Key Challenges and Opportunities Shaping the Latin America Carbon Footprint Management Market

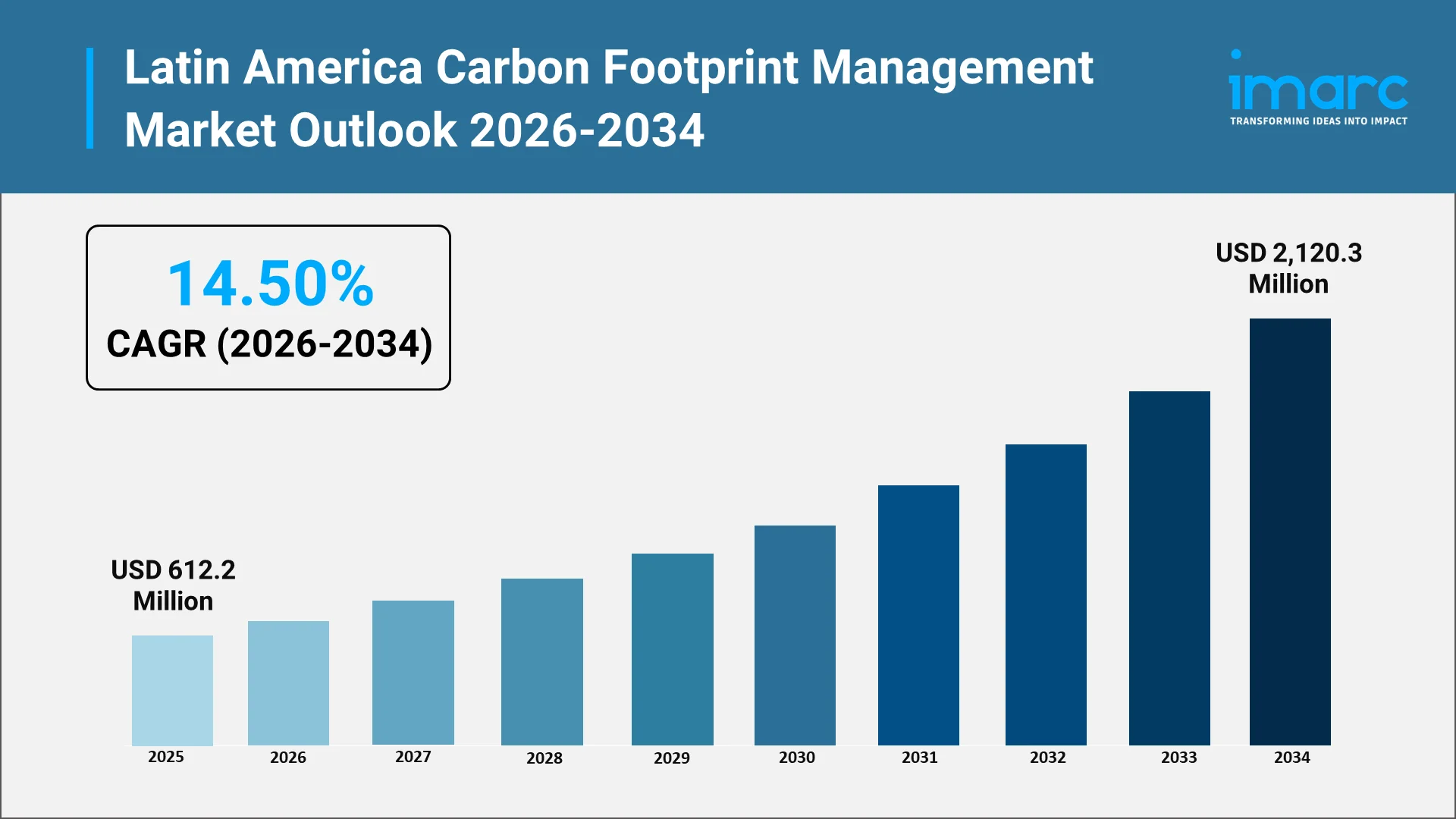

The Latin America carbon footprint management market represents a critical frontier in the global transition toward sustainable business practices and environmental accountability. As organizations across the region confront mounting pressure from stakeholders, investors, and regulatory bodies, the demand for sophisticated carbon emission tracking systems has intensified dramatically. This market encompasses a comprehensive ecosystem of technologies, platforms, and consulting services designed to measure, monitor, and reduce organizational carbon footprints while supporting compliance with evolving environmental standards. In 2025, the Latin America carbon footprint management market size reached USD 612.2 Million.

Latin American enterprises navigate a complex landscape where economic development aspirations must be balanced against urgent climate commitments. The region's diverse industrial base presents unique measurement and management challenges. Growing awareness of ESG compliance Latin America requirements is driving corporate transformation across sectors, as companies recognize that environmental performance directly influences market valuation, access to capital, and competitive positioning. Advanced sustainability analytics platforms enable unprecedented visibility into emissions across supply chains while modeling tools project financial implications of decarbonization pathways.

