Top Factors Driving Growth in the Saudi Arabia Steel Market

The Kingdom of Saudi Arabia is undergoing an unprecedented economic transformation, shifting its traditional reliance on hydrocarbon revenues toward a diverse, knowledge-based economy. Central to this monumental shift is the steel industry in Saudi Arabia, a sector that serves as a foundational pillar for virtually every national development project. The demand for steel, a universal commodity crucial for construction, manufacturing, and energy infrastructure, is experiencing a robust period of expansion. This significant upward trajectory is underpinned by a combination of ambitious government planning, massive investments in giga-projects, and a global pivot toward sustainable industrial practices. Understanding the underlying forces is key to grasping the future direction of the Saudi Arabia steel market.

Introduction to the Saudi Arabia Steel Industry:

The steel industry in Saudi Arabia has historically been a critical player in the wider Middle East and North Africa region, leveraging the Kingdom’s inherent energy advantages, particularly low-cost natural gas, to fuel energy-intensive production processes like Direct Reduced Iron (DRI). While long steel products, primarily rebar for construction, have traditionally dominated local output, the national strategy is now emphasizing high-value flat products and specialty steel grades to achieve greater self-sufficiency and enhance its global Saudi Arabia steel market share.

This repositioning is about increasing output and fundamentally about industrial quality and diversification. The industry is currently in a phase of strategic evolution, aiming to close the capacity gaps in specialized steel types that were previously met solely through imports. This strategic shift is aimed at enhancing local content and ensuring a secure supply chain for the nation’s mega-projects, which require vast quantities of high-specification steel. The robust ecosystem of local manufacturers, suppliers, and distributors is becoming increasingly sophisticated, creating a competitive environment that encourages technological adoption. This ambitious structural development indicates a strong Saudi Arabia steel market outlook for the next decade.

Explore in-depth findings for this market, Request Sample

Rising Infrastructure Development and Construction Projects:

Undoubtedly, the single most powerful catalyst for the current growth phase in the Saudi Arabia steel market is the massive wave of infrastructure and construction development sweeping across the Kingdom. At the heart of this expansion are the Vision 2030 giga-projects—new, futuristic urban centers and tourism hubs that are unparalleled in their scale and complexity. Projects like NEOM, The Red Sea Project, Qiddiya, and Diriyah, alongside the continuous development of urban centers like Riyadh and Jeddah, are consuming steel at an extraordinary rate.

These projects demand not just tonnage but also specialized structural steel, high-quality rebar, and advanced fabrication capabilities. The Saudi Arabia prefabricated building and structural steel market size reached USD 1,827.5 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 2,585.0 Million by 2033, exhibiting a growth rate (CAGR) of 3.73% during 2025-2033. The requirement for structural integrity in high-rise buildings, vast transportation networks including metros and high-speed rail, and complex industrial facilities places immense pressure and opportunity on steel producers. The sheer volume of material required for these developments is a defining factor shaping the Saudi Arabia steel market growth. The commitment to meeting aggressive construction timelines further accelerates demand for efficiently supplied and fabricated steel products, favoring suppliers with localized, responsive production and delivery mechanisms. This continuous flow of projects guarantees substantial demand for various steel grades for the foreseeable future, driving the overall steel market across the Kingdom.

Expansion of the Oil & Gas and Petrochemical Sectors:

While diversification is the goal, the traditional strengths of the Saudi economy, specifically the oil, gas, and petrochemical sectors, continue to be significant drivers of steel demand. These industries require highly specialized steel grades, known as tubular products, for exploration, production, processing, and transportation infrastructure. Seamless and welded pipes are essential components for high-pressure applications, pipelines, and downstream processing facilities.

The expansion of domestic refining and petrochemical capacities, driven by the desire to capture more value from extracted hydrocarbons, necessitates substantial investment in new plants and upgrades to existing infrastructure. This requires corrosion-resistant, high-strength alloy steel, often sourced from specialized global suppliers but increasingly a target for domestic production under the localization initiatives. Furthermore, the expansion of supporting infrastructure, such as ports, logistics hubs, and storage tanks, which are integral to the hydrocarbon supply chain, also relies heavily on steel. This industrial segment provides a stable base of demand for the steel industry in Saudi Arabia, complementing the more cyclical needs of the construction sector. The intersection of traditional energy prowess with modern industrial expansion ensures a dynamic and resilient market.

Growing Demand for Sustainable and Recycled Steel:

A key factor distinguishing the current phase of growth is the emphasis on sustainability, aligning the Saudi Arabia steel market trends with global environmental standards. The Kingdom’s commitment to achieving net-zero emissions has translated into a growing demand for green steel and steel produced using more circular economy principles. This shift is particularly evident in the construction sector, where developers of giga-projects are increasingly prioritizing materials with lower embodied carbon footprints.

Manufacturers in Saudi Arabia are responding by investing in advanced technologies, such as Electric Arc Furnaces (EAFs), which primarily utilize scrap metal as feedstock. This process is significantly less carbon-intensive than traditional methods. Furthermore, the nation is strategically positioned to transition towards next-generation production methods, including hydrogen-based direct reduction (H2-DRI), leveraging its massive, planned investments in green hydrogen production. This proactive adoption of cleaner production methods creates a distinct market segment for high-quality, recycled, and low-carbon steel. As green building certifications and sustainability mandates become standard, the demand for sustainably produced steel will continue to grow, positively influencing the entire Saudi Arabia steel market. This evolution toward environmentally conscious practices is reshaping the competitive landscape and technological priorities within the industry.

Increasing Investments in Industrial and Manufacturing Facilities:

The national strategy for economic diversification includes a strong focus on enhancing the domestic manufacturing base, moving beyond commodity production to higher-value goods. This drive involves establishing new industrial cities, specialized manufacturing zones, and large-scale industrial complexes. The construction of these facilities—from automotive manufacturing plants and machinery production hubs to specialized material processing centers—requires significant volumes of steel.

This growth segment is crucial because it generates long-term, recurrent demand for steel products that goes beyond the initial construction phase. Once operational, these manufacturing facilities become steady consumers of flat steel products, sheets, coils, and specialized components for their ongoing operations and production needs. The government’s National Industrial Development and Logistics Program (NIDLP) is specifically designed to foster these industries, thereby guaranteeing a consistent demand source that reinforces the overall market growth. These investments are aimed at creating an intricate industrial ecosystem, where local steel producers are strategically integrated into the domestic supply chains of various manufacturing sectors. This planned horizontal integration provides greater stability and resilience to the Saudi Arabia steel market.

Government Initiatives under Vision 2030 to Boost Domestic Steel Production:

The strategic blueprint provided by Saudi Vision 2030 is arguably the master plan governing the acceleration of the Saudi Arabia steel market. The government has explicitly targeted the steel sector for massive capacity expansion and technological modernization. The core aim is to achieve near self-sufficiency in steel production, thereby securing critical material supply for national projects and reducing import dependency. This comprehensive plan is designed to restructure the industry, addressing historical weaknesses and focusing on producing specialized flat products where the Kingdom was previously reliant on foreign sources.

Initiatives include substantial financial incentives, policy support for local content (often through mandated local procurement), and the facilitation of large-scale industrial partnerships with global steel majors. These alliances are crucial for technology transfer and access to high-grade production expertise. The policy framework includes measures to ensure fair trade and support environmental, social, and governance (ESG) standards, promoting the growth of a high-quality, competitive steel industry in Saudi Arabia. These top-down government interventions create a highly favorable investment climate, ensuring that strategic projects necessary for national goals receive priority access to domestic steel capacity. The strategic alignment between government vision and industrial execution is a primary guarantor of the positive Saudi Arabia steel market outlook.

Opportunities and Challenges in the Saudi Arabia Steel Industry:

The robust Saudi Arabia Steel Market presents compelling opportunities alongside notable challenges. The primary opportunity lies in the sustained and predictable long-term demand generated by giga-projects, which offers a reliable pipeline for domestic producers. Furthermore, the focus on diversification creates a strong opening for manufacturers to move into high-margin products like automotive-grade steel, specialty alloys for the energy sector, and advanced construction materials. The pivot towards green production also positions the Kingdom as a potential leader in the future low-carbon steel market.

