid modality systems.

- Policy and Infrastructure Advisory: Stay one step ahead of ANVISA regulatory paradigms, government-sponsored modernization programs, and reimbursement strategies affecting diagnostic equipment procurement, installation, and operational sustainability.

- Custom Reports and Consulting: Get tailored insights geared to your organizational objectives—be it launching new imaging modalities, investing in AI-driven diagnostic ventures, or expanding healthcare infrastructure across Brazil's diverse regional markets.

At IMARC Group, our goal is to empower healthcare leaders with the clarity and intelligence required to navigate Brazil's dynamic diagnostic imaging landscape. Join us in advancing diagnostic excellence—because accurate imaging saves lives. Click here for more detailed report: https://www.imarcgroup.com/brazil-diagnostic-imaging-equipment-market

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

The Indian healthcare space has indeed been changing. Telemedicine has emerged as one of the most important drivers of this change. Driving this transformation is the increased adoption of digital tools, growing patient awareness, and the pressing need to make healthcare more accessible across diverse geographies.

The Australia medical aesthetics industry size reached USD 396.4 Million in 2025. Looking forward, the market is expected to reach USD 784.8 Million by 2034, exhibiting a growth rate (CAGR) of 7.89% during 2026-2034. Over the last ten years, the medical aesthetic industry in Australia has transformed from a niche beauty service into a mainstream part of healthcare and wellness.

A rapid diagnostic test (RDT) kit is a medical device designed to quickly detect specific biomarkers, antigens, antibodies, or nucleic acids linked to diseases—typically within minutes and without the need for sophisticated laboratory equipment. These kits often use lateral flow assays, immunochromatographic strips, or rapid molecular testing methods to deliver fast and reliable results.

The Philippines pharmaceutical industry stands as one of Southeast Asia's most dynamic and rapidly expanding healthcare markets in the ASEAN region. With a market valuation reaching USD 3.36 Billion in 2025, the sector demonstrates resilience and tremendous growth potential.

Pharmaceuticals are medical products, substances, or formulations involved in the development, manufacture, and regulation for the prevention, diagnosis, treatment, and management of diseases in humans as well as animals.

The Australia aged care industry stands at a pivotal juncture as the nation grapples with demographic shifts that are reshaping the landscape of elderly care services. With an aging population that continues to expand, Australia faces both unprecedented challenges and remarkable opportunities in delivering quality care to its senior citizens.

The Indian vaccines industry holds an unparalleled position globally, often celebrated as the pharmacy of the world due and its massive production scale and capabilities. It reached INR 113.7 Billion in 2024 according to IMARC Group and it is projected to grow at a CAGR of 8.8% from 2025-2033.

The medical imaging market has reached a transformational phase, driven both by rapid technological advancements and growing demands for precision-driven diagnostics. As health systems worldwide come under increasing pressure to improve patient outcomes while minimizing procedural risks and optimizing clinical workflows, medical imaging has become one of the most important cornerstones of modern medicine.

India’s medical devices industry is on a sustained growth trajectory driven by expanding hospital infrastructure, rising chronic disease burden, stronger local manufacturing supported by government incentives, and a rapidly growing shift toward portable and home care devices.

Pectin represents a naturally occurring polysaccharide mainly extracted from cell walls of fruits (mainly from citrus peel and apple pomace). It is a soluble dietary fiber and a hydrocolloid with gelling, thickening, and stabilizing properties. It is mostly composed of galacturonic acid units.

Paracetamol, also referred to as acetaminophen, is an analgesic and antipyretic compound that is commonly used worldwide for the treatment of mild to moderate pain and the management of fever. The mechanism of action occurs mainly in the central nervous system, where it inhibits the mechanisms that regulate pain and body temperature, but lacks anti-inflammatory properties.

The Australia wellness tourism industry has emerged as a critical segment of the country’s broader travel and hospitality sector. It reflects a growing global emphasis on health, self-care, and holistic well-being, capturing the attention of travelers seeking experiences that combine relaxation, rejuvenation, and personal growth.

The Brazil cardiovascular devices market represents a crucial segment in the country’s healthcare ecosystem, addressing one of the leading causes of morbidity and mortality: cardiovascular diseases. Conditions such as heart attacks, stroke, arrhythmias, and heart failure require ongoing medical intervention and advanced heart disease treatment solutions. With the rising prevalence of cardiovascular disorders, demand for comprehensive cardiac care equipment and innovative treatment modalities is increasing.

India's Ayurvedic products market is experiencing remarkable transformation as consumers increasingly prioritize holistic wellness and natural remedies over conventional alternatives. The convergence of traditional healing wisdom with modern consumer preferences has created a dynamic landscape where herbal medicines, chemical-free personal care products, and immunity-boosting supplements are becoming household staples.