Overview of the Latin America Carbon Footprint Management Market:

The Latin America carbon footprint management market encompasses a comprehensive ecosystem of software platforms, consulting services, and verification providers enabling organizations to quantify greenhouse gas emissions across operational boundaries. The market serves enterprises seeking to establish baseline measurements, implement reduction strategies, and demonstrate alignment with international climate frameworks. Regional dynamics distinguish Latin America through its unique combination of resource-dependent economies and vulnerability to climate impacts, with Brazil's biofuels sector, Chile's renewable energy leadership, Mexico's manufacturing integration, and Argentina's agricultural prominence creating distinct market characteristics. IMARC Group expects the Latin America carbon footprint management market to reach USD 2,120.3 Million by 2034, exhibiting a growth rate (CAGR) of 14.50% during 2026-2034.

Market participants range from multinational corporations implementing enterprise-wide carbon accounting systems to small enterprises taking initial measurement steps. Technology providers are increasingly localizing offerings to address regional requirements including languages, currencies, and regulatory frameworks. Professional services firms are expanding capabilities to meet surging demand for strategic advisory and verification services.

Explore in-depth findings for this market, Request Sample

Market Growth and Emission Reduction Goals:

Market expansion reflects intensifying corporate commitments to achieve emission reductions aligned with climate agreements. According to the Latin American Energy Organization (OLADE), renewable energy in Latin America's electricity production increased by 4% year over year to reach 68% renewable electricity generation. Organizations are establishing ambitious carbon neutrality targets and investing in management capabilities. The momentum behind carbon offsetting initiatives demonstrates recognition that operational improvements alone cannot address required reduction scale, necessitating investment in verified offset projects.

Corporate sustainability commitments drive systematic changes in operations, procurement, and capital allocation. Leading companies implement science-based targets establishing reduction pathways consistent with temperature limitations. These commitments cascade through supply chains as buyers require suppliers to measure and report carbon footprints, creating network effects accelerating adoption. The integration of renewable energy integration strategies with carbon management platforms represents a critical growth driver. Organizations leverage modeling tools to evaluate renewable investments, assess grid impacts, and optimize energy portfolios for cost efficiency and emission reduction.

Key Challenges Facing Implementation:

Organizations encounter substantial obstacles implementing effective carbon management systems despite market momentum. Data availability and quality issues represent fundamental challenges, as enterprises lack robust systems for tracking energy consumption across value chains.

Technical capacity constraints pose significant barriers. Many organizations lack internal expertise in carbon accounting methodologies and sustainability analytics interpretation. This gap extends beyond measurement to strategic planning and stakeholder communication. Professional shortages create consultant dependency, increasing costs and limiting knowledge transfer supporting sustained efforts.

Financial considerations influence adoption timelines significantly. Initial investments in platforms, verification services, and change management can be substantial for enterprise-wide implementations. Return on investment calculations remain challenging when quantifying benefits including risk mitigation and regulatory compliance. Supply chain complexity creates difficulties measuring Scope 3 emissions comprehensively, with companies participating in global value chains where suppliers operate across jurisdictions with varying transparency levels.

Opportunities in Corporate Sustainability and Technology:

The expanding emphasis on ESG compliance Latin America creates substantial opportunities for market participants. Investors increasingly incorporate environmental performance into valuation models, creating financial incentives for robust carbon management. Companies demonstrating leadership experience improved capital access, lower borrowing costs, and enhanced valuations, positioning carbon management as strategic capability rather than compliance function.

Technological advancement democratizes access to sophisticated capabilities. Cloud-based platforms with intuitive interfaces reduce implementation complexity. Artificial intelligence applications enhance data collection automation, improve emission factor accuracy, and enable predictive analytics. Regional carbon offsetting market development presents significant opportunities, as Latin America's forests and renewable energy potential provide advantages for developing quality offset projects. Organizations increasingly seek locally sourced offsets delivering co-benefits including biodiversity protection and community development, stimulating verification infrastructure investment.

Cross-sector partnerships accelerate decarbonization at scale. Industry associations develop sector-specific protocols and share best practices reducing implementation costs. Public-private collaborations create shared monitoring infrastructure, enabling resource pooling and knowledge transfer benefiting entire industries.

Government Initiatives and Green Regulations:

Government action establishes regulatory frameworks mandating or incentivizing corporate carbon management. ECLAC's November 2025 report highlights that climate action offers opportunities for spurring growth, creating jobs, and enhancing international positioning. National climate strategies translate international commitments into domestic policies affecting businesses directly. Regulatory approaches vary significantly, with jurisdictions implementing mandatory reporting requirements or focusing on voluntary mechanisms supported by incentives and technical assistance programs.

Carbon pricing mechanisms emerge as policy instruments in major economies. These systems create explicit financial incentives for emission reductions by establishing economic costs for pollution. Pricing mechanisms drive demand for robust measurement capabilities enabling organizations to determine obligations and identify cost-effective opportunities. Regulatory harmonization efforts gradually reduce cross-border compliance complexity, with international standards influencing national approaches and creating consistency in measurement methodologies and verification protocols.