However, several critical challenges must be navigated. One major concern is the reliance on imported raw materials, particularly iron ore, which exposes the industry to volatility in global commodity prices and international shipping dynamics. Successfully meeting the massive projected Saudi Arabia steel market size requires overcoming logistical and supply chain hurdles. Another significant challenge is the need for a highly skilled workforce, particularly in advanced manufacturing and digitalized operations, a gap that requires substantial investment in human capital development and training. Furthermore, maintaining profitability amidst global capacity fluctuations and trade policy changes remains a constant balancing act for the steel industry in Saudi Arabia.

Future Outlook for the Saudi Arabia Steel Industry:

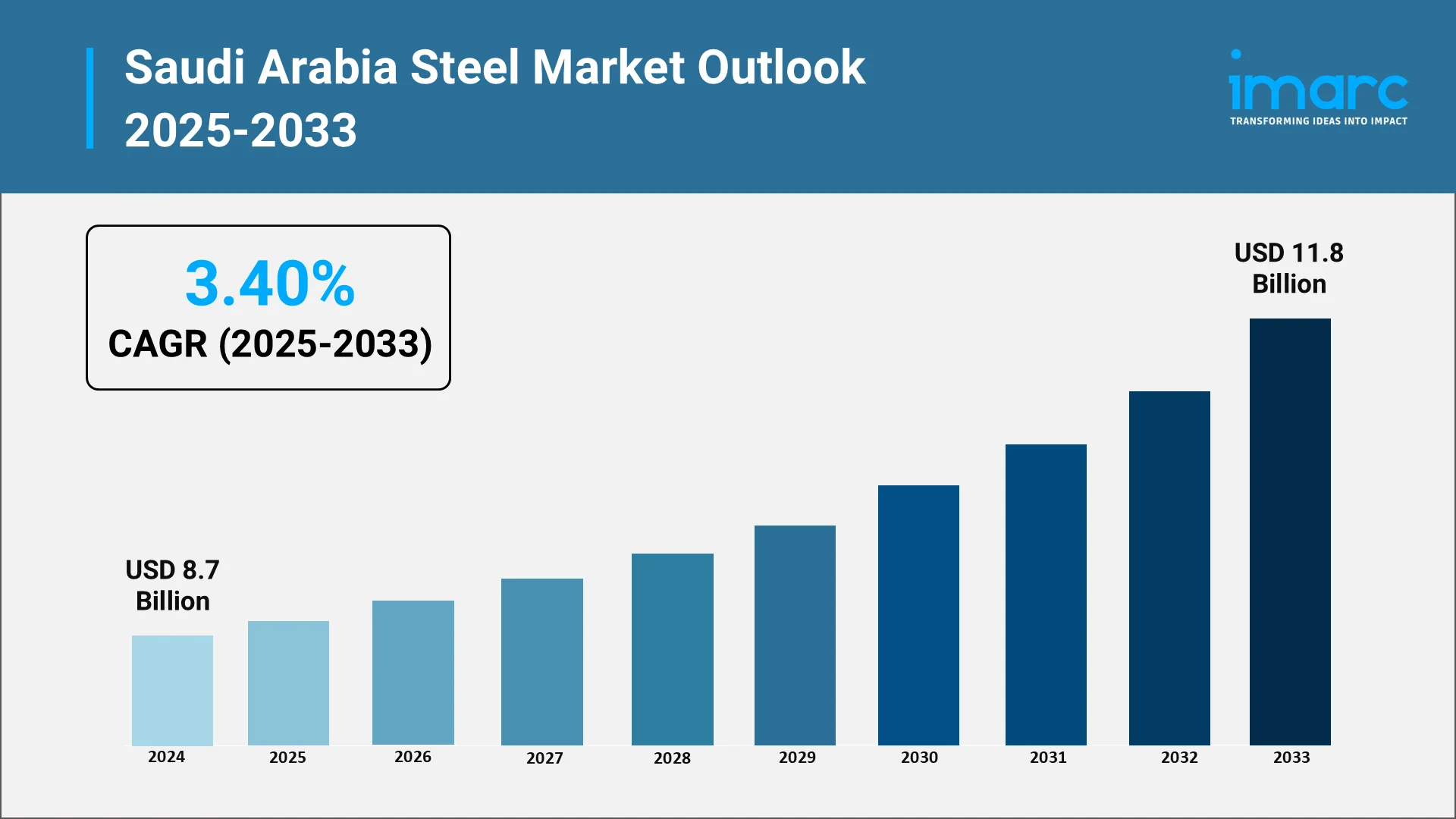

The Saudi Arabia steel market outlook is overwhelmingly positive, driven by the sustained momentum of the Vision 2030 agenda. The industry is transitioning from being primarily a supplier of commodity construction steel to becoming a strategic, technologically advanced sector capable of providing specialized materials for a diversified economy. This future growth is underpinned by key saudi arabia steel market trends, including the increasing adoption of Industry 4.0 technologies—automation, digitalization, and Artificial Intelligence—to optimize production efficiency and product quality. The Saudi Arabia steel market size was valued at USD 8.7 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 11.8 Billion by 2033, exhibiting a CAGR of 3.40% from 2025-2033.

The long-term expansion of the Saudi Arabia steel market size will be intrinsically linked to the successful completion of the giga-projects and the establishment of a vibrant local manufacturing ecosystem. The focus on sustainability, particularly the shift to hydrogen-based production and enhanced recycling efforts, will not only ensure compliance with global environmental standards but will also confer a competitive edge in international markets. As the Kingdom continues its trajectory of economic transformation, the steel sector is set to remain a powerful engine of industrial growth, reinforcing the nation's position as a regional economic powerhouse and solidifying its Saudi Arabia steel market share on a global scale. The long-term forecast suggests an era of profound expansion, modernization, and strategic importance for the nation’s steel producers and related industries.

Choose IMARC Group for Unmatched Market Intelligence and Strategic Advisory:

- Comprehensive Data-Driven Analysis: Access detailed insights into the Saudi Arabia steel market through extensive research covering production capacity, consumption patterns, trade flows, and competitive dynamics across all major steel product categories and end-use segments.

- Strategic Growth Forecasting: Leverage sophisticated modeling techniques to anticipate emerging trends in steel demand driven by infrastructure development, industrial expansion, sustainability initiatives, and technological innovation throughout the Kingdom and broader region.

- Competitive Intelligence Services: Gain actionable understanding of competitive forces shaping the Saudi steel industry through detailed benchmarking of major producers, analysis of capacity expansion plans, and tracking of technology adoption patterns and strategic partnerships.

- Policy and Regulatory Guidance: Stay ahead of evolving government policies affecting steel production and consumption, including local content requirements, trade measures, environmental regulations, and Vision 2030 implementation priorities that shape market conditions.

- Customized Consulting Solutions: Receive tailored intelligence aligned to your specific organizational objectives—whether entering the Saudi steel market, evaluating acquisition opportunities, optimizing product portfolios, or developing long-term strategic plans for regional expansion.

At IMARC Group, we empower steel industry stakeholders with the clarity and intelligence required to navigate complex market dynamics and capitalize on growth opportunities. Partner with us to make informed decisions that drive competitive advantage—because strategic insight makes the difference between opportunity and achievement. Click here for more details: https://www.imarcgroup.com/saudi-arabia-steel-market

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

A silk reeling unit is a type of manufacturing plant where raw silk threads are obtained from the cocoons of silkworm moths and processed into raw silk yarn by weaving them into a continuous strand of raw silk.

PVC solvent cement is a specialized adhesive formulation used to create permanent joints between polyvinyl chloride (PVC) pipes, fittings, and components. Unlike standard adhesives that rely on surface bonding, solvent cement chemically fuses PVC materials together. It works by using a blend of solvents and resins that temporarily soften and dissolve the surfaces of the PVC components.

PVC (Polyvinyl Chloride) pipes are durable and versatile piping products made from a synthetic thermoplastic polymer known for its strength, chemical resistance, and longevity. These pipes are produced primarily through the extrusion process, which ensures consistent wall thickness and uniform mechanical properties. Available in both rigid and flexible forms, PVC pipes are designed to transport fluids, gases, or solids safely under controlled pressure and temperature conditions.