Nicotine pouches are small, smokeless oral delivery products of nicotine, free from tobacco, designed to allow for controlled release of the active principle without burning, vaporizing, or use of traditional tobacco leaves. It consists of a small pouch that contains a matrix made basically from plant fibers, flavorings, pH adjusters, and stabilizers impregnated with nicotine, encased in a permeable material permitting the gradual absorption of the product via the oral mucosa.

The pharmaceutical industry in Japan is among the most advanced globally, recognized for combining innovation, high-quality standards, and patient-centered care. Its extensive value chain includes drug discovery, clinical trials, manufacturing, distribution, marketing, and post-market surveillance. Serving both domestic and international markets, Japanese pharmaceutical companies are respected for regulatory compliance, safety, and reliability, establishing them as trusted global collaborators in drug development.

The pharmaceutical industry in Japan is among the most advanced globally, recognized for combining innovation, high-quality standards, and patient-centered care. Its extensive value chain includes drug discovery, clinical trials, manufacturing, distribution, marketing, and post-market surveillance. Serving both domestic and international markets, Japanese pharmaceutical companies are respected for regulatory compliance, safety, and reliability, establishing them as trusted global collaborators in drug development.

The global healthcare IT industry is on a remarkable upswing, fueled by the surge in preventive care, digital health platforms, and smarter patient management systems. According to IMARC Group, the market hit USD 363.15 Billion in 2024, a clear sign of worldwide adoption. An aging population, the growing comfort with remote care, and the push toward personalized medicine are all speeding this momentum.

The global endoscopy devices market is on a sharp growth path, fueled by the shift toward minimally invasive procedures, the need for early diagnosis, and cutting-edge imaging technologies. IMARC Group reported the market hit USD 50.01 Billion in 2024, underscoring its worldwide acceptance.

The global business-to-business (B2B) payments landscape is experiencing a fundamental transformation that is reshaping how enterprises conduct financial transactions across borders and industries. The market, valued at approximately 1,189.6 Billion in 2024, is projecting remarkable growth with expectations to reach USD 2,189.0 Billion by 2033, exhibiting a CAGR of 7% from 2025-2033. This exponential expansion is signaling a paradigm shift in commercial finance, driven by technological innovation, changing business expectations, and the urgent need for more efficient payment infrastructures.

The smart medical devices market is entering a decade defined by connected care, real-time diagnostics, and patient empowerment. Valued at USD 45.9 Billion in 2024, the market is projected to reach USD 82 Billion by 2033, expanding at a compound annual growth rate (CAGR) of 6.33% between 2025 and 2033 by IMARC Group. This steady rise reflects growing confidence in data-driven healthcare systems, integration of IoT in medical environments, and the increasing role of artificial intelligence in clinical decision-making.

Active Pharmaceutical Ingredients (APIs) are the bioactive molecules of any drug used in pharmaceuticals, which cause the desired therapeutic action in the body of a human being. APIs are the central core of all drugs, chemical or biological and are responsible for the efficacy, strength, and safety of the drug. APIs are synthesized by various complex chemical synthesis, fermentation, biotechnological, or extraction processes based on the type of drug.

A bio medical incinerator is a high-temperature combustion system specialized for biomedical waste disposal by hospitals, clinics, laboratories, and research institutions. Biomedical waste usually consists of infectious waste, pathological waste, sharps, pharmaceuticals, and contaminated disposables that are very hazardous to human health and the environment if not treated.

Obesity, once viewed primarily as a lifestyle choice, is now widely recognized as a complex and chronic disease characterized by excessive body fat accumulation. Its global prevalence is escalating at an alarming rate posing a significant and growing challenge to public health systems worldwide.

Gonorrhea, a sexually transmitted infection caused by the bacterium Neisseria gonorrhoeae, is a major public health issue globally. Reports show that over one million new cases of curable STIs are contracted every day by individuals aged 15 to 49 years, with the majority being asymptomatic.

The 7 major allergic conjunctivitis markets reached a value of USD 2.1 Billion in 2024. Looking forward, IMARC Group expects the 7MM to reach USD 2.9 Billion by 2035, exhibiting a growth rate (CAGR) of 3.00% during 2025-2035.

The healthcare sector is changing rapidly because of the growing demand for better ways to manage chronic diseases. As we move toward 2025 and beyond, digital tools are playing an important role in dealing with conditions like diabetes, heart disease, cancer, and respiratory problems.

The global multivitamin gummies market consists of chewable dietary supplements that are charged with key vitamins and minerals aimed at maintaining general health and wellness. The gummies present a handy, enjoyable, and easy-to-swallow option to classic pills or tablets, hence are predominantly preferred by children and adults who do not like taking pills.

India's pharmaceutical sector is evolving rapidly, supported by the integration of artificial intelligence (AI) across the value chain. As of 2023, India ranked as the third-largest pharmaceutical producer by volume, accounting for 20% of global generic drug exports.