Government support programs address implementation barriers through financial assistance and technical training. Development banks offer concessional financing for carbon management investments targeting small and medium enterprises. Public institutions develop emission factor databases and guidance documents reducing adoption costs, accelerating market development by lowering barriers.

Competitive Insights and Future Prospects:

The competitive landscape features diverse participants from established global vendors to specialized regional providers. International firms adapt platforms for Latin American requirements through local partnerships and language support. Homegrown providers leverage deep knowledge of local business practices and regulatory environments to capture market share among enterprises prioritizing regional expertise.

Strategic differentiation centers on integration capabilities connecting carbon management with enterprise systems. Leading platforms incorporate APIs and connectors synchronizing with financial systems and supply chain applications. This integration reduces manual entry and enables frequent reporting. Organizations prioritize solutions offering seamless connectivity over standalone applications requiring parallel data collection efforts.

Future market evolution will be shaped by converging trends. Artificial intelligence will enable sophisticated predictive modeling and automated anomaly detection. Blockchain may enhance offset market verification while reducing transaction costs. Internet of Things sensors will provide real-time monitoring at granular levels, moving toward continuous measurement systems supporting dynamic decisions. The expansion of renewable energy integration throughout electricity grids will fundamentally alter corporate footprints, requiring organizations to adapt approaches to reflect evolving grid emission factors and renewable procurement tracking.

Stakeholder expectations regarding transparency will continue intensifying. Investors demand granular disclosure including Scope 3 emissions and transition planning. Consumers increasingly consider environmental performance in purchasing decisions. Employees prioritize environmental values when evaluating employers. These pressures will sustain demand for comprehensive capabilities while raising credibility standards.

.webp)

Conclusion:

The Latin America carbon footprint management market stands at a pivotal juncture where environmental imperatives, regulatory evolution, and business strategy converge to create unprecedented momentum. Organizations throughout the region are recognizing that effective carbon management represents not merely a compliance obligation but a strategic capability that influences financial performance, competitive positioning, and long-term resilience. The challenges of data availability, technical capacity, and financial resources remain significant, yet the opportunities emerging from technological innovation, supportive policies, and stakeholder engagement provide compelling pathways forward.

Success in this evolving landscape requires organizations to move beyond viewing carbon footprint management as a standalone environmental initiative. Leading companies are integrating carbon emission tracking into core business processes, embedding sustainability considerations into strategic planning, capital allocation, and performance management. This transformation demands investment in enabling technologies, development of internal capabilities, and cultivation of organizational cultures that value environmental stewardship alongside traditional business metrics.

The trajectory of the Latin American market suggests continued expansion as regulatory frameworks mature, technological capabilities advance, and stakeholder expectations intensify. Organizations that establish robust carbon management foundations today will be positioned to navigate future regulatory requirements, capture emerging commercial opportunities, and demonstrate leadership in the transition toward a low-carbon economy. The question facing Latin American businesses is not whether to invest in carbon footprint management capabilities, but rather how quickly they can build the systems, expertise, and partnerships necessary to thrive in an increasingly carbon-constrained world.

Choose IMARC Group for Unmatched Expertise:

- Data-Driven Market Intelligence: Enhance your understanding of carbon footprint management adoption patterns, technology innovations, and regulatory developments throughout Latin America through comprehensive research reports.

- Strategic Growth Forecasting: Anticipate emerging trends in sustainability analytics, carbon offsetting mechanisms, and corporate environmental disclosure by analyzing regional market dynamics and stakeholder expectations.

- Competitive Intelligence: Evaluate competitive positioning within the carbon management ecosystem, assess technology provider capabilities, and identify strategic partnership opportunities that accelerate market entry.

- Policy and Regulatory Advisory: Navigate evolving carbon pricing mechanisms, mandatory reporting requirements, and voluntary disclosure frameworks affecting organizational compliance obligations across Latin American jurisdictions.

- Custom Research and Consulting: Access tailored insights addressing your organizational objectives, whether launching carbon solutions, investing in sustainability technologies, or developing decarbonization strategies that drive outcomes.

For more detailed report, please visit: https://www.imarcgroup.com/latin-america-carbon-footprint-management-market

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

The UK's ATM market, therefore, stands as an important pillar in its financial ecosystem for the benefit of millions of consumers and businesses who rely on timely, convenient, and secure ways of accessing cash. However, despite the rapid acceleration of contactless payments and digital banking, ATMs remain indispensable across the urban and rural areas.

The India smartphone industry has cemented its position as one of the world's most critical and dynamic technology markets, undergoing a profound transformation driven by consumer aspiration and technological advancement. Far from merely being a volume-driven segment, the market is experiencing a significant value premiumisation trend, where consumers are increasingly upgrading to feature-rich and higher-priced devices.

India is now undergoing a transformative phase of the Internet of Things (IoT) industry, as it solidifies its role as a key facilitator of the ambitions of the Indian economy to become digital. IoT, which was initially viewed as a futuristic idea, has quickly become a baseline technology in the consumer, enterprise, and public infrastructure domains.