Plastic pyrolysis is a form of recycling plastic waste via a process referred to as thermochemical recycling. This process produces liquid fuels, gases, and solid wastes through thermal degradation under low or no oxygen. Unlike traditional recycling, plastic pyrolysis involves the breakdown of long polymer chains into smaller hydrocarbon molecules using heat, in most cases in the presence of catalysts.

Insulation tapes made of PVC are adhesive tapes produced through a process involving a polyvinyl chloride (PVC) carrier coated with an adhesive made of rubber or acrylic materials. These insulation tapes have applications in electrical installations to serve their intended purpose of insulation and protection against environmental damage for electrical components and cables.

Precipitated silica is a synthetic and amorphous silicon dioxide, which is prepared through a process of controlled chemical reaction between soluble silicates and mineral acids. Unlike regular silica, precipitated silica is manufactured to have desired particle sizes, surface area, and porosity in terms of its structure, determining its final end-use performance. Precipitated silica is a fine, white, and free-flowing powdered substance.

Plywood is an engineered wood product made by bonding multiple thin layers of wood veneer together with strong adhesives under heat and pressure. The veneers are oriented so that their grain directions are at right angles to each other in successive layers, a manufacturing technique that improves strength, stability in dimensions, and resistance to cracking or warping.

Plastic crates are a rigid and reusable construction with a production material that includes a thermoplastic such as high-density polyethylene (HDPE) and Polypropylene (PP). These crates have design features that ensure the efficient storage, transport, and handling of goods while having a strong load-bearing capacity and a longer life span.

The cement industry remains one of the most critical foundations of global development, shaping the built environment and enabling progress across residential, commercial, and industrial landscapes. As construction activity expands and infrastructure investment intensifies, the cement market size continues to evolve, supported by new material innovations, sustainability priorities, and smart manufacturing technologies.

The GCC ceramic tiles market has emerged as one of the most dynamic segments in the region's construction and building materials sector. Spanning countries including United Arab Emirates, Saudi Arabia, Kuwait, Oman, Qatar, and Bahrain, the market reflects the Gulf region's ambitious transformation from oil-dependent economies to diversified, modern nations.

Paints are liquids, semi-liquids, or powdered materials, usually having a high content of pigments, binders or resins, solvents or vehicles, or additives, intended for application onto substrates to create a continuous film after drying or curing. Paints work as materials after their application, possessing several functionalities, such as protecting the surface, adding color, or modifying functionalities. Paints contain several components, such as binders or resins, pigments, solvents or vehicles, or additives, each differing based on their functionalities. The binder or resin is mainly involved in providing strength or adhesive characteristics, while pigments are used to create colors or opaqueness.

Organic fertilizers refer to nutrient-value-adding materials that come from ecologically degradable sources like plant debris, animal manure, composted materials, bio-wastes, bone meal, and microbe organisms. Another key point of distinction between organic and synthetic fertilizers is that whereas synthetic fertilizers give quicker nutrient release through chemical reactions, nutrient release occurs via bacterial decomposition in the case of organic fertilizers.

Oleochemicals are chemicals obtained from natural fats and oils derived mainly from renewable plant-based feedstocks like palm oil, palm kernel oil, coconut oil, soybean oil, and other materials high in triglyceride content. These raw materials are transformed into fatty acids, fatty alcohols, glycerin, methyl esters, and other derivatives by means of hydrolysis, transesterification, hydrogenation, fractionation, and other techniques. They represent renewable, biodegradable, and environmentally friendly alternatives to chemicals made from petrochemical raw materials.

NdFeB magnets are a family of high-performance permanent magnets primarily made of an alloy of neodymium, iron, and boron. They are fabricated by the sintering or bonding processes, which create extremely high magnetic energy density and make them the most powerful commercial magnets. NdFeB magnets have the best coercivity, remanence, and effectiveness in compact forms that can generate strong magnetic fields in the smallest volume.

Mineral wool ceiling tiles consist of acoustic and thermal insulation panels fabricated from inorganic fibers, which originate mainly from molten basalt, slag, or other mineral-based raw materials. The fibers are spun and bonded together with resins, then compressed into rigid tiles that perform well in terms of sound absorption, fire resistance, and moisture tolerance. They are usually available in standard sizes for application in suspended ceiling systems in commercial, industrial, and institutional buildings.

Methanol, also known as methyl alcohol or wood alcohol, is a colorless liquid that is volatile and flammable with the chemical formula CH3OH. The simplest of the alcohols, it is produced mainly by the catalytic conversion process of natural gas, coal, or biomass into synthesis gas-a mixture of carbon monoxide and hydrogen-further followed by methanol synthesis under high pressure.

Lubricating oil is a specially formulated liquid substance that reduces friction, wear, and generation of heat between moving mechanical surfaces. It is usually made from refined mineral base oils, synthetic oils, or a mixture of both, supplemented with performance-improving additives such as anti-wear agents, detergents, dispersants, antioxidants, corrosion inhibitors, and viscosity improvers.

The Philippines passenger vehicles lubricants industry stands at a transformative juncture, driven by robust automotive sector expansion, technological innovation, and evolving consumer preferences toward high-performance products. As the Philippine economy demonstrates resilient growth and vehicle ownership continues to rise, the demand for premium automotive lubricants has accelerated significantly across the archipelago.

Hydrogen is the lightest and most abundant element in the universe, being a colorless, odorless, highly combustible gas. It does not usually occur free in nature but is produced from hydrogen-rich compounds like water, natural gas, biomass, or other hydrocarbons. Owing to its high energy content per unit mass and clean combustion (with the production of water vapor only), hydrogen is widely recognized as a versatile energy carrier. Depending on how hydrogen is produced, it is classified as grey, blue, or green and increasingly plays a significant role in clean energy systems, industrial processing, and developing low-carbon technologies.

HDPE pipes are thermoplastic piping systems made from high-strength polyethylene resin, which features excellent flexibility, high impact resistance, and strong chemical and corrosion resistance. HDPE pipes are produced by extruding molten polyethylene into a variety of diameters and pressure ratings. Their seamless structure, along with their low friction and resistance to internal pressure and external load, makes them ideal for the transport of fluids. HDPE pipes boast superior endurance, long service life, and leak-free performance, since it is possible to join them through heat fusion, thus creating monolithic, continuous pipelines that are suitable for buried, aboveground, or underwater installations.

Graphite is a crystalline form of pure carbon, where atoms are organized in layered hexagonal structures, reflecting exceptional lubricity, electrical conductivity, heat resistance, and a high degree of chemical stability. It comes in many forms: flake, amorphous, vein, and synthetic graphite-derived from petroleum coke or coal tar pitch. Because of this layered structure, the sheets slip easily, which gives graphite its characteristic softness and lubricity, while strong covalent bonding within the layers makes it thermally stable and conductive. The unique characteristics make graphite indispensable in uses such as steelmaking, refractories, batteries, electronics, and in high-performance industrial components.

The Japan urea industry stands as a critical pillar supporting multiple sectors of the nation's economy, from agricultural productivity to automotive emissions control. As a nitrogen-rich compound essential for modern farming practices, urea plays an indispensable role in ensuring food security for Japan's population while simultaneously addressing stringent environmental standards through its industrial applications.

The Japan industrial gases industry stands as a critical enabler of the nation's economic infrastructure, supporting diverse sectors including manufacturing, healthcare, electronics, semiconductors, steel production, and energy generation. Industrial gases such as oxygen, hydrogen, nitrogen, carbon dioxide, argon, and specialty gases serve as essential inputs across these industries, facilitating everything from metal fabrication and medical treatments to advanced semiconductor manufacturing.

A fire extinguisher is either a portable or fixed device that is designed to combat and suppress small fires by discharging a controlled substance, which cools the burning material, cuts off oxygen supply, or interrupts the chemical chain reaction sustaining combustion. It is among the most important items that comprise fire protection systems, finding wide applications in residential, commercial, industrial, and transport environments.