As Lung Cancer Awareness continues to build global momentum in 2025, Artificial Intelligence (AI) is proving to be a transformative force—not only in clinical diagnostics but also in public education and preventive health efforts. Given that lung cancer remains one of the world’s deadliest cancers, accounting for over 1.8 million deaths each year and a five-year survival rate of just 28.4%, the integration of AI marks a critical turning point.

Observed on May 19, Hepatitis Testing Day 2025 emphasizes the need to "Test. Treat. Eliminate," highlighting the gap in diagnosing hepatitis B and C, which cause over 1.3 million deaths annually. Hepatitis remains a major global health threat, on par with HIV, tuberculosis, and malaria. The growing viral hepatitis market <Viral Hepatitis Market Size | Share, Trends - 2034 > reflects rising demand for better diagnostics, treatments, and integrated care. The WHO warns that without faster testing and treatment, the goal of eliminating hepatitis by 2030 may not be achieved, with disparities in diagnostics, particularly in low- and middle-income countries, hindering progress.

Observed on May 8, World Ovarian Cancer Day 2025 carries the theme “No Woman Left Behind,” reinforcing the urgent need to close the gaps in access, diagnosis, treatment, and care across all regions and socioeconomic groups. Ovarian cancer remains one of the deadliest gynecological cancers, often detected too late due to vague symptoms and limited screening tools. The World Ovarian Cancer Coalition projects a 55% rise in annual cases and nearly 70% more deaths by 2050, with the heaviest burden falling on low- and middle-income countries. Equitable access to early diagnostics, genetic testing, and targeted therapies is critical.

In clinics around the world, a concerning pattern is becoming increasingly evident: a growing number of patients are experiencing wheezing, breathlessness, and persistent coughing. This surge reflects a broader global trend. According to the World Health Organization (WHO), more than 260 million people are currently living with asthma, making it one of the most widespread and persistent chronic respiratory conditions globally.

Observed on April 25, World Malaria Day 2025 carries the theme “Accelerating Equity in Malaria Prevention and Cure,” underscoring the urgent need to reach communities still lacking access to life-saving vaccines and diagnostics. While global malaria death rates have seen modest declines, the disease continues to claim the life of one child every minute, highlighting the critical need for swift, equity-driven action

Sulfamethoxazole is a common synthetic antibacterial that is a member of the sulfonamide class of antibiotics. This substance plays a very significant role in modern medicine due to the amazing capabilities offered by the substance for curing infections and bacterial diseases. Trimethoprim and sulfamethoxazole are frequently used together to create the well-known antibiotic co-trimoxazole, which is well-known for its potency against a variety of bacterial infections. It works by preventing the manufacture of folic acid, which is necessary for the growth of bacteria. Sulfamethoxazole is an essential part of modern antibiotic therapy since it has been used to treat lung infections, urinary tract infections, and other common bacterial illnesses.

Healthcare consumables are necessary medical supplies used for patient treatment, diagnostics, and cleanliness in clinics, hospitals, and home care settings. These consist of supplies such as surgical masks, bandages, gloves, syringes, catheters, and disinfectants. Usually, they are disposable or single use to preserve sterility and stop infections. Healthcare consumables are an essential component of the global healthcare ecosystem and are in high demand due to expanding healthcare needs, an increase in operations, infection control measures, and technological improvements.

Catheters are flexible, tubular medical devices designed to access various body cavities, organs, or blood vessels for diagnostic or therapeutic purposes. They can be broadly classified into types based on their application, including urinary catheters, cardiac catheters, and intravenous (IV) catheters. Catheters are commonly used in diverse healthcare settings for managing chronic conditions, enabling fluid drainage, delivering medications, or facilitating minimally invasive surgeries.

Bioinformatics involves applying computational techniques and tools to study and understand biological systems at the molecular level. It is a field of study that combines mathematics, biology, computer science, and statistics to research genomic data and biological networks. The goal is to interpret information from large biological data sets, such as DNA sequences, protein structures, gene expressions, and other high-throughput experimental data. This field provides various products and services, such as knowledge management tools, bioinformatics platforms, and services.

A non-animal model refers to an experimental system or method used in scientific research or testing that does not involve the use of animals. These models are developed to simulate biological processes, test hypotheses, or study diseases without the need for live animals. The aim is often to reduce the reliance on animal testing, which has ethical implications and raises concerns about animal welfare.

Cell therapy involves the transplantation and manipulation of living cells to replace and repair damaged tissue. Its primary branches include stem cell therapy and non-stem cell therapy. Stem cell therapy utilizes stem cells to repair, replace, or rejuvenate damaged or diseased cells and tissues as they possess the ability to differentiate into various specialized cell types, making them valuable for regenerative medicine. Non-stem cell-based therapies typically involve somatic cells isolated from the human body. These cells are propagated, expanded, selected, and then administered to patients for curative, preventive, or diagnostic purposes. On the other hand, gene therapy seeks to treat diseases by introducing, replacing, or inactivating genes within cells.