As banks and startups embrace modernization, secure and efficient digital platforms are attracting strong local and global investment. Artificial intelligence (AI), automation, and predictive analytics are redefining how finance works in Australia. These tools make transactions faster, decisions sharper, and client experiences more intuitive. From fraud detection to personalized banking, technology is transforming every corner of the market.

The Europe artificial intelligence market stands at a pivotal juncture, balancing unprecedented technological advancement with complex regulatory frameworks and strategic imperatives. As businesses across the continent accelerate their AI adoption Europe initiatives, the region emerges as a distinctive force in global artificial intelligence development, characterized by its commitment to ethical innovation and human-centric technologies.

India’s rapid digitalization has transformed the way organizations operate, connect, and deliver services. However, this digital shift has also exposed enterprises to a surge in cyber threats, ranging from ransomware and phishing to sophisticated data breaches and identity theft. As companies across sectors increase their reliance on digital platforms, the frequency and complexity of cyberattacks have intensified, forcing both public and private institutions to prioritize cybersecurity investments.

The Europe drones market has evolved into an indispensable aspect of the continent's operational and technological environment. Drones are now sequentially incorporated into sectors that rely on precision, real-time monitoring, and safe performance of field operations. Their capacity for aerial monitoring, environmental condition evaluation, and real-time observation allows companies to achieve greater accuracy in decision-making while reducing reliance on human intervention in hazardous areas.

The 3D printing industry is currently experiencing a revolutionary growth that has had a radical change on the manufacturing operations within the industries of the world. The technology is also referred to as additive manufacturing (AM), and it is the way to create three-dimensional objects by adding layers to the digital model, thereby providing unprecedented flexibility in both design and production. The 3D printing sector of the world has become a pivotal source of innovation enabler, efficiency, supply chain resilience, and competitive edges to organizations as small-and-medium-sized as small businesses to Fortune 500 organizations.

The education sector in India is witnessing a sea change with digital learning becoming integral to both formal and informal education. The rapid rise of online education platforms has reshaped the way schools, coaching institutes, and higher education centers impart learning experiences, accelerated by pandemic-driven digital acceleration. And today, technology-enabled education is no longer confined to urban centers; it is reaching Tier-2 and Tier-3 cities, democratizing access to quality learning resources for millions of students.

India’s healthcare sector is undergoing a technological transformation, with artificial intelligence positioned as a central driver of change. With a population exceeding 146.39 crore and a system challenged by issues of accessibility, affordability, and quality, AI is no longer optional but essential for building sustainable healthcare solutions.

India health and wellness market is on a fast track, with more people paying attention to preventive care and overall well-being. IMARC Group stated that the market hit USD 156.01 Billion in 2024, owing to the boom in nutraceuticals, fitness, and digital health platforms. Artificial intelligence (AI) is bringing a fresh wave of innovation to health and wellness, enhancing personalized fitness routines, predictive health insights, and more efficient wellness tracking.

Japan's ecotourism industry is experiencing a remarkable transformation, positioning the country as Asia's leading destination for sustainable travel experiences. The market, which is reaching unprecedented valuations of USD 12,999.78 Million in 2024, is demonstrating exceptional growth momentum with projections indicating an expansion to USD 34,542.85 Million by 2033, representing a robust compound annual growth rate (CAGR) of 11.47% during the 2025-2033 period.

The United Kingdom is currently establishing itself as one of Europe's most dynamic blockchain innovation hubs, demonstrating remarkable resilience and growth despite global economic uncertainties. The UK blockchain market reached a valuation of USD 0.66 Billion in 2024 and is projecting explosive growth toward USD 54.63 Billion by 2033, exhibiting a compound annual growth rate (CAGR) of 63.26% during the forecast period. This extraordinary trajectory is placing the nation at the forefront of distributed ledger technology adoption and development.

Japan has been a world leader in robotics, especially industrial, for decades. The nation's unflinching faith in technology development, precision manufacturing, and automation has made it a world leader in industrial robotics. Industrial robots have transformed the manufacturing process to become necessary equipment in today's manufacturing, helping companies increase productivity, retain quality, decrease errors in operations, and enhance efficiency in processes.

The Europe 3D printing market stands at the forefront of a manufacturing revolution that is reshaping industries across the continent. As additive manufacturing technologies mature and expand beyond prototyping into full-scale production, European manufacturers, healthcare providers, and aerospace companies are increasingly embracing these transformative solutions. With substantial government backing, strategic industry collaborations, and breakthrough material innovations, the European 3D printing landscape is positioned for remarkable expansion through 2033.

The Philippines gaming industry has emerged as Southeast Asia's fastest-rising digital entertainment powerhouse, achieving USD 4,822.00 Million in gross gaming revenue for 2024. This explosive growth signals a fundamental transformation in how Filipinos engage with interactive entertainment, driven by the rapid adoption of augmented reality (AR) and virtual reality (VR) technologies.

The data monetization market has emerged as a critical pillar of the modern digital economy, transforming how organizations create value from their information assets. As businesses recognize data as a strategic asset, the ability to extract financial value has become a competitive imperative. The global data monetization industry encompasses diverse approaches, ranging from direct data sales to indirect monetization through enhanced decision-making. According to IMARC Group, the industry reached USD 4.1 Billion in 2024. It is projected to reach USD 16.1 Billion by 2033, at a CAGR of 15.76% during 2025-2033.