Fiberglass, also known as glass fiber, is a composite material manufactured by weaving, chopping, or layering minute strands of glass into strong yet lightweight and durable products. It is made by melting silica sand, limestone, soda ash, and other raw materials together at very high temperatures-around 1,700°C-through which molten glass is obtained. It is extruded through fine nozzles to create continuous filaments, then combined into mats, fabrics, or roving later on, according to use.

Engine oil is a specific lubricant that serves to reduce friction, wear, and heat in an internal combustion engine's moving parts, allowing the smooth operation of such engines. Besides lubrication, it accomplishes other very important tasks: cooling, cleaning, sealing, and protection against corrosion. The two major components of engine oil formulation are the base oil and additives. The base oils, mineral or petroleum-based, synthetic, and semi-synthetic, constitute approximately 70-90% of the formulation and provide the fluidity and viscosity for the best performance.

The Australia bioplastics industry is experiencing unprecedented growth, driven by intensifying consumer demand for sustainable alternatives and robust government sustainability initiatives.

Ferrous sulphate is an inorganic salt, composed of iron, sulfur, and oxygen, and is mainly known for its pale green or blue-green crystalline appearance. It exists in various hydrated forms, the most common being ferrous sulphate heptahydrate (FeSO4·7H2O), although it is also produced largely as a monohydrate and anhydrous variant, depending on the industrial needs. It is usually manufactured as a by-product of the pickling of steel using sulfuric acid, or it could be produced as a co-product from titanium dioxide pigment manufacture.

Bamboo plywood is an engineered wood product that is made by laminating thin strips or veneers of bamboo into multi-layered panels to create a stable, uniform sheet material combining the natural aesthetics of bamboo with the structural versatility of plywood. Unlike conventional plywood made from hardwood or softwood veneers, bamboo plywood most often uses strand-woven, horizontal, or vertical lamination patterns of bamboo culm that are bonded under heat and pressure with formaldehyde-free or low-emission adhesives.

Biomass pellets are a sustainable, carbon-neutral, and renewable source of energy made from organic materials such as forestry waste, agricultural residues, sawdust, wood chips, and other biomass feedstocks. Biomass pellets are small, cylindrical in shape, and usually between 6 and 12 millimeters in diameter and are utilized as a clean energy alternative to fossil fuels in power production, heating, and for industrial purposes.

Bioethanol is a biodegradable, renewable alcohol that is made by fermenting sugars from biomass resources like corn, sugarcane, wheat, cassava, and cellulosic materials like agricultural waste and forest residues. It is cleaner than gasoline from fossil fuels and provides valuable decreases in greenhouse gases and helps to move us toward sustainable energy systems. The process of production of bioethanol is mainly about the conversion of biomass carbohydrate to simple sugars by hydrolysis and subsequent fermentation by yeast or bacteria into ethanol.

Blue ammonia is one type of ammonia production that is meant to reduce carbon dioxide emissions. Traditional methods of ammonia production include sourcing hydrogen from natural gas, usually through steam methane reforming (SMR) or auto-thermal reforming (ATR) and then reacting this hydrogen with nitrogen (from air) through the Haber-Bosch process. The "blue" suffix indicates that the carbon dioxide waste product produced in the course of hydrogen synthesis is captured (through Carbon Capture, Utilization, and Storage / CCUS) and not released into the environment.

Biodiesel is a renewable and biodegradable fuel source mainly from vegetable oils, animal fats, or waste cooking oils, and can serve as a direct replacement or blend with traditional petroleum diesel. It is chemically constituted by fatty acid methyl esters (FAMEs), which are formed when triglycerides react with methanol or ethanol in the presence of a catalyst under transesterification.

Anhydrous Ferric Chloride, FeCl3, is a corrosive dark brown crystalline chemical that finds extensive application as a major industrial chemical in water treatment, metallurgy, electronic manufacturing, and chemical synthesis industries. It is produced by reacting chlorine gas with iron or ferrous chloride at elevated temperatures to form a high-purity, moisture-free product. In contrast to its hydrate, anhydrous ferric chloride is not aqueous and is mostly used in processes involving controlled levels of moisture, for example, etching circuits in electronics and as a catalyst in the synthesis of organics.

Ammonium Bicarbonate (NH4HCO3) is a white crystalline inorganic chemical used extensively in the fertilizer, food processing, pharmaceutical, and chemical industries. It is a salt that is produced by the combination of ammonia, carbon dioxide, and water and is renowned for decomposing at relatively low temperatures into ammonia, carbon dioxide, and water vapor. This characteristic makes it useful as a leavening agent for the food industry, especially in baked foods, cookies, and crackers, which produce a light and porous texture due to its presence.

Biodegradable plastic granules are eco-friendly polymer materials designed to decompose naturally through the action of microorganisms such as bacteria, fungi, and algae, reducing the environmental burden associated with conventional plastics. These granules are the fundamental raw materials used in the production of biodegradable products such as packaging films, agricultural mulch, carry bags, cutlery, and medical components.

Bioplastics are a category of materials that come entirely or partly from renewable biological resources like corn starch, sugarcane, vegetable oils, or cellulose, to be used as sustainable substitutes for traditional petroleum-based plastics. Bioplastics may be biodegradable, non-biodegradable, or compostable, depending on their chemical composition and manufacturing process.

Battery recycling is the collection, dismantling, and processing of used or end-of-life batteries to recover valuable materials and limit environmental threats. With the burgeoning exponential increase in electric vehicles (EV), renewable energy storage, and consumer electronics, the number of spent batteries has skyrocketed, necessitating recycling as a key component of the energy transition worldwide.

Binding wire is a low-cost, flexible steel wire, mainly utilized for tying, fastening, and bundling in applications of construction, industry, agriculture, and packaging. Usually produced from mild steel wire rod by successive cold-drawing, annealing and surface-finishing processes, binding wire comes in an assortment of gauges (typically 18–24 AWG / 1.0–1.6 mm) and in a few forms: soft/annealed plain wire, galvanized (zinc-coated) wire for corrosion-proofing, and polymer/PVC-coated wire for better handling and durability.

Aluminum anodizing is an electrochemical process that improves the surface characteristics of aluminum by creating a long-lasting, corrosion-resistant oxide coating on its surface. In contrast to coatings or paint applied to the outside surface, anodizing makes the outer surface of aluminum into a protective aluminum oxide coating that is bonded integrally to the metal and will last long and stay adherent.

Aluminum powder is a finely divided metallic aluminum with a wide range of applications in various industries because of its specific physical and chemical properties. It is manufactured by atomization, mechanical grinding, or flake milling of pure aluminium. The powder has high reactivity, low density, high thermal conductivity, and high reflectivity. Depending on the manufacturing technique, it can exhibit spherical, irregular, or flake-like morphologies, making it suitable for diverse applications.

Aluminum bottles are lightweight, strong, and recyclable packages manufactured mostly from high-purity aluminum that provides a sustainable and premium alternative to conventional plastic and glass packaging. Aluminum bottles integrate functionality with style and, therefore, are gaining popularity in industries like beverages, cosmetics, personal care, pharmaceuticals, and household products.

Aluminum ingots are standardized raw forms of aluminum that are produced by smelting and refining processes, which act as a basic raw material for downstream industries. The ingots are commonly prepared by refining bauxite ore to alumina through the Bayer process, followed by electrolytic reduction in smelters through the Hall-Héroult process. The molten aluminum thus produced is cast into ingot shape for transportation convenience, handling, and further processing.

Aluminum extrusion is a versatile metal forming process whereby aluminum billets are pushed through a shaped die to create long profiles with the same cross-section. Through this process, manufacturers can create intricate shapes that balance strength, lightweight characteristics, and beauty, making it a cornerstone of several industries.

Activated alumina balls are porous, granular, and spherical materials consisting of aluminum oxide (Al2O3). They possess a large surface area, high adsorbing capacity, and excellent resistance to thermal shock and abrasion. Manufactured by the controlled dehydroxylation of aluminum hydroxide, activated alumina balls are chemically inert, non-toxic, and possess excellent water and polar molecule affinity. Due to such features, they find extensive applications as desiccants, adsorbents, and catalysts. In industrial operations, they are useful for drying gases and liquids in processes, eliminating fluoride, arsenic, and selenium ions from water, and as a catalyst carrier in petrochemical refining applications.