The global access control market is entering a phase of serious expansion and transformation. In 2024, IMARC placed its value at USD 10.6 Billion, with a forecast of USD 18.8 Billion by 2033 (CAGR of 6.5 %). This reflects how rapidly the underlying technologies, threat landscape, and regulatory regimes are shifting. Across enterprises, campuses, infrastructure sites, and smart buildings, access control is evolving from door-level locks to identity, context, behavior, and integration. In many markets, access control is becoming an essential bridge between physical security and cybersecurity.

The media consumption landscape in Japan is in the midst of a revolutionary change with over-the-top (OTT) services as a leading force behind the way viewers are consuming entertainment content. OTT services, which provide video content directly on the internet and not via conventional cable or satellite television, are fast becoming a standard in Japanese homes. The growth of the Japanese OTT industry has been shaped by various factors, from technological innovations to changing consumer tastes.

The e-commerce market in Mexico is thriving, driven by increased internet access, mobile shopping, and smooth digital payment options. IMARC Group estimated that the market reached an impressive USD 47.52 Billion in 2024, signifying a distinct transition towards online shopping.

The global Industry 4.0 market is experiencing strong momentum, propelled by the integration of smart technologies across manufacturing, logistics, and energy sectors. With automation, connectivity, and data intelligence at its core, Industry 4.0 is reshaping how enterprises design, produce, and deliver products.

The global soft skills training market size was valued at USD 33.39 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 92.59 Billion by 2033, exhibiting a CAGR of 11.40% during 2025-2033. This substantial growth reflects a fundamental shift in how organizations approach workforce development, as the recognition of soft skills as strategic assets rather than supplementary competencies becomes universal across industries.

The global Wi-Fi infrastructure market is experiencing unprecedented expansion, fundamentally reshaping how organizations operate and consumers interact with technology. According to Wi-Fi Alliance, the official industry certification body, 4.1 Billion Wi-Fi devices are forecast to ship in 2024, contributing to 45.9 Billion cumulative Wi-Fi shipments over the technology's 25-year lifetime.

Australia's mobile money industry is experiencing unprecedented transformation as artificial intelligence reshapes the landscape of digital payments, mobile wallets, and financial services. The integration of sophisticated AI technologies has revolutionized how Australians conduct transactions, manage their finances, and interact with digital payment platforms. From smartphone-based payment solutions to advanced fraud detection systems, AI is driving innovation across every facet of the mobile money ecosystem.

India vehicle tracking market is undergoing a significant transformation, with artificial intelligence emerging as a central driver of innovation. According to the IMARC Group’s report, the market size reached USD 0.90 Billion in 2024.

India stands at a decisive stage where economic growth must advance in parallel with environmental sustainability. According to an IMARC Group report, the Indian green technology and sustainability market reached USD 837.2 Million in 2024, reflecting the nation’s growing commitment to sustainable development.

Closed-Circuit Television (CCTV) cameras are electronic monitoring systems that are used to watch, record, and send video images for security and observational reasons. Unlike television broadcasting, CCTV signals are sent to selected monitors or recording devices, and hence they are the backbone of contemporary security infrastructure.

India's educational technology sector stands at the precipice of a transformative revolution, with artificial intelligence (AI) emerging as the primary catalyst driving unprecedented growth and innovation. The convergence of AI technologies with educational platforms is fundamentally reshaping how millions of Indian students access, consume, and engage with learning content, creating an ecosystem that democratizes access to quality education across the country’s diverse linguistic and socioeconomic groups.

Japan’s higher education sector is at a major turning point as demographic and economic pressures converge with technological disruption. One of the major trends in the Japan higher education market include the number of students entering universities has been shrinking for decades due to the country’s aging population, creating structural challenges for institutions that once relied on a stable or growing pool of applicants.

Japan, a global leader in technological innovation, is at the forefront of a new digital revolution in its satellite communication sector. As the nation pushes toward a more connected and resilient future, the integration of Artificial Intelligence (AI) is proving to be a critical catalyst. From enhancing network performance to automating complex operations AI is not just an add-on it is a foundational technology reshaping the very fabric of satellite communication.

Generative artificial intelligence (AI) is rapidly becoming one of the most influential technologies of the decade, and its global footprint is continuously expanding. Nations across the world are exploring its transformative potential, with Japan emerging as a unique hub where technological innovation, traditional industries, and forward-looking government policies are converging.

A battery charger is a piece of electrical equipment that is used to recharge a rechargeable battery by imposing an electric current upon it. The main purpose of a charger is to transfer alternating current (AC) from the power source into an appropriate direct current (DC) that has the required voltage and current for the particular type of battery. Battery chargers play a vital role in a broad variety of applications, from consumer devices and electric vehicles (EVs) to industrial equipment and renewable energy systems.

Indian manufacturing continues to grapple with significant losses caused by defects, rework, and product returns, which weaken profitability and competitiveness. As per an industry report, in FY22, the total return order volume in India stood at 14.86%. Furthermore, high-volume industries such as automotive, FMCG packaging, textiles, and electronics are particularly exposed, where even a small defect rate can translate into substantial financial setbacks. Industry research states that in mature operations, the Cost of Poor Quality (COPQ) can account for as much as 15–20% of total sales. Moreover, Return Prime’s recent report shows that returns remain a major challenge in e-commerce sales, with 17.6% of all orders being sent back.

Industry 4.0 has been a defining milestone in the advancement of manufacturing. It is responsible for introducing automation, digitization, and data-driven processes that significantly enhanced productivity and precision. Presently, India is moving into the next phase of manufacturing, that is, autonomous factories. Here, artificial intelligence (AI) goes beyond simple automation, enabling systems to render decisions, learn from changing conditions, and continuously improve operations. This shift has the potential to reshape industrial growth in the country and establish new standards for smart manufacturing.

Indian manufacturers are facing difficulties due to rising input costs, shortages of skilled labour, unplanned machine downtime, and inconsistent product quality. According to an industry report, during the July–September quarter of FY25, raw material expenses for 1,679 listed non-financial manufacturing companies increased by 5.1%, outpacing sales growth, which rose by only 3.3%. Similarly, the Global Talent Shortage Survey 2025 reported that 80% of Indian employers report difficulty finding skilled talent, compared to the global average of 74%, highlighting a severe talent crunch.

According to the International Energy Agency (IEA), global energy-related CO2 emissions grew by 0.8% in 2024 to a record 37.8 gigatonnes, driving atmospheric concentrations to an unprecedented 422.5 ppm. This has led to an increased urgency in addressing climate change. Similarly, the industries are facing unprecedented pressure to rethink their operations due to the energy demand rising by 2.2% in 2024, which is faster than the annual average of 1.3% witnessed between 2013 and 2023.

India is among the fastest-growing economies globally. The nation is currently the fourth-largest economy in the world and is on its way to becoming the third-largest, with an estimated GDP of USD 7.3 Trillion by 2030. This momentum is not only strengthening India’s economic resilience but also opening lucrative opportunities for businesses, investors, and technology providers aligned with the country’s growth vision.

The role of artificial intelligence (AI) in modern project management has transitioned from a theoretical concept to a strategic imperative. As businesses navigate increasingly complex projects in a data-driven world, AI is emerging as a powerful force for efficiency, accuracy, and innovation.

The artificial intelligence market is no longer niche. Current projections value the market at a significant level today, with strong growth expected as generative AI matures, computing costs decline, and enterprise pilots scale into full production.

The data center sector in Japan is at the epicenter of a tech revolution, wherein artificial intelligence (AI) is fundamentally redefining how digital infrastructure manages, scales, and adapts. With the country progressing toward digital transformation in various industries, AI has been the force behind unprecedented innovation in the design, management, and optimization of data centers.

In the modern era, the global video streaming market is fundamentally reshaping the entertainment landscape, driven by the dual forces of digitalization and the escalating demand for on-demand content. Artificial intelligence (AI) also serves as a pivotal catalyst for this growth, enabling the personalization of user experiences through tailored recommendations, improved content discovery, and enhanced audience engagement.

The global gaming console market is undergoing a significant transformation, fueled by the adoption of artificial intelligence (AI) and an increasing demand for interactive entertainment.

For decades, call centers have played a central role in customer service. Traditionally staffed with large teams of agents, they operated as cost-heavy units designed to handle inquiries, complaints, and service requests. While essential, this model was often associated with inefficiencies, long wait times, and high employee turnover.

According to IMARC Group, the global identity verification market was valued at USD 13.8 Billion in 2024 and is projected to reach USD 46.4 Billion by 2030, expanding at a CAGR of 14.4% during 2023–2030. This strong growth is being fueled by the increasing adoption of artificial intelligence (AI) and machine learning (ML), which are enabling higher levels of automation, fraud detection, and real-time authentication.

Japan is a leader in digital transformation, known for being one of the most advanced nations in technology globally. Artificial Intelligence (AI) is becoming an integral force across various sectors, and the telecom industry is no exception.

Generative AI is revolutionizing industries by bringing fresh, game-changing solutions that boost creativity and streamline workflows. Whether it’s automating content creation or optimizing complex processes in fields like healthcare and finance, AI is opening doors to exciting new possibilities.

The e-commerce market has undergone a seismic shift in the past twenty years. What started as simple, text-based product pages has grown into a complex web of intelligent platforms capable of customizing experiences for every individual user. At the core of this evolution is Artificial Intelligence (AI).

The global laptop and tablet market includes portable computing devices for both personal and commercial use, providing mobility, flexibility, and connectivity. Laptops extend desktop computers' power and functionality in a portable package, while tablets provide light-touch screen interfaces for consumption of media, creative work, and on-the-go productivity.

The global cloud gaming industry is experiencing an unprecedented surge, driven by technological advancements and evolving consumer preferences. As the market expands, Artificial Intelligence (AI) stands out as a pivotal force, reshaping every facet of the cloud gaming landscape, from infrastructure to player experience. It enables smarter resource allocation, real-time content personalization, latency reduction, and advanced game logic.