Activated carbon or activated charcoal is a very porous form of carbon with an incredibly large surface area, usually anywhere from 500 to 1,500 m²/g. Manufactured by activating carbon-rich materials such as coconut shells, wood, coal, or peat, it is subjected to physical or chemical treatment to create its distinctive pore structure. The microporous structure enables activated carbon to efficiently absorb gases, vapors, and dissolved materials, which makes it a vital adsorbent in all industries.

Glass Fiber Reinforced Polymer (GFRP) rebar and mesh are composite materials developed to be used in place of the conventional steel reinforcement in concrete structures. They consist of continuous glass fibers dispersed within a polymeric resin matrix, most commonly epoxy, vinyl ester, or polyester. The synergy between the tensile strength of glass fiber and the corrosion inhibition properties of polymers produces reinforcement products that are light weight, corrosion-free, and extremely durable.

Phosphorus Pentasulfide (P2S5) is a yellow-green crystalline compound primarily produced through the controlled reaction of elemental phosphorus and sulfur. As a key phosphorus-based intermediate, it plays a critical role in the chemical industry, particularly in the manufacture of lubricant additives such as zinc dialkyldithiophosphate (ZDDP), agrochemicals, and battery electrolytes. Structurally, P2S5 consists of phosphorus and sulfur atoms bonded in a cage-like configuration, imparting high reactivity and compatibility with organic synthesis pathways. It is valued for its sulfur-donating properties, thermal stability, and role as a bridging compound in synthesizing more complex phosphorus-sulfur compounds.

Steel bolts and fasteners are integral mechanical components that provide secure connections across industrial, commercial, and household applications. Comprising primarily of carbon steel, alloy steel, or stainless steel, these fasteners are engineered to withstand significant mechanical loads, torque, and environmental exposure. Their key properties include high tensile strength, corrosion resistance, dimensional precision, and durability under cyclic stress. Manufacturing typically involves processes such as forging, machining, threading, and surface finishing to meet exacting industry standards.

Copper sulphate is an inorganic chemical made up of copper, sulfur, and oxygen that is best known for its crystalline blue color and varied uses. Most often found as copper sulphate pentahydrate (CuSO4·5H2O), it is prized for its water solubility, stability, and fungicidal activity. Primary characteristics are that it is a fungicide, herbicide, algicide, and electrolyte used in industrial applications. It also serves as a precursor for the manufacture of other compounds of copper and as a laboratory reagent.

Sebacic acid is a naturally occurring dicarboxylic acid, a long-chain organic compound with two carboxyl functional groups. It is mainly produced from castor oil through cracking and purification in a significant industrial process, as it is a valuable bio-based chemical with major industrial relevance. The white flaky or crystalline powder is cherished for its superior properties, such as high thermal stability, corrosion resistance, and the ability to form long-lasting polymers.

Aluminium conductors are electrical wires or cables whose current-carrying core is primarily made of aluminium (or its alloys), used for overhead transmission lines, distribution, AAC (All Aluminium Conductor), AAAC (All Aluminium Alloy Conductor), ACSR (Aluminium Conductor Steel Reinforced), etc. The material is lightweight, has relatively good electrical conductivity (lower than copper but acceptable for many applications), and is cost-effective per unit weight.

Steel rolling products, encompassing hot-rolled, cold-rolled, and coated steel sheets and coils, form the backbone of numerous industrial applications, from automotive manufacturing to construction and infrastructure. The cost of these products is influenced by a complex interplay of raw material prices, energy costs, labor, technological advancements, and logistical considerations.

Treatment of sewage is the procedure of eliminating contaminants from domestic or industrial wastewater to yield treated effluent that can be safely released into the environment or recycled for different purposes. Sewage contains organic matter, nutrients, suspended solids, microorganisms, and chemical pollutants and hence physical, chemical, and biological processes must be utilized for purification.

Green methanol is a renewable and sustainable form of methanol produced from non-fossil-based feedstocks such as biomass, municipal solid waste, biogas, or captured carbon dioxide combined with green hydrogen generated via electrolysis powered by renewable energy. Chemically, it is identical to conventional methanol (CH3OH), a simple alcohol with high energy density and versatile chemical properties.

Sodium hydrosulfide (NaHS) is an inorganic chemical mainly known for its good reducing nature and adaptability in uses in industry. It exists as pale yellow solid or liquid in aqueous solution with the smell of sulfur. It is chemically obtained by the partial neutralization of hydrogen sulfide (H2S) by sodium hydroxide (NaOH) to form a stable and water-soluble salt.

Recycled Polyethylene Terephthalate (rPET) is a thermoplastic polymer obtained from post-consumer and post-industrial PET waste, mainly plastic bottles and packaging materials. It is chemically the same as virgin PET, composed of polymerized units of terephthalic acid and ethylene glycol, but is made from a recycling process that minimizes dependence on fossil-based feedstocks. Major characteristics of rPET are high strength-to-weight ratio, chemical resistance, dimensional stability, and high recyclability.

Animal feed grade Di-calcium Phosphate (DCP) is a mineral feed supplement commonly applied in animal and poultry nutrition to fortify dietary calcium and phosphorus—two of the most important nutrients in maintaining animal health and production levels. Manufactured predominantly through the reaction of phosphate rock-based phosphoric acid with calcium carbonate or lime, feed-grade DCP is generally found as a white or off-white granular or powdered material.

Copper tubes are cylindrical hollow goods consisting mainly of purified copper, which are highly prized for their high thermal conductivity, corrosion resistance, ductility, and antimicrobial qualities. They are produced by processes like casting, extrusion, and drawing, which provide accurate dimensions and clean internal surfaces.

Automotive fabrics are specialized textile materials engineered for use in vehicle interiors, combining aesthetics, functionality, and durability. Unlike ordinary textiles, automotive fabrics must withstand prolonged wear, UV exposure, temperature variations, and continuous contact, while also contributing to passenger comfort and vehicle safety.

Aluminum sheets, cans, and foils are among the most common types of processed aluminum, serving industries from packaging and construction to transport and consumer products. Aluminum sheets are flat-rolled material manufactured in a range of thicknesses and grades, prized for light weight, corrosion resistance, and ability to be recycled, ideal for use in car body panels, building cladding, roofs, and kitchen appliances.

Synthetic graphite is a state-of-the-art carbon material developed through petroleum coke and coal tar pitch treatment at high temperatures, providing highly crystalline carbon materials of higher purity and uniformity than natural graphite. Synthetic graphite is produced in controlled industrial conditions unlike natural graphite, which is excavated.

Diammonium Phosphate (DAP) is among the most popular phosphorus fertilizers in the world due to its high concentration of nutrients and multiple uses in agriculture. It is manufactured by reacting ammonia with phosphoric acid, forming a compound that has about 18% nitrogen and 46% phosphorus pentoxide (P2O5). Such levels of nutrients make DAP an effective supply of critical macronutrients for plants, especially for root development, seed germination, and plant growth early on.

Australia's battery recycling market is charging ahead, with a value of USD 336 Million in 2024 and no signs of slowing down. Driven by the booming demand for cleaner, greener solutions—especially in the Australia battery energy market and electric vehicle (EV) sectors—the industry is expected to reach USD 612.55 Million by 2033. That’s a steady growth rate of 6.90% annually from 2025-2033.

Green ammonia is used to describe ammonia made from renewable energy systems like wind, solar, or hydropower through water electrolysis to obtain green hydrogen, then blended with nitrogen in the air through the Haber-Bosch process. Unlike traditional ammonia, which is derived from natural gas and produces enormous amounts of CO2, green ammonia is a carbon-free and sustainable alternative.

Hydrogen Peroxide (H2O2) is an all-purpose, eco-friendly chemical used extensively as an oxidizing, bleaching, and disinfectant agent in various industries. Hydrogen Peroxide is a clear, colorless liquid with high oxidizing power, breaking down into oxygen and water, and thus a clean alternative to several hazardous chemicals.

Biofertilizers are microbial products that contain living microbes, and they enhance plant growth through the improvement of nutrient availability in the soil microcosm. They may consist of useful microorganisms like Rhizobium, Azotobacter, Azospirillum, phosphate-solubilizing bacteria (PSB), and mycorrhizal fungi. These microorganisms form symbiotic or associative relations with plants and enhance nitrogen fixation, phosphorus solubilization, and the uptake of required nutrients.

Steel stands as one of the world’s most essential industrial materials, forming the backbone of modern infrastructure, manufacturing, and economic progress. As a critical material, its production and consumption directly influence global economic dynamics. The steel market has seen significant evolution, driven by innovations, demand from diverse sectors, and increasingly sustainable practices.

The global petrochemicals market is witnessing steady growth, supported by rising end-user consumption, industrial diversification, and infrastructure development across both developed and emerging economies.

Ethyl acetate is a volatile, colorless, flammable liquid having a characteristic sweet smell. It is primarily used as a solvent in various industrial and commercial applications. It finds primary production through esterification from ethanol and acetic acid.

Ammonium nitrate (NH4NO3) is a white solid that is widely used as a high-nitrogen fertilizer and as a component of industrial explosives. It is made by neutralization of ammonia with nitric acid and is very soluble in water, making it useful for its efficiency in providing nitrogen to plants.

Ceramic tiles are durable, versatile, and cost-effective building materials made from natural clay, sand, and water, which are shaped, glazed, and kiln-fired at high temperatures. Known for their aesthetic appeal, resistance to moisture, and ease of maintenance, ceramic tiles are widely used in flooring, walls, kitchen backsplashes, and bathrooms across residential, commercial, and industrial spaces.

Diethylenetriamine (DETA) is a colorless, hygroscopic organic chemical compound of the ethyleneamine group having the chemical formula HN(CH2CH2NH2)2. It is a triamine that contains two primary amine groups and one secondary amine group, thus imparting to it a highly reactive molecular structure to be used in a number of industrial processes.

Calcium Chloride Anhydrous (CaCl2) is an off-white, hygroscopic inorganic substance commonly utilized due to its high desiccating and exothermic properties. The anhydrous form, as opposed to its hydrated counterparts, has no water molecules within it, thus making it very effective to use in moisture control processes.

Explore a step-by-step guide to setting up a unsaturated polyester resin production plant including planning, machinery, raw materials, costs & demand drivers.

Explore the growth, trends, and innovations driving the global bio-lubricant market toward a sustainable future.

Medium Density Fibreboard (MDF) is an engineered wood product created by dissolving hardwood or softwood residues into wood fibers, blending them with wax and resin binders, and molding them into panels under the pressure of high temperature. MDF is renowned for its even density, smooth surface, and easy machinability and is used extensively in cabinetry, flooring, furniture, and interior decoration because of its relative cheapness and adaptability as compared to plywood and solid wood.

Lanthanum oxide (La2O3) is a white, odorless, and extremely stable rare earth compound obtained mainly from monazite and bastnäsite ores. It is essential for a vast array of industrial uses such as the manufacture of optical lenses, ceramics, phosphors, and battery electrodes. Lanthanum oxide is also used extensively as a catalyst in petroleum refining processes, particularly in fluid catalytic cracking (FCC) operations. Due to its exceptional electrical, optical, and catalytic properties, La2O3 is an important material for advanced technologies like electric vehicles (EVs), smart electronics, and renewable energy devices.

Silica sand is a pure quartz-based material used extensively by many industries. It is known for its durability, chemical inertness, and resistance to heat, and it is an important raw material in glass production, construction, foundries, electronics, and hydraulic fracturing (fracking). Increasing demand for high-purity silica in semiconductors, solar panels, and filters is fueling market growth. With more infrastructure development and development in silica processing, the applications keep expanding, and it is becoming an essential industrial commodity worldwide.

Stone paper is an innovative, eco-friendly material gaining traction across various industries due to its durability, sustainability, and water resistance. Made primarily from calcium carbonate and resin, it offers a tree-free alternative to traditional paper, reducing deforestation and water consumption. Its tear-resistant and smooth texture makes it ideal for printing, packaging, and stationery applications. Additionally, stone paper is recyclable, photodegradable, and highly resistant to moisture, making it suitable for outdoor and high-humidity environments. With growing environmental concerns and demand for sustainable packaging and printing solutions, stone paper is emerging as a key player in the global paper industry, attracting interest from publishers, packaging manufacturers, and eco-conscious brands.

Nitrile gloves are synthetic rubber gloves that are extensively used in the medical, industrial, and food industries because of their strength, resistance to chemicals, and hypoallergenic nature. They are ideal for people with allergies since they are latex-free, as opposed to latex gloves. They are more flexible, puncture-resistant, and resistant to infection and chemicals. The demand for nitrile gloves in manufacturing, healthcare, and laboratory environments is increasing because of stringent safety regulations and increasing hygiene consciousness, which is driving the worldwide market growth.

Acetic acid (CH3COOH) is a clear, colorless liquid organic compound with a sour taste and a pungent odor. It is produced by the carbonylation of methanol and is also manufactured via bacterial fermentation. Acetic acid is extensively employed in the manufacturing of vinyl acetate monomer (VAM), purified terephthalic acid (PTA), acetic anhydride, and ester solvents, among others. It provides solvent effectiveness, chemically useful to use in syntheses, as well as utilization in the fabrication of polymers and resins.

Calcium bromide (CaBr2) is an inorganic compound commonly used in drilling fluids for oil and gas exploration, as well as in pharmaceutical and photographic applications. It is a white, crystalline solid or solution that dissolves very easily and is used as a clear, dense brine in well drilling operations. Calcium bromide is prized for its capacity to manage pressure and avoid well blowouts due to its exceptional thermal and chemical stability. The growing energy industry and improvements in drilling technology are the main drivers of its demand.

Laminated veneer lumber (LVL) is one of the most popular engineered wood products, which is manufactured from sliced and peeled thin wood veneers. LVL is a light material used for construction, which is utilized in public structures, industrial warehouses, product parts, large, prefabricated buildings, as well as designed wooden homes. This can be attributed to its strength, uniformity, high strength, and dimensional accuracy. Apart from this, it is utilized for structural framing in residential and commercial building work, including lintels, joists, beams, purlins, scaffold boards, concrete formwork, and truss chords.

Cross-laminated timber (CLT), an engineered wood product, is renowned for its durability, strength, and adaptability in contemporary building. CLT provides a lightweight yet strong substitute for steel and concrete in structures with sustainable engineering. Its layered structure adds to its integrity and makes it suitable for building anything from residential to commercial to high-rise buildings. Besides being aesthetically pleasing for eco-friendly building projects, CLT has very good fire resistance, thermal performance, and ease of installation. CLT changes the architectural sphere and instigates the development of new concepts for urban environments and shaping the future of sustainable construction.

Copper wire is a versatile, flexible, and highly conductive electrical wire used extensively in power transmission, telecommunications, and electronics. Fabricated from pure copper, copper wire has good thermal and electrical conductivity, resistance to corrosion, and ease of processing. Copper wire plays a critical role in construction, automotive, and consumer electronics industries. With the increased demand for effective power distribution and advancing technology, the copper wire market keeps growing because of urbanization, electrification, and growth in infrastructure development globally.

Aluminum wire rods are critical industrial products renowned for their high conductivity, strength, and versatility. They are cylindrical metal rods that are the backbone of electrical transmission and distribution systems and play a fundamental role in power infrastructure, building construction, and manufacturing. Due to their good conductivity and low weight, they are a top choice for cable production, overhead power lines, and electrical wires. Outside of electrical uses, aluminum wire rods find extensive application in the automotive, aerospace, and industrial industries, where their corrosion resistance and recyclability play important roles in sustainability initiatives.

N-Methyl Aniline (NMA) is an organic chemical compound widely used as an intermediate in various industrial applications. It plays a crucial role in the production of dyes, agrochemicals, pharmaceuticals and fuel additives. As a key component in high-octane fuel formulations NMA enhances combustion efficiency and reduces engine knocking making it valuable in the automotive and petroleum industries. Its use in the synthesis of specialty chemicals and pigments further expands its industrial significance.

Ammonium perchlorate is a crystalline, white inorganic substance that finds principal application as an energetic oxidizer in solid rocket propellants, explosives, and pyrotechnics. Its release of oxygen when subjected to heat gives it a fundamental role in different industrial and technological processes. Aside from its primary application in propulsion systems, it is also used in pyrotechnic devices to generate controlled, vibrant flames and brilliant effects, especially in aerospace displays and enormous entertainment productions.

Potassium sulfate (K2SO4) is an inorganic compound widely used as a specialty fertilizer, providing essential potassium and sulfur nutrients to crops. Its low salt index makes it the preferred crop for crops that are sensitive to chloride, like fruits, vegetables, and tobacco. Potassium sulphate is also used in pharmaceutical and glass manufacturing processes, among other industrial processes. It is the perfect choice for contemporary agricultural methods because of its high solubility and compatibility with irrigation systems, which promote plant development, yield enhancement, and soil health maintenance.

Battery electrolyte is a key element of energy storage, facilitating the flow of ions between electrodes to drive devices effectively. It is an important factor in lithium-ion, solid-state, and future batteries, influencing performance, safety, and durability. In electric vehicles, renewable energy storage systems, and consumer devices, development in electrolyte technology targets sustainability, improved conductivity, and heat resistance for unlocking the future of clean energy technologies.

Cobalt acetate is an inorganic substance that is frequently utilised in chemical synthesis as a precursor, dye mordant, and catalyst. This crystalline solid has a reddish-purple appearance and is very soluble in organic solvents and water. In addition to being widely used in the manufacture of paints, inks, and adhesives, it is also an essential component of polyester and a catalyst in oxidation processes. It is a crucial component in many industries, with industrial uses driving its demand, especially in petrochemicals, textiles, and battery technology.

Transformer oil, sometimes referred to as insulating oil, is essential to electrical transformer operation. Its main functions are to cool and insulate the internal parts. By acting as a dielectric medium, the oil prolongs the transformer's lifespan and improves overall performance by preventing electrical discharges between various components. It moves around inside the transformer, assisting in the dissipation of heat produced during the conversion of energy. Although there are synthetic and bio-based substitutes, refined mineral oil is usually the source of it. Moisture, impurities, or the disintegration of the oil's chemical structure can all cause its quality to decline over time. It must be tested and maintained on a regular basis to stay effective.

Silica gel is obtained from silica dioxide a naturally occurring compound in sand and comprises fine particles that can soak quantity of water. It is a drying agent that is frequently packaged in tiny paper or cloth packets as tiny, transparent beads or crystals of clear rock. These packets are frequently included with business goods to guard against moisture-related damage. Food, clothing, and electronics are just a few of the many things that include silica gel packets. Although silica gel is typically non-toxic, it poses a choking hazard, particularly to young children.

Amorphous silicon dioxide (silica) particles dispersed in water are known as colloidal silica. In order to produce these amorphous silica particles, silica nuclei from silicate solutions are polymerised in an alkaline environment to create silica sols with a high surface area and a nanometre size. The surface of the silica nanoparticles is then charged, which causes the particles to reject one another and create a stable colloid, or dispersion. Although colloidal silica comes in a variety of grades, all of them are made up of silica particles that range in size from roughly 2 nm to 150 nm. The particles might exist as discrete particles or as slightly organised aggregates, and they can have a spherical or slightly irregular shape.

In a time characterized by environmental awareness and limited resources, sustainable manufacturing has become an essential priority for companies all over the world. Sustainable manufacturing is a model beyond conventional manufacturing practices, focusing on the production of goods in a manner that reduces harm to the environment, uses less energy and natural resources, and prioritizes the health and safety of workers, communities, and consumers.

Intravenous (IV) solutions represent a critical and ubiquitous component of modern healthcare, playing a fundamental role in patient care and treatment. These sterile, liquid formulations consist of a carefully balanced blend of fluids and electrolytes, administered directly into a patient's bloodstream. They are tailored to address a wide range of medical needs, from rehydration and medication delivery to nutritional support and blood transfusions.

Titanium dioxide (TiO 2) is a white, naturally being mineral extensively used as a pigment, UV blocker, and opacifier. A vital element of paints, coatings, plastics, cosmetics, and sunscreens, it's well- known for its exceptional opacity, high illumination, and superior light- scattering capabilities. Also, TiO 2 is essential for advanced operations like photocatalysis, food, and pharmaceuticals. Because of its non-toxic and chemical- resistant rates, it's a necessary element of numerous different sectors, performing in steady demand worldwide.

Yellow phosphorus, a chemical element with the symbol P and atomic number 15, is a fascinating and essential element in the periodic table. This highly reactive nonmetal is widely known for its distinctive yellow appearance and its crucial role in various industrial applications. Found in nature primarily as phosphates, yellow phosphorus is isolated through a complex process to ensure its purity and effectiveness. Its versatility allows it to be employed in the production of fertilizers, detergents, and even in the synthesis of organophosphorus compounds used in medicine and pesticides.

Xanthan gum is a food additive that is produced by fermenting simple sugar using bacteria. It quickly disperses and creates a viscous and stable solution when added to a liquid for providing a thickness or stabilizing effect to a product. It assists in improving the texture, flavour, consistency, appearance, and shelf life of a product. It aids in preventing food products from separating and allowing them to flow smoothly and can lower blood sugar levels among individuals. It also reduces cholesterol levels, slows digestion, supports weight loss management, and treats dry mouth problems.

Titanium sponge is a highly porous, lightweight form of titanium metal produced through the Kroll process. It is the major raw material in the production of titanium alloys in industrial, automotive, medical implant, and aerospace applications. For high-performance industries, titanium sponge is an indispensable component as it has a very high strength-to-weight ratio, is resistant to corrosion, and is biocompatible. It is prepared by reducing titanium tetrachloride (TiCl4) with magnesium, followed by purification and processing to produce titanium compounds that can be used.

Urea is a nitrogenous compound produced in living organisms as a byproduct of the metabolism of protein degradation. In industrial and agricultural use, urea is a synthetic compound produced on a large scale for use as a fertilizer. Urea is a critical source of nitrogen that helps to enhance plant growth and development. Its high content of nitrogen makes it popular in the agricultural sector and serves as a concentrated, readily available source of nitrogen for crops. Besides being a fertilizer, urea also has several industrial uses, such as the manufacture of adhesives and some resins, as well as plastics.

Active dry yeast is a dehydrated form of yeast commonly used in baking and fermentation. Its dormant yeast cells spring to life when they are rehydrated with warm water. In bread-making, brewing, and other fermentation operations, active dry yeast is frequently employed due to its extended shelf life and convenience of storing. It aids in flavour development and raises dough by generating carbon dioxide. It is a necessary component of both commercial and home baking due to its dependability and convenience.

Ethylene-vinyl alcohol, commonly referred to as EVOH, is an extraordinary polymer with outstanding properties that have revolutionized applications in packaging, industrial, and medical fields. The copolymer consists of alternating ethylene and vinyl alcohol monomer units, which result in the unique gas barrier property that makes EVOH a strong contender for food packaging applications.

Ethylene propylene diene monomer (EPDM) is an adaptable synthetic rubber with unique performance properties. It is a copolymer of ethylene, propylene, and diene monomers and is manufactured through suspension, solution polymerization, or gas-phase polymerization processes. It is commonly used in belts, window and door seals, tubing, roofing membrane, non-slip coatings, radiator, drain tubes, and trunk seals.

Ferrosilicon, an iron alloy made of silicon and iron, is a very versatile alloy that is used in many different industries, especially the steel and casting industries. Its composition can vary, with silicon content ranging from 15% to 90%, depending on the application and desired properties.

Polytetrafluoroethylene (PTFE) refers to a tough, waxy and non-flammable synthetic resin that consists of carbon and fluorine atoms. It is manufactured through the free-radical polymerization process of chloroform, fluorspar and hydrochloric acid. PTFE is usually used to give a non-stick coating to surfaces, especially cookware, such as pans and baking trays and industrial products.

Collagen in the connective tissues, bone, and skin of cows and pigs contains gelatin. A common method for creating this colourless, odourless animal protein is to boil ligaments, tendons, and skin in water. Its outstanding physical characteristics include low viscosity, dispersion stability, high affinity, and dispersibility.

Electrolytic manganese dioxide (EMD) is made by dissolving manganese dioxide in sulfuric acid and placing between two electrodes. Manganese dioxide, also referred to as Manganese (IV) oxide, is an inorganic compound that is commonly found in blackish or brown solid and is insoluble in water. EMD is a highly refined form of MnO2 designed to meet the specific electrical requirements of battery manufacturers.

Electrolytic manganese metal is a pure form of the metallic element manganese, Mn concentration ranges from 99.7% to 99.9%. It is termed "electrolytic" because the refining process involves electrolysis. In other words, a chemical reaction powered by an electric current. Heating the ore and applying chemical processes to remove most impurities is the first steps in the processing of manganese.

Ethanol is a renewable biofuel produced primarily from crops such as corn, sugarcane, and biomass. It is often added to fuel to lower carbon emissions and improve energy security. Additionally, ethanol is used in the beverage, chemical, and pharmaceutical sectors. Ethanol is becoming more popular as a cleaner substitute for fossil fuels due to the rising need for sustainable energy solutions, which is propelling improvements in biofuel technology and production efficiency.

Widely recognized for its superior mechanical, chemical, and thermal properties, unsaturated polyester resin (UPR) is a highly versatile thermosetting polymer utilized across multiple industries. UPR is created when unsaturated acids and glycols react mostly used in composites, coatings, and adhesives.

Sodium cyanide (NaCN) is a highly toxic, colorless crystalline compound with a faint almond-like odor. It is a water-soluble salt composed of sodium (Na+) and cyanide (CN-) ions, known for its versatile applications across various industrial sectors. Despite its hazardous nature, sodium cyanide is extensively used due to its unique properties and efficacy in specific processes.

Caustic soda is the common term for sodium hydroxide (NaOH), a versatile alkali widely used in industries such as chemicals, textiles, pulp and paper, detergents, and water treatment. Sodium hydroxide is known to have strong alkaline properties. It is employed in manufacturing processes such as saponification, pH regulation, and chemical synthesis, making it essential for diversified industrial applications.

Citric acid is a naturally occurring weak organic acid found in citrus fruits, widely used for its sour taste, preservative properties, and acidity regulation. Industrially, it is produced through the fermentation of sugars and is a key ingredient in the food and beverage industry, where it enhances flavor and preserves freshness. Additionally, it has applications in pharmaceuticals, cosmetics, and cleaning products due to its ability to stabilize ingredients and chelate metals.

Calcium stearate, a key chemical compound, holds significant importance across various industries due to its multifunctional properties. Comprising calcium and stearic acid, it serves as a versatile additive and processing aid. As a widely utilized stabilizer and lubricant in the manufacturing of plastics, rubber, and pharmaceuticals, calcium stearate plays a pivotal role in enhancing material properties and processing efficiency.

Calcium hypochlorite is a powerful chemical compound, widely used in many different applications and industries. This white solid, made up of calcium, oxygen, and chlorine, contains excellent chlorine content with a strong oxidation capability. Being an oxidizing agent that gives out chlorine when dissolved in water, it is in huge demand for the treatment, sanitation, and disinfection of water.

Nitrocellulose, also known as cellulose nitrate or guncotton, is a chemically modified form of cellulose known for its exceptional film-forming capabilities, strong adhesion, and biodegradability. It is widely used in applications such as wood coatings, printing inks, leather finishes, automotive paints, nail varnishes, and more.

The growth of the copper wire market is primarily driven by increased electricity demand, heightened investments in construction, expansion of electrical infrastructure, the rise of renewable energy, a shift toward electric vehicles in the automotive industry, and the growing adoption of electric appliances. The development of smart grids and investments in upgrading power transmission systems further boost global copper wire demand. Additionally, the telecom industry's use of copper in optic fiber cables and infrastructure development in emerging markets, especially in Asia Pacific and Latin America, are expected to sustain high demand for copper wire in the coming years.

Urea, also known as carbamide, is an organic compound with the formula CO(NH2)2. It is a highly versatile and widely used chemical, primarily known for its role in agriculture as a nitrogen fertilizer. Urea is available in various grades, including fertilizer grade, feed grade, and technical grade, and is used in a wide range of applications, such as nitrogenous fertilizers, stabilizing agents, keratolytic, and resins, among others. Key industries that utilize urea include agriculture, chemicals, automotive, and medical sectors.

Lithium-ion batteries are rechargeable power sources widely used in devices such as cell phones, laptops, and electric vehicles. These batteries store energy by transferring lithium ions between the anode and cathode electrodes, with the electrolyte facilitating this movement and generating free electrons at the anode. Key types of lithium-ion batteries include those with lithium cobalt oxide, lithium iron phosphate, lithium nickel manganese cobalt, and lithium manganese oxide. Lithium-ion batteries come in a range of capacities from 0 mAh to 6000 mAh. They offer several advantages, including a high energy-to-weight ratio, excellent charge retention, and generally longer lifespans with more charge/discharge cycles compared to other rechargeable batteries.

Brazil is renowned across the world for its enormous rainforests and agricultural resources. Over the recent years, the country has emerged as a major player in the global cellulose industry. As per IMARC estimates, the cellulose fiber market in Brazil was valued at US$ 740.4 Million in 2023. By 2032, the market is projected to reach US$ 1,379.9 Million, growing at a CAGR of 7.0% from 2024 till 2032. Strategic investments in the industry, along with favorable environmental conditions, are guiding a cellulose revolution in Brazil, which is likely to have profound implications for both regional and international markets.

Green chemistry refers to the practice of creating new chemicals, materials, and processes that are less toxic to human health and the environment. It comprises the utilization of renewable resources and reducing waste and energy consumption. Green chemicals are used in various applications such as industrial and chemical, food and beverages, automotive, packaging, construction, agriculture, personal care, and many others. Nowadays, different types of green chemicals are available in the market, including bio-alcohol (bioethanol, bio-butanol, bio-methanol, and many others), bio-organic acids (bio-lactic acid, bio-acetic acid, bio-citric acid, bio-adipic acid, bio-acrylic acid, bio-succinic acid, and others), biopolymers (poly-lactic acid, bio-polyethylene, and others), bio-ketones, bio-solvents, and many other organic acids.

Vanadium has been discovered in sediment samples collected from the Gulf of Khambhat, which opens into the Arabian Sea off Alang in Gujarat. This discovery is expected to enhance the production of steel and titanium in India and boost redox battery manufacturing. Vanadium is one of the most abundant transition metals and is typically found in various minerals, including vanadinite, patronite, and carnotite. It is a hard, ductile, and rare grey metal, often extracted as a byproduct while processing other metals such as iron and uranium.

Steel is a versatile and widely used alloy composed primarily of iron and carbon, with small amounts of other elements such as manganese, chromium, nickel, and others. It is a widely utilized material in construction, manufacturing, and various industries. Steel exhibits a range of desirable properties, including high tensile strength, durability, hardness, corrosion resistance, heat resistance, and the ability to be formed into different shapes. Carbon steel, alloy steel, stainless steel, and tool steel are the main types of steel. Steel is utilized in the manufacturing of various products, including ingots, semi-finished materials, hot-rolled sheets and coils, galvanized sheets, steel tubes and fittings, plates, wire rods, and many others. Its applications span various industries such as building and construction, electrical appliances, metal products, automotive, transportation, and mechanical equipment. The top five exporters of steel are China, Japan, South Korea, and Germany. Similarly, the major importers of steel include the United States, Germany, Italy, and Turkey.

Copper is an essential material in electrical wiring, electronics, and heating systems. It is also highly ductile and malleable, allowing it to be easily shaped and drawn into thin wires. Additionally, copper possesses antimicrobial properties, making it useful in medical and architectural applications. Its resistance to corrosion and its ability to form alloys with other metals further enhance its versatility across various industries.