The global power bank market is experiencing steady growth as digital lifestyles become more integrated into everyday routines. With rising dependence on smartphones, tablets, laptops, and wearables, power banks have shifted from being simple backup batteries to versatile, feature-rich accessories that fulfill the needs of a wide range of users. Consumers now prefer power banks with fast-charging capabilities, higher battery capacity, and environmentally responsible designs.

The hybrid cloud market across the world has been changing at a very fast rate, with companies globally adopting the mix of on-premises and cloud-based infrastructures to fuel innovation and operational effectiveness.

Japan’s artificial intelligence (AI)-driven three-dimensional (3D) printing startups are redefining manufacturing by merging speed, sustainability, and precision. Japan’s additive manufacturing scene is moving beyond prototypes—it's rewriting how industries build, design, and innovate.

As a global leader in technology and innovation, Japan has increasingly recognized the critical importance of cybersecurity to protect its digital infrastructure.

Electric cables or power cables are the fundamental parts employed for the transfer of electrical power or signals over short and long distances. They generally comprise one or more conductors, typically composed of copper or aluminum, covered with insulating materials and protective sheaths. Electric cables, based on their use, differ in structure, including low-voltage, medium-voltage, and high-voltage power cables, control cables, instrumentation cables, or data transfer cables like fiber optics.

Smart Factory and Industry 4.0 Integration is a comprehensive set of services that helps firms overhaul their manufacturing processes by embracing new technologies such as the Internet of Things (IoT), Artificial Intelligence (AI), robotics, big data analytics, and cloud computing.

Digitalization is reshaping the very essence of travel, transforming it into a more personalized, convenient, and efficient experience than ever before. With the growing popularity of travel platforms, travelers now have the power to plan and book their entire journey with just a few taps on their smartphones.

Product and facility certification support offers professional assistance to companies in resolving complicated processes of product certification and facility certification. Our services facilitate adherence to global standards and regulatory guidelines to ensure hassle-free market entry and operational continuity across global markets.

The global e-commerce landscape is rapidly transforming, propelled by several evolving e-commerce industry trends. These fundamental shifts encompass changes in consumer behavior, rapid technological advancements, and increasing internet accessibility worldwide. As a direct result, brands are now prioritizing quick delivery, mobile-centric platforms, and deeply customized digital experiences.

Setting up a drone manufacturing plant with a step-by-step business plan covering setup, costs, equipment, compliance, and market strategy.

India’s textile industry is undergoing a transformative shift led by the government’s visionary PM MITRA (Mega Integrated Textile Region and Apparel) Parks initiative. With a mission to establish India as a worldwide leader in textiles, this program is creating world-class integrated manufacturing zones that drive innovation, reduce production costs, and boost sustainability.

India’s sports technology sector is gaining extraordinary momentum, driven by the digitalization of sports leagues, enhanced fan engagement, and increasing investments in athletic performance solutions. With the Indian Premier League (IPL) 2025 poised to become the most tech-driven tournament to date, the market is no longer restricted to wearables and broadcasting; it now powers every aspect of sports, from grassroots training to AI-based strategic decision-making.

India is becoming a popular location for foreign manufacturers because of its quickly expanding economy, affordable labour costs, and consistent government support. For businesses looking to establish manufacturing facilities in the nation, the Government's "Make in India" incentive program offers an alluring alternative. This guide will assist in comprehending the crucial requirements for setting up a manufacturing facility in India.

Factory audits are important for companies that intend to ensure compliance and quality in operations as well as supply chain efficiency. India is experiencing unparalleled growth in manufacturing. The skills to perform factory audits effectively can be used to counter most risks related to Indian supplier relationships. This blog gives a complete step-by-step guide on how to perform factory audits in India, including a complete checklist.

Establishing a manufacturing plant is a major investment that requires meticulous planning and a thorough understanding of the associated costs. Whether a seasoned entrepreneur or an industrial novice, understanding the "cost equation" is vital for making informed financial decisions and ensuring the long-term profitability of the operations. This blog will break down the various expenses associated with establishing a manufacturing facility in India.

Setting up a manufacturing plant is a significant milestone for any business, but it comes with complexities that require careful planning, research, and execution. From selecting the right location to ensuring regulatory compliance and operational efficiency, every aspect needs expert attention to guarantee success. This is where IMARC Group steps in, offering comprehensive pre-feasibility studies and consultation services to help businesses establish manufacturing plants seamlessly.

The manufacturing sector is a cornerstone of India's economy. It accounted for about 14% of the overall GDP of the nation in 2024 and has employed millions of people across the country. India has been a rising manufacturing powerhouse globally and 2025 is expected to be a turning point. Given the better government focus and strong labor force, along with the increasingly effective infrastructure, India is likely to be sealed as a prime destination for global manufacturers.

Many have encountered this scenario: visiting a website with enthusiasm to purchase a product seen in an advertisement, only to face challenges such as navigating a complex interface, unresponsive customer service, and a cumbersome checkout process.

The OTT industry is experiencing a pivotal transformation, signaling the advent of a new digital entertainment era. Consumers are increasingly demanding convenience and personalized experiences on OTT platforms. As a result, platforms are investing massively in technologies such as AI to enhance the recommendations of content and improve user experience.

From established giants in the United States and Europe to fast-paced markets in Asia, the e-commerce revolution is creating a competitive marketplace that transcends geographical boundaries. Vietnam stands out as a key force in this global trend, showcasing the potential of e-commerce to drive national economic transformation. The country’s e-commerce industry is witnessing tremendous growth, driven by new markets and growth opportunities in established markets.

Head-mounted displays consist of small displays with in-built sensors and optics that project images directly onto the user's eyes. They provide a virtual reality (VR) or augmented reality (AR) experience that allows users to interact with digital objects or environments. They resemble glasses or goggles and are designed to be worn on the head. They comprise many components, such as a controller, sensor, camera, lens, goggles, head tracker, case, connector, display, battery, processor, memory, pico projector, and accessories. Tracking systems and sensors detect the user's head movements and adjust the displayed content accordingly, offering the user a more realistic, immersive, and interactive experience.

5G technology or fifth-generation wireless technology is the latest advancement in mobile communication systems that provides enhanced data transfer speeds, reduces latency rates, improves reliability, and increases network capacity. This technology operates in the mm-wave spectrum, the spectrum band ranging from 30 to 300 gigahertz (GHz), which facilitates high-speed networks and faster data delivery. 5G technology supports the growth of emerging technologies like artificial intelligence (AI), machine learning (ML), and edge computing, enabling new business models and unlocking economic potential. It enhances the performance of business applications and digital experiences, such as video conferencing, online gaming, live streaming media, and self-driving cars. The components included in 5G technology are hardware, software, and services, and it is utilized in a wide range of applications, such as automation, video services, connected vehicles, smart homes, virtual & augmented reality, and monitoring & tracking. For better connectivity of networks, various industries, such as manufacturing, automotive, transportation & logistics, media & entertainment, energy & utilities, healthcare, government, and others, have deployed 5G technology extensively.

Robotics is the branch of engineering that deals with designing, constructing, and operating robots. Robots are programmable machines capable of carrying out tasks autonomously or semi-autonomously. Major types of robotics include industrial and service robots, combining elements of mechanical engineering, electrical engineering, computer science, and artificial intelligence (AI). Industrial robots encompass articulated, Cartesian, SCARA, and cylindrical robots. Service robots serve personal, domestic, and professional purposes, used in various applications, such as household tasks, entertainment, defense, fieldwork, logistics, healthcare, infrastructure, mobile platforms, and cleaning, and more. Robotics can efficiently and accurately perform tasks in environments that may be hazardous or challenging for humans. Robots reduce human labor, enhance production efficiency, lower costs, and improve product quality in various industries. Robotics is further categorized into types such as industrial robotics, food robotics, warehouse robotics, smart robotics, automotive robotics, agriculture robotics, logistics robotics, construction robotics, space robotics, and others. Nowadays, robotics has become an important part of many industries, even being used to explore deep oceans and space. Additionally, it is employed in creating autonomous vehicles, performing surgery, and conducting medical diagnoses.

Artificial Intelligence (AI) chips are designed to accelerate and optimize AI and Machine Learning (ML) workloads. The field of AI involves tasks such as pattern recognition, data analysis, and decision-making, which often require massive parallel processing. AI chips perform various tasks like deep learning, neural network processing, and other computationally intensive operations. These chips are tailored to support the parallel computing needs of AI workloads, making them well-suited for these tasks.

Oman is situated on the southeastern coast of the Arabian Peninsula. It boasts a rich cultural heritage, stunning landscapes, and a diverse range of attractions, making it an emerging destination in the tourism market. The country offers a wide array of tourist activities, including sunbathing, swimming, kitesurfing, diving, snorkeling, boating, among many others. Beach activities and kite surfing are popular in Muscat, Al Sawadi Beach, Alzaiba Beach, and Masirah Island, while desert safaris are a highlight in Wahiba Sands. Oman's rich historical heritage includes numerous UNESCO World Heritage Sites, ancient temples, forts, and palaces, such as Bahla Fort and the Archaeological Sites of Bat, Al-Khutm, and Al-Ayn.

Virtual reality (VR) gaming represents a new generation of computer games that leverage VR technology to provide high-definition visuals, spatial audio, and precise motion tracking, creating a sense of presence and immersion. VR gaming offers a 360-degree view of the virtual environment, keeping players engaged for longer periods compared to traditional gaming. Additionally, VR gaming is used in rehabilitation and the treatment of phobias, anxiety disorders, and other psychological conditions. It is also employed to train soldiers in combat scenarios, strategy, and decision-making.

Cloud computing delivers computing services over the internet, including servers, storage, databases, networking, software, analytics, and intelligence. It promotes faster innovation, flexible resource allocation, and economies of scale. Moreover, it offers numerous advantages, such as cost efficiency, mobility, scalability, reliability, and automatic software updates, among